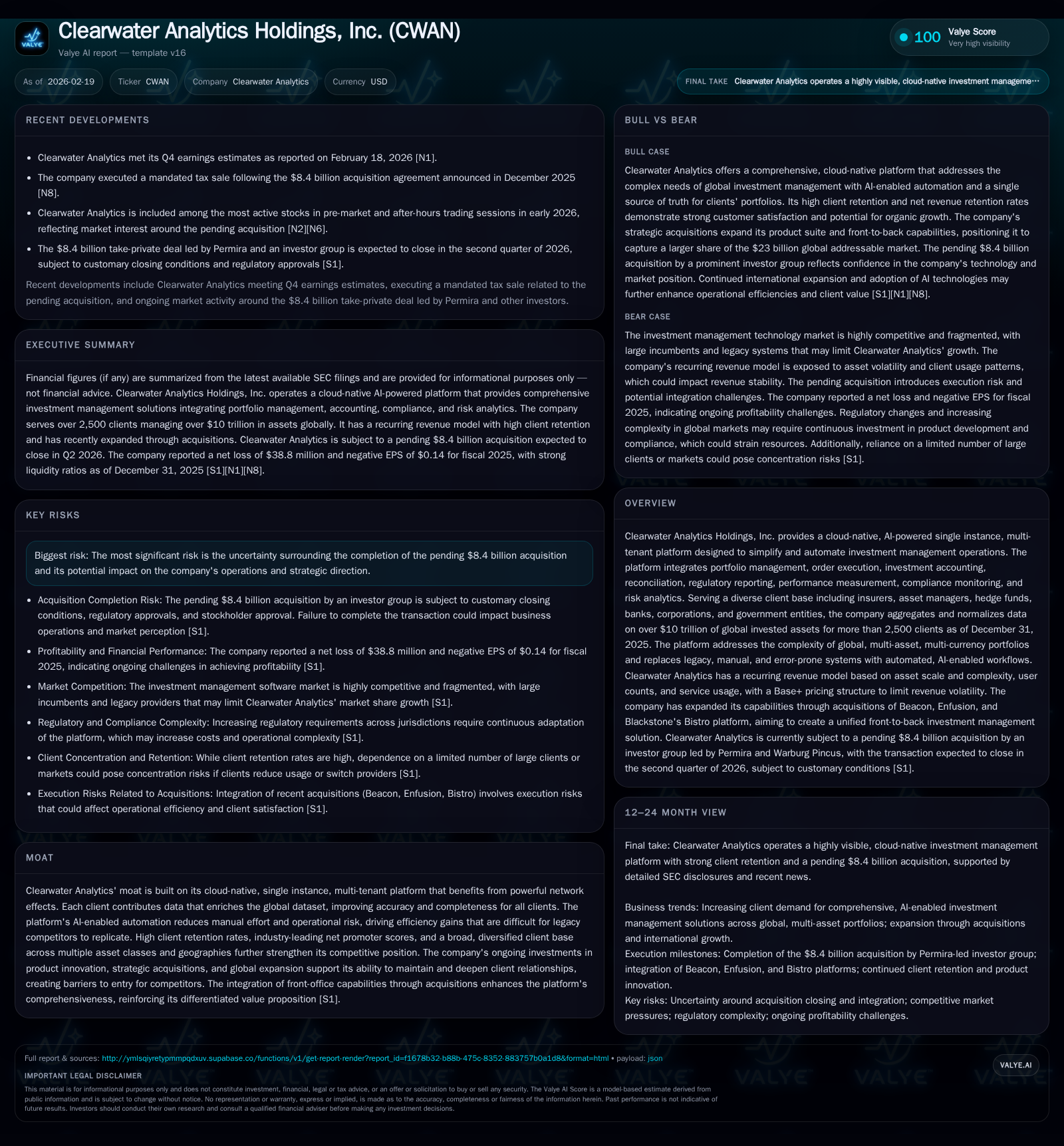

Clearwater Analytics Faces Profitability Setback While Scaling AI-Driven Investment Platform

An $8.4 billion acquisition looms as Clearwater expands its cloud-native SaaS for complex investment management.

Clearwater Analytics Holdings, Inc. offers a comprehensive cloud-native platform that automates global investment operations across multiple asset classes, leveraging AI to reduce manual workflows and deliver timely portfolio insights. The company has scaled impressively to over 2,500 clients managing more than $10 trillion in assets but reported a notable operating and net loss in fiscal 2025 linked to high expenses and merger-related costs. While recurring revenues remain robust with strong client retention, significant risks revolve around the pending investor group acquisition expected in Q2 2026. Future growth will depend on deepening client relationships, expanding internationally, and integrating acquired front-office capabilities.

Company Overview

Clearwater Analytics Holdings, Inc. (CWAN) provides a cloud-native, AI-driven investment management platform designed to simplify the multifaceted operations underlying modern portfolio management. Its single instance, multi-tenant SaaS architecture consolidates portfolio management, order execution, investment accounting, regulatory reporting, compliance monitoring, performance measurement, risk analytics, and reconciliation into a unified workflow. This integration addresses the complexities faced by asset owners and managers navigating multi-asset class portfolios spanning diverse geographies, currencies, and accounting bases.

By aggregating normalized data for over $10 trillion in global invested assets across more than 2,500 institutional clients—including insurers, asset managers, hedge funds, banks, corporations, government entities—Clearwater delivers daily or on-demand visibility enabling timely decisions on performance and compliance [S4][S16].

Historical Financial Performance

Revenue Data Gap

Direct revenue figures are not available within provided disclosures; however, other financial metrics detail operational outcomes.

Operating Income Behavior

CWAN's operating income demonstrated volatility over recent years: positive but modest income of $5.1 million in FY2022 swung sharply to negative $16.7 million in FY2023 before recovering slightly near breakeven in FY2024 ($12.2 million profit) and then declining again to a $7.7 million operating loss in FY2025 [F1]. The underlying swings reflect substantial investments tied to business growth and merger-related expenses.

Net Income Trends

The firm recorded net losses in three of the last four fiscal years except FY2024 when it posted an anomalously large income of $424 million—likely reflecting nonrecurring items such as gains from acquisitions or accounting adjustments—followed by a sizable net loss of $38.8 million in FY2025 [F1].

Cash Flow and Capital Deployment

Operating cash flow expanded robustly from $58 million in FY2022 to roughly $176 million in FY2025 (+137% YoY), enabling the firm to finance ongoing investments [F1]. Capital expenditures approximately doubled between FY2024 ($5.3 million) and FY2025 ($11.5 million), illustrating an increased spend on technology infrastructure supporting product innovation [F1].

This free cash flow generation surplus of circa $164 million (CFO minus Capex) contrasts with net losses on the income statement and underscores strong cash conversion from subscription fees typical for SaaS models.

Shareholder Returns

In FY2025 CWAN repurchased approximately $18 million of common stock; no dividend payments were reported during this period indicating capital allocation prioritizes reinvestment and share repurchases [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -39 | 176 | -8 | 12 | -109.1% |

| 2024 | 424 | 74 | 12 | 5 | +2062.3% |

| 2023 | -22 | 85 | -17 | 6 | -171.5% |

| 2022 | -8 | 58 | 5 | 8 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 18 | 164 | -1.9 |

| 2024 | 69 | 42.1 | |

| 2023 | 0 | 79 | |

| 2022 | 1 | 50 |

Source: SEC companyfacts cache [F1].

Note: Revenue unavailable; dividends omitted due to insufficient data.

Growth Drivers and Strategic Positioning

Product Strengths and Moat

Clearwater’s moat is anchored on its cloud-native architecture delivering industry-leading automation with embedded AI/ML capable of driving up to 90% reductions in manual reconciliations and speeding report generation by nearly 80%, with same-day audit readiness [S14]. This efficiency gain undercuts legacy systems heavily reliant on manual workflows.

The platform uniquely supports extensive global complexity including multi-asset classes (fixed income, equities, alternatives like private credit), multiple currencies (>60 local), functional accounting standards (>45 bases), fulfilling varied regulatory regimes across continents [S24]. This breadth enables clients a "golden copy" consolidated view essential for risk management and compliance.

High client retention metrics—gross revenue retention remained above 98% for nearly seven years continuously with net revenue retention at about 109%, reflecting upsell success—underscore sticky customer relationships [S4][S17].

Market Opportunity

The total addressable market (TAM) is estimated near $23 billion globally encompassing asset managers ($10B), insurance companies ($6B), pension funds/governments ($3B), among others leaving ample penetration headroom given CWAN’s ~4% current market share [S6][S17].

International growth is prioritized with offices across Europe and Asia-Pacific but currently only contributes roughly one-quarter of revenues versus making up half the TAM—highlighting substantial expansion potential outside the U.S. [S17].

Client End-Markets Expansion

Besides established customer verticals (insurance, asset managers, hedge funds), Clearwater intends targeted expansion into adjacent markets including sovereign wealth funds, pension funds, state/local governments leveraging customization capabilities especially within regulatory reporting functions [S17].

Recent Acquisitions Integrate Front-Office Solutions

Acqui sitions like Enfusion's Bistro front-office platform enable cross-selling integrated front-to-back capabilities embedding order management/risk analytics juxtaposed with Clearwater's strength in middle/back-office functions aiming for holistic solutions that improve client retention and increase wallet share [S6][S16].

Risks Surrounding Pending Acquisition

The company's current trajectory is marked by a pending acquisition agreement completed late December 2025 valued at approximately $8.4 billion involving private equity firms Permira, Warburg Pincus, Temasek Holdings, and Francisco Partners [S1][N3]. Completion is anticipated by Q2 2026 but subject to regulatory approvals including Hart-Scott-Rodino clearance recently granted early termination effective Feb ’26 [S16].

Risks include:

- Potential delays or failure affecting stock price stability,

- Restrictions preventing strategic moves until deal closure,

- Possible distractions for management impacting ongoing operations,

- Increased cost of capital post-announcement,

- Legal actions arising from merger proposals that may delay or impair transition,

- Approximate termination fee of $200 million payable if deal falls through under certain circumstances.

These uncertainties could impair talent retention or client relationships temporarily as well [S1][S19].

Forecasts & Milestones To Watch

CWAN has not publicly provided formal guidance amid merger finalization but highlights include:

- Merger close expected in H1/2026,

- Potential integration success of front-office capabilities via acquisitions like Enfusion,

- Further scaling international presence,

- Expansion into adjacent segments,

- Ongoing improvements in AI-enabled workflow automation expanding operational efficiencies. Monitoring quarterly updates post-merger announcement will be critical to assess progress toward these milestones [N1][N2][S16].

Capital Structure & Returns Analysis

As of December 31, 2025 CWAN had healthy liquidity with cash & equivalents exceeding $91 million against current liabilities near $161 million resulting in a current ratio of about 1.83—a reasonable short-term financial position given cash flow ability [F1][S5]. Equity capital stood at over $2 billion reflecting substantial book value growth likely impacted by share issuances related to previous financing rounds or equity comp plans [F1].

Return on Equity based on latest annual results was negative approximately -1.9%, signaling profitability challenges driven primarily by nonrecurring costs during aggressive growth phases [F1]. However strong operating cash flow conversion mitigates these concerns somewhat from a cash perspective.

Share repurchases resumed moderately (~$18 million) in FY2025 showing confidence in capital discipline though no dividends were declared suggesting reinvestment focus remains dominant amidst competitive SaaS landscape dynamics [F1].

Industry Context & Competitive Landscape

The broader investment management software sector remains highly fragmented featuring established incumbents offering legacy systems often deployed on-premise (SS&C’s Advent suite; State Street; BNY Mellon’s Eagle; BlackRock Aladdin). Competitors face challenges migrating clients toward scalable cloud architectures – an area where Clearwater’s single-instance multi-tenant platform provides differentiation [S27].

Strong network effects arise as each client adds data enhancing aggregate insight quality improving comparability benchmarks—a significant barrier for greenfield entrants or legacy providers lagging AI adoption [S27]. Competition also includes internal IT department bespoke solutions though these tend toward costly manual effort prone to errors.

The industry's accelerating shift toward real-time data availability combined with rising regulatory demands around ESG metrics heightens demand for Clearwater’s compliance & reporting solutions which are continuously updated for new regimes including NAIC/Statutory / Solvency II provisions plus emerging ESG standards increasingly influential for institutional investors globally [S25][S26].

Conclusion

Clearwater Analytics stands at an inflection point showcasing robust SaaS platform scale supporting vast global institutional assets through advanced AI powered investment management automation with high client stickiness evidenced by retention rates and NPS scores. However the firm’s recent operating losses reflect elevated expenses linked partly to merger activities alongside increased R&D/sales capacity investments aimed at future growth. Successful closure of the pending acquisition will introduce new strategic direction while preserving or enhancing existing go-to-market efforts will be key for sustained momentum given rich market opportunity both domestically and abroad. Investors should watch execution risks evolving through H1’26 alongside integration achievements that could unlock further cross-selling synergies especially around front-office capabilities merging seamlessly into CWAN’s core platform. Cash flow strength remains a notable positive enabling continued innovation even amid short-term earnings volatility common within high-growth SaaS environments serving complex financial services ecosystems.

Disclaimer: This analysis is informational only without any buy or sell recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments