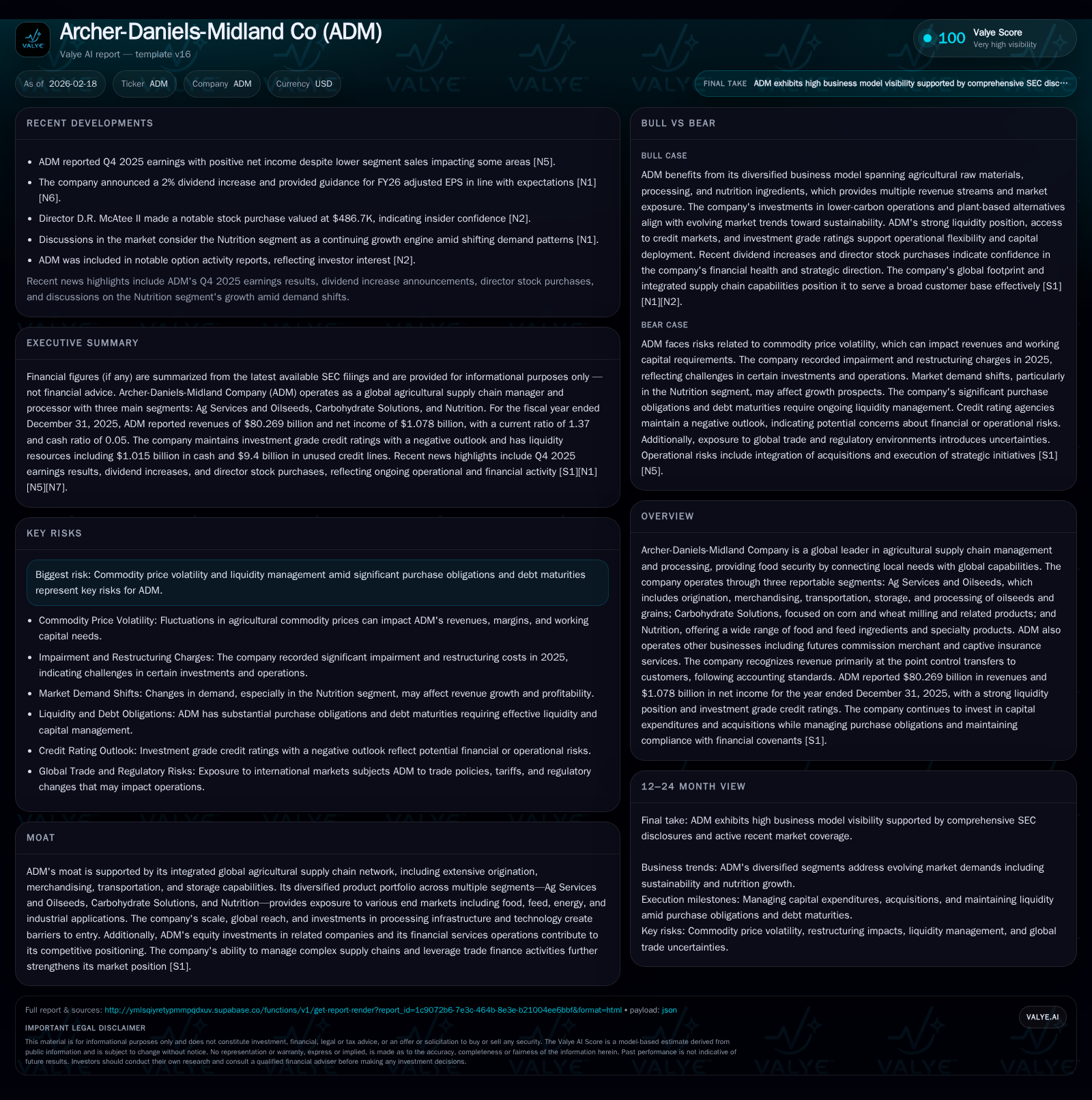

ADM’s Strategic Balance: Managing Supply Chain Scale and Margin Pressures

ADM leverages vast global agricultural supply chains and diversified segments to mitigate margin pressures amid commodity volatility.

Archer-Daniels-Midland Co (ADM) showcased substantial top-line contraction in FY2025 driven by weaker commodity prices and volumes, yet notably delivered strong operating cash flow growth. The company’s three-segment model—Ag Services and Oilseeds, Carbohydrate Solutions, and Nutrition—faces varied margin impacts shaped by deferrals in biofuel policies, global trade challenges, and regulatory delays. ADM maintains a solid liquidity profile supported by operational cash generation and ample credit facilities while balancing capital allocation priorities with sustained dividends amid a pause in share repurchases. Continued legal proceedings pose uncertainties, but ADM’s integrated supply chain infrastructure and segment diversification underpin its resilience as it navigates evolving industry dynamics.

Strong Foundations: ADM’s Historical Revenue and Profit Patterns

ADM reported FY2025 revenues of $80.3 billion, declining by 6.2% from $85.5 billion in FY2024 [F1]. This revenue contraction was largely attributable to softer sales volumes and lower commodity prices within its Ag Services and Carbohydrate Solutions segments, offset modestly by pricing gains in Nutrition. Net income experienced a steeper decline, falling by 40.1% YoY to $1.08 billion in FY2025 from $1.8 billion the prior year, reflecting compressed margins amid elevated supply levels and deferrals of key biofuel policies [F1][S17]. However, operating cash flow surged nearly double (+95.4%) reaching $5.45 billion due to improved working capital management, particularly effective control of inventory, payables including brokerage customer balances, and other accrued expenses – highlighting operational resilience even as profitability took a hit [F1][S4]. Capital expenditures tapered down by about 20%, standing at $1.25 billion in FY2025 versus $1.56 billion last year pointing to controlled spending focused on processing capacity optimization [F1].

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 80.3 | 1.1 | 5.5 | 1248 | -6.2% | -40.1% |

| 2024 | 85.5 | 1.8 | 2.8 | 1563 | +272.2% | +218.6% |

| 2023 | 23.0 | 0.6 | 4.5 | 1494 | -77.4% | -87.0% |

| 2022 | 101.6 | 4.3 | 3.5 | 1319 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 987 | 0.0 | 4.2 |

| 2024 | 985 | 2.3 | 1.2 |

| 2023 | 977 | 2.7 | 3.0 |

| 2022 | 899 | 1.4 | 2.2 |

Source: SEC companyfacts cache [F1].

- Note: FY2023 revenue appears anomalous likely due to reporting differences; excludes meaningful segments reclassification or adjustments. ** Percentage change not meaningful due to prior year baseline differences.

Source: [F1]

Segment Insights: Ag Services, Carbohydrate Solutions, and Nutrition Dynamics

ADM’s business is organized into three segments with distinct margin profiles and exposure to commodity dynamics:

Ag Services and Oilseeds: This largest segment includes grain origination, merchandising, storage, transportation, as well as oilseed crushing operations producing vegetable oils and protein meals serving food, feed, energy (including biofuels), and industrial markets worldwide [S18]. In FY2025 revenue declined roughly 7% to $61.6 billion as both volumes (-$2.8B) and prices (-$2.1B) softened amid increased global grain supplies increasing stock-to-use ratios globally which pressured gross margins [S18][S17]. Notably, North American origination faced uncertainty from expanding trade policy frictions but saw a partial rebound in soybean exports later in the year against China demand returning incrementally [S1]. Additional headwinds stemmed from logistical challenges underpinned by low water levels slowing shipment execution pace along key river corridors affecting timing rather than absolute volume realization [S17]. South America faced slower farmer selling while the Black Sea origination was hampered by retention issues linked to geopolitical tensions around Russia-Ukraine conflict escalations impacting physical exports availability [S1][N2]. Furthermore, postponement of the EU Deforestation Regulation implementation has deferred anticipated premiums or penalty mechanisms affecting refining subsegments' volumes and margins negatively at least temporarily [S18]

Carbohydrate Solutions: This corn and wheat milling segment converts raw materials into sweeteners like glucose syrups, starches used in food/beverages, fermentation feedstocks such as alcohols, and animal feed ingredients [S20]. Revenues dropped approximately 4% YoY to around $10.7 billion driven primarily by lower prices (-$330 million) combined with volume reductions (-$167 million). Biofuel policy deferrals also impacted ethanol production anticipation which directly influences downstream carbohydrate demand eroding margin potential here compared to more stable Nutrition margins although manufacturing costs rose moderately due to inflationary pressures on labor/energy input costs across EMEA markets [S17][N2]

Nutrition: The most specialty-focused segment delivering plant proteins, natural colors/flavors systems, enzymes, probiotics/prebiotics along with edible beans/feed ingredients manifested resilient demand trends with revenues growing slightly (+2%) reaching approximately $7.5 billion through a mix of higher sales prices (+$68 million) and asset redeployment gains such as contract cancellation benefits adding ~$55 million during the year [N12][S18]. Segment operating profit improved modestly driven by mix optimization even as commodity-related cost passthroughs differ meaningfully from the other more commodity-volume exposed segments where margins tie closely with underlying raw material pricing volatility vs Nutrition where value-added formulations allow better margin control [N12][S13].

Commodity Influences and Regulatory Challenges Shaping Margin Trends

Commodity price volatility constitutes a double-edged sword given ADM's vast integrated supply chain scale but limited pricing flexibility in volume-heavy segments like Ag Services/Oilseeds where cost passthrough typically neutralizes much of gross margin swings barring logistical disruptions or policy changes impacting volumes or operational cadence [S17][S18]. In contrast, Nutrition's downstream innovation portfolio decouples revenue growth from pure commodity movements allowing selective margin expansion opportunities.

ADM contended with larger-than-normal stock-to-use ratios through FY2025 exerting downward pressure on spreads especially among grains/oilseeds fed into refining/crushing operations that also suffered from mandated deferrals — chiefly U.S.-based biofuel policies delayed pending legislative clarity reducing domestic renewable fuel blend mandates critical for soybean oil derivative demand while similarly postponements of EU Deforestation Regulations held back sustainable premium market capture prospects internationally [S1][N2][N12]. These regulatory uncertainties extend execution risk into adjacent shipping/logistics sectors where asset utilization softens amid weather-created bottlenecks like historically low river water levels restricting barge traffic slowing throughput rates impacting timing-sensitive trading windows especially along Mississippi river systems integral for outbound exports from North America bulk warehouses [S17][N2]. Additionally geopolitical strains on Black Sea corridor trade routes continue impairing origination volume fulfillment from Ukraine/Russia regions thereby amplifying supply chain complexity costs despite ADM's robust multimodal transport assets deployed worldwide [S1][N2].

Cash Generation and Investment Patterns: A Closer Look at Capital Allocation

Despite falling net income margins in fiscal year 2025, ADM's free cash flow remained robust at approximately $4.2 billion (operating cash flow of $5.45 billion minus capital expenditures of around $1.25 billion) affirming improved working capital dynamics management under stress conditions including inventory control optimizing payables cycles from brokerage customers alongside prudent capex moderation aimed at refining existing processing infrastructure rather than scaling aggressively amid uncertain macro market directions [F1][S10]. Return on equity calculated roughly at a subdued ~4.7%, down from prior years consistent with net income shrinkage versus steady equity base demonstrating ongoing capital efficiency pressures but still positive relative cash yield generation supporting dividend continuity.

Dividend payments totaled about $987 million sustaining investor income attraction aligned with corporate policy despite pausing repurchase activity for the full calendar year of 2025 – a notable shift versus multi-billion dollar buyback bursts observed over previous cycles ($2+ billion annually) signaling liquidity preservation focus while maintaining shareholder return flexibility should market conditions pivot favorably over short-to-medium horizon periods [F1][S23][N11]. Insider buying activities during early 2026 signal selective confidence among directors even as external macro risks remain high.

Liquidity Profile and Debt Management in a Volatile Market

As of end-2025 ADM held approximately $1 billion in cash with an undrawn credit line capacity near $9.4 billion forming total available liquidity exceeding $10 billion adequate for covering working capital volatility periods including anticipated long-term maturities (~$1 billion current portion payable within twelve months) plus planned dividend/capex commitments without access strain evident currently given historical demonstrated ability tapping public/private capital markets domestically/internationally where ADM maintains investment grade credit ratings albeit accompanied by negative outlook revisions reflecting sector cyclicality risks facing agribusiness globally amid trade/franchise uncertainties [F1][S4][S8][S11]. The company's current ratio approximated at healthy ~1.37 indicating well-matched short-term asset/liability structure supporting operating cash conversion cycles.

Long-term debt aggregated roughly $6.6 billion post-$0.67B repayment smoothing future interest & principal burdens across diversified maturities extending effectively into late decade timeframe dyad ensuring measured refinancing risk exposure coupled with covenant compliance intact under current rating criteria providing manageable leverage optics through turbulent agrarian cycles ahead [S11][S14].

Legal and Regulatory Risks: Litigation Impact and Outlook

ADM remains entrenched in multiple legal proceedings primarily tailored around alleged commodities manipulation involving putative class actions originally filed circa mid-2019 plus derivative lawsuits targeting governance conduct related claims dating back approximately two years ago respectively with ongoing motions hearings leading only partially resolved outcomes presently leaving open risk windows subject to final court adjudication timelines potentially extending well beyond current fiscal periods yet management maintains active defense strategies stressing lack of substantive merit leading them to affirm no expected material adverse financial impact derived therefrom thus far though investor perceptions may reflect cautious sentiment weighting such latent liability scenarios amid continuing regulatory scrutiny demanding vigilant monitoring going forward [S6][S7].

Forecast Signals: What to Watch in ADM’s Upcoming Earnings and Strategy Updates

Explicit quantitative forward guidance has not been issued for upcoming periods necessitating investor focus on qualitative indicators including evolving U.S./EU biofuel regulatory clarifications impacting volume ramp-ups especially within Ag Services refining subsegments aligned with possible trade dispute resolutions affecting export optimism notably toward China market absorption potential key for soy exports resumption momentum recovery narratives highlighted in recent earnings calls alongside Nutrition segment growth sustainability amid shifting consumer demand patterns relying increasingly on premium plant-based ingredient formulations offering differentiated margin cushions compared against legacy commodity exposure segments thus shaping average blended profitability forecasts moving forward [N3][N12]. Further scrutiny of working capital fluctuations embedded within quarterly results will clarify whether recent efficiency gains hold steady sustaining robust free cash flows underpinning future capital deployment options either reinvestment cycles or renewed shareholder return initiatives remain pertinent watchpoints.

This report compiles data derived exclusively from Archer-Daniels-Midland Company’s publicly available SEC filings as of February 17, 2026 ([F1],[S#]) combined with recent news releases up to February 13, 2026 ([N#]). Analysis herein aims exclusively to provide factual company insights without endorsing specific investment decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments