Leidos Holdings Boosts Margins and Advances Digital Modernization in FY2025

Leidos leverages government contracting expertise and disciplined capital allocation to enhance profitability amid modest revenue growth.

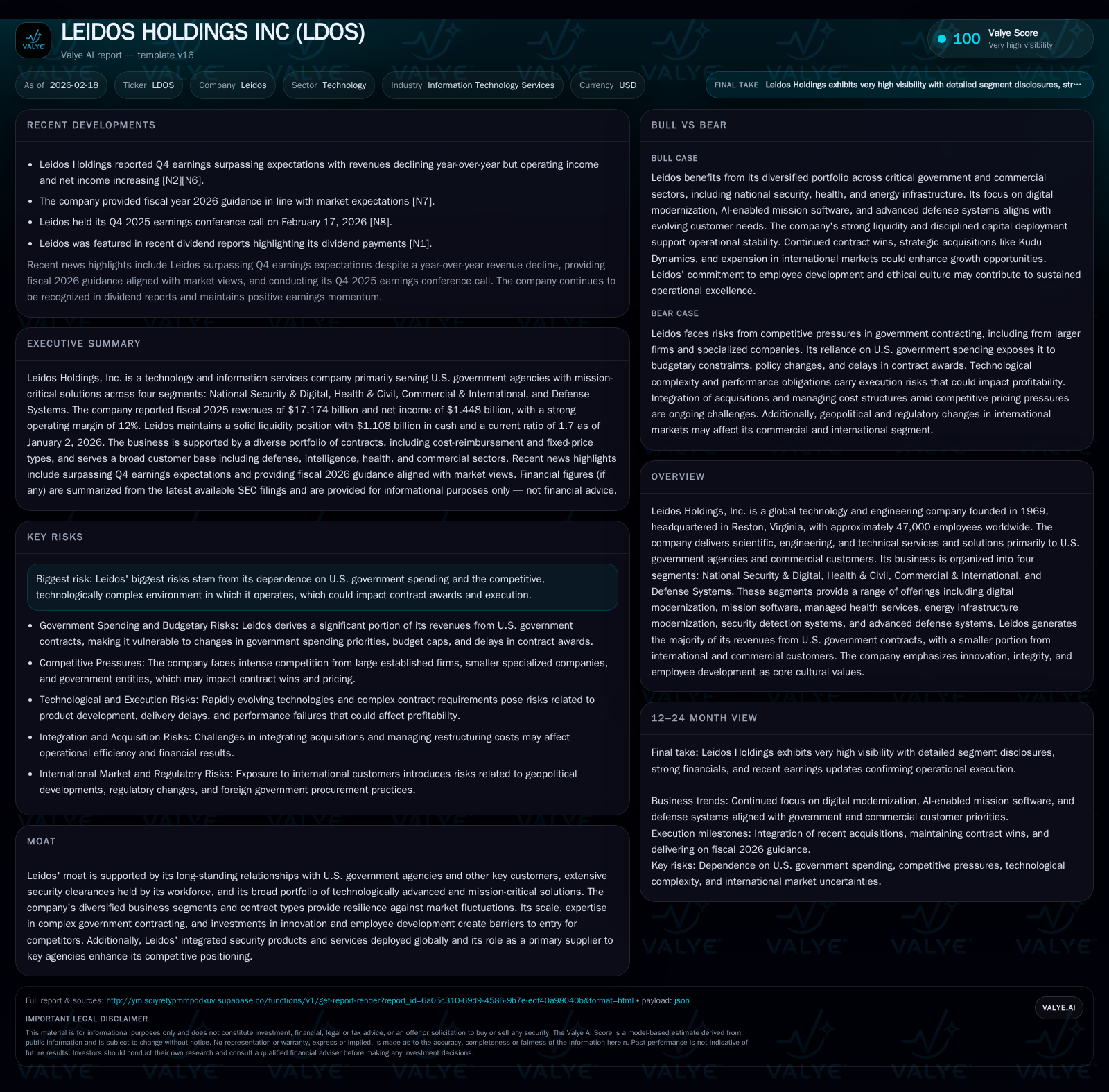

Leidos Holdings posted a 3.1% revenue increase in fiscal 2025, reaching $17.17 billion, while significantly outpacing top-line growth with 15.4% operating income expansion and 15.5% net income increase, driven by operational efficiencies and cost management. Its primary focus on U.S. government contracts—accounting for approximately 87% of revenues—coupled with investments in digital modernization and advanced defense solutions underpin future growth prospects. Though near-term guidance aligns with expectations, uncertainties around federal budget appropriations remain a key risk factor. The company’s robust return on equity near 30%, strong cash flow generation, and increased buyback activity reflect its disciplined capital allocation strategy.

Financial Performance Overview: A Closer Look at FY2025

Leidos Holdings Inc reported steady top-line growth in its fiscal year ended January 2, 2026 (FY2025), with revenues increasing by 3.1% to $17.17 billion compared to $16.66 billion in FY2024 [F1]. Despite this modest headline improvement, the company achieved significant operating income growth of 15.4%, rising to $2.11 billion from $1.83 billion year-over-year, accompanied by a net income increase of 15.5% to $1.45 billion [F1]. These figures demonstrate notable margin expansion driven by operational efficiencies and effective cost controls against the backdrop of competitive pressures in government contracting.

Operating cash flow (CFO) generation also accelerated markedly by 25.7%, climbing to $1.75 billion from $1.39 billion [F1], reflecting improved working capital management alongside enhanced earnings quality.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 17.2 | 1448 | 1750 | 2.1 | +3.1% | +15.5% |

| 2024 | 16.7 | 1254 | 1392 | 1.8 | +7.9% | +530.2% |

| 2023 | 15.4 | 199 | 1165 | 0.6 | +7.2% | -70.9% |

| 2022 | 14.4 | 685 | 986 | 1.1 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 400 | 29.5 |

| 2024 | 850 | 28.4 |

| 2023 | 225 | 4.7 |

| 2022 | 0 | 15.9 |

Source: SEC companyfacts cache [F1].

Note: Capex data insufficient for recent years from tags.

Drivers Behind Revenue Growth and Segment Dynamics

Approximately 87% of Leidos' FY2025 revenues stemmed from U.S. government contracts, primarily via prime contractor positions or as subcontractors supporting critical agencies including the Department of War (DoW), Intelligence Community, Homeland Security (DHS), Federal Aviation Administration (FAA), Veterans Affairs (VA), among others [S1][S5]. This heavy concentration affords revenue stability but also exposes the company to shifts in federal spending priorities.

Revenue contributions are segmented into four major reportable divisions:

National Security & Digital: The largest segment propelling topline gains focused on delivering advanced technological capabilities—such as digital modernization, IT transformation services, cyber security enhancements—to federal clients nationwide [S13]. This unit accounted for roughly half of total revenue and benefited from increased demand driven by ongoing governmental digitization initiatives.

Health & Civil: Represented about 30% of revenues and includes managed health services alongside mission software solutions supporting healthcare systems within DoD and VA hospitals [S18]. This stable area has expanded gradually but faces typical healthcare sector regulatory complexities.

Commercial & International: Constituting approximately 13%, this segment serves international governments (notably UK Ministry of Defence and Australia), investor-owned utilities for energy infrastructure modernization projects, and provides integrated security detection products globally [S6][S18]. Growth has been somewhat muted due to geopolitical risks and supply chain constraints affecting commercial customers.

Defense Systems: Making up around a dozen percent of revenues, Defense Systems supplies rapid prototyping hardware/software solutions for DoD specialties such as multi-domain operations, autonomous systems development, and intelligence tools [S6].

The balanced presence across multiple verticals helps mitigate market cycle volatility inherent in any single segment [S13]. Moreover, shifts toward multiple-award IDIQ contracts have intensified competition but also increased opportunities for longstanding providers like Leidos that possess requisite security clearances and broad domain expertise [S5].

Digital Modernization and Advanced Solutions Powering Future Prospects

Digital modernization remains at the core of Leidos’s strategic investment themes aimed at sustaining medium- to long-term growth [N14][S1]. Its National Security & Digital division leverages AI-driven analytics, cloud migration services, cybersecurity enhancements aligned with evolving Department of Defense Cybersecurity Maturity Model Certification (CMMC) standards, and mission software innovation across space/maritime defense platforms [S21]. These capabilities address critical federal priorities ranging from infrastructure resilience to emergent cyber threats.

Expansion into energy infrastructure modernization under the Commercial segment supports utility clients aiming to upgrade grid reliability through smart grid technologies and electrification strategies [S14][N14]. Global security products deployed internationally further diversify exposure.

Nevertheless, risks persist owing to uncertain appropriations cycles stemming from ongoing congressional debates on fiscal budgets including recent DHS funding delays that briefly shuttered parts of the department early in calendar year '26 [N14][S24]. Leidos’s scalability within digital domains coupled with its ability to integrate legacy systems remains a competitive advantage against both established federal contractors and newer technology entrants seeking footholds.

Visible Near-Term Guidance and Key Operational Milestones

For fiscal year ending January '27 (FY2026), management's guidance is aligned with market expectations forecasting revenue stabilization accompanied by modest margin improvements driven by continued efficiency gains in contract execution [N14].

Absent explicit numerical guidance beyond general commentary [N14], it will be important to track:

- Renewal rates on major multi-year contracts within National Security & Digital;

- Progress against enterprise transformation goals leveraging AI/automation;

- Integration effectiveness following the acquisition of Savanna Industries ("Kudu Dynamics") completed during FY2025;

- Margin sustainability amid evolving labor cost structures and competitive bidding pressures.

Quarterly earnings cadence may remain impacted by seasonal factors related to government fiscal calendar timing as well as contract award variability [S21]. Maintaining backlog strength remains essential for forward visibility into revenue streams.

Capital Allocation Strategy: Shareholder Returns and Cash Flow Generation

Leidos exhibits disciplined capital deployment characterized by strong operational cash flow conversion complemented by a conservative approach toward capital expenditures totaling moderate levels relative to operating cash inflows [F1][N12]. For FY2025:

- Operating cash flow rose robustly by approximately $315 million (+25.7%) compared with FY2024 reaching $1.75 billion [F1];

- Free cash flow after estimated capex stands near $1.63 billion (capex not fully detailed but modest relative scale inferred from available historic data) [F1];

- Return on equity hovered near an impressive ~29.5%, highlighting profitable reinvestment efficiency given equity base near $4.92B at fiscal year-end [F1];

- The company continues buybacks albeit at reduced levels versus prior years with repurchases totaling $400 million versus $850 million in FY2024 indicating prudence amid macroeconomic uncertainties [F1];

- Dividend payments have been reinitiated recently reinforcing shareholder distribution alongside buybacks per market dividend reports [N12].

This balanced mix reflects management’s commitment to enhancing shareholder value while preserving financial flexibility for strategic investments or acquisitions such as the Kudu Dynamics deal closed during FY25 [S6].

Risk Factors Unique to Government Contracting Exposure

Leidos operates within a rigorously regulated environment subject to extensive legal oversight due both to its customer base predominately consisting of U.S federal agencies (~87%) and the sensitive nature of many contracts involving classified information or national security missions [S4][S21]. Risks include:

- Dependence on U.S government spending levels which may fluctuate amid political impasses over budget appropriations or broad macroeconomic pressures such as sequestration caps embedded in the Budget Control Act or newer fiscal responsibility measures [S24];

- Heightened compliance obligations stemming from cost accounting standards (CAS), Federal Acquisition Regulations (FAR/DFARS), cybersecurity mandates including CMMC enforcement phases impacting subcontractor qualification criteria; potential penalties include contract termination or suspension [S9][S21];

- Exposure to investigations arising from audits or claims under False Claims Acts or related regulations that can result in severe financial penalties alongside reputational harm adversely affecting future contract awards [S4][S26];

- Complex international regulatory risks as Leidos expands non-U.S government operations (~8% revenues) subject to export controls such as ITAR/EAR plus geopolitically sensitive jurisdictions increasing compliance burdens [S25];

- Escalating cybersecurity threats including data breaches that could compromise classified client information with attendant legal liabilities and performance disruption risks; investments targeting enhanced information assurance remain ongoing operational priorities [S23];

- Intensifying competition both from large legacy players like Accenture Federal Services or Amentum combined with niche technology startups capable of rapid innovation potentially disrupting traditional delivery models requiring continuous program management vigilance [S16][S17].

Mitigating these risks requires stringent internal controls adherence combined with employee training programs focused on ethics and compliance as well as proactive engagement with government regulators.

The information presented herein is based solely on publicly available sources including Leidos Holdings' SEC filings ([F1]/[S#]) and recent news commentary ([N#]). This report is intended solely for informational purposes without providing any investment recommendation or advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments