Consolidated Water's Licensing and Receivables Challenges Cloud Growth Trajectory

Latest Q1 2026 report highlights regulatory renegotiations in Cayman and collection delays in Bahamas impacting operating income.

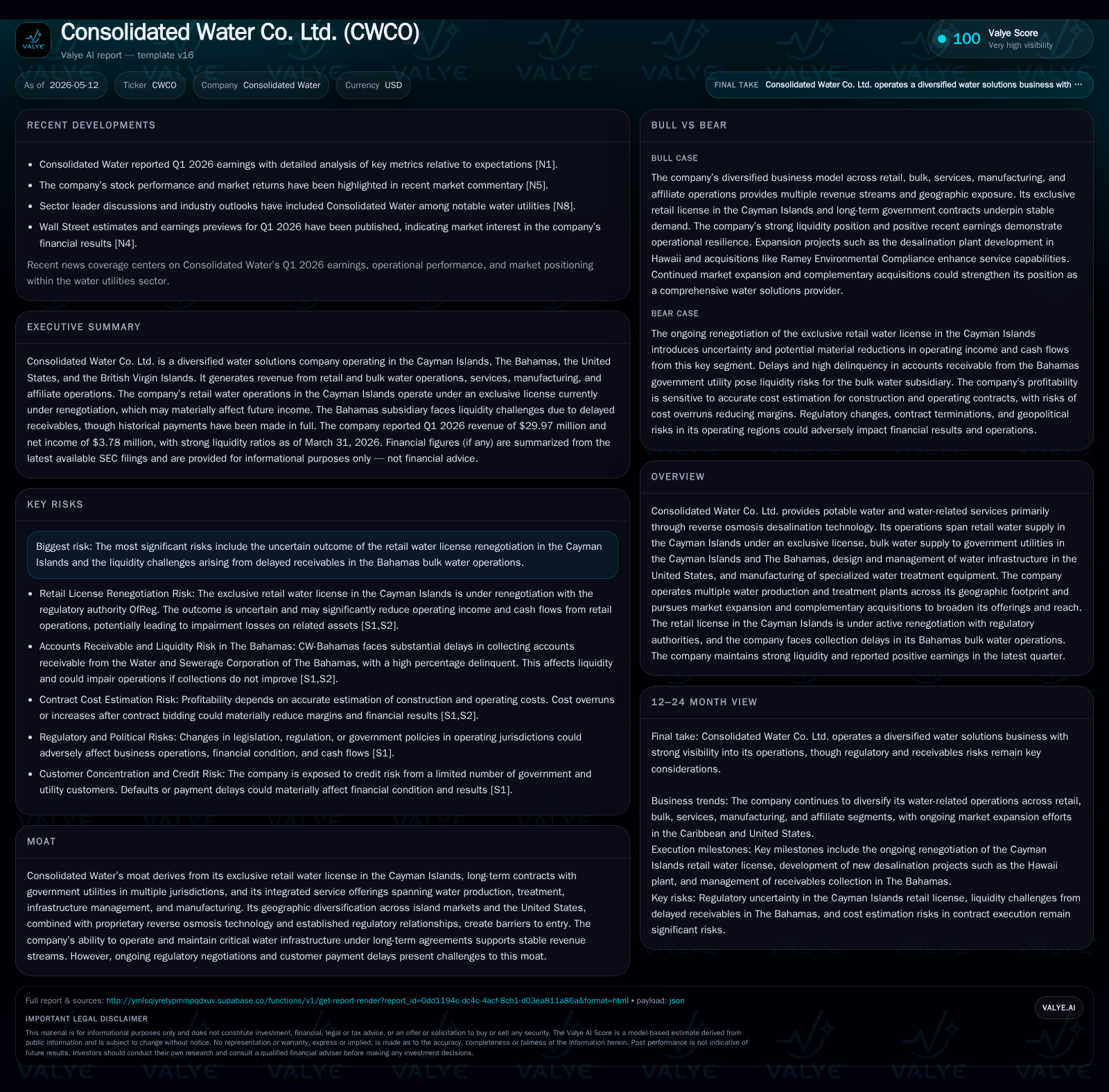

In Q1 2026, Consolidated Water Co. Ltd. reported continued uncertainty around its exclusive retail water license in the Cayman Islands, with ongoing negotiations that could materially reduce historic operating income from this core segment. Additionally, the company faces significant receivable collection delays in its Bahamas bulk water operations, posing liquidity risks. Despite these headwinds, Consolidated Water maintains strong overall liquidity and a diversified business model spanning desalination, water infrastructure services, and manufacturing. The company’s integrated reverse osmosis capabilities and entrenched regulatory relationships underpin its defensibility, but near-term growth depends heavily on license resolution and improved receivables management.

Recent Operating Update: Q1 2026 Highlights and Regulatory Developments

Consolidated Water Co. Ltd.'s latest quarterly filing for Q1 ended March 31, 2026 reveals that approximately 29% of its consolidated revenue and a disproportionate 45% of gross profit were generated from its Cayman Islands retail water operations conducted under an exclusive license granted in 1990 [S2]. This marks a slight increase compared to prior periods where retail contributed about 26–28% of revenue.

However, the company's dominant retail license covering two of Grand Cayman's most populated areas — Seven Mile Beach and West Bay — remains under active renegotiation with OfReg, the newly established regulatory authority responsible for economic regulation since 2017 [S2]. The original license was due to expire in July 2010 but has been extended multiple times; the last express extension expired January 31, 2018. Since then, operations have continued under the old license terms with continuous royalty payments.

OfReg reportedly seeks to restructure the license terms significantly, which could materially reduce Consolidated Water's historical operating income and cash flow derived from this segment [S2]. The company acknowledges it is unable to predict the outcome or quantify the financial impact currently but flags potential impairment losses on retail segment assets if license negotiations conclude unfavorably.

Meanwhile, troubling developments persist within the Bahamas bulk water operations unit (CW-Bahamas). As of February 28, 2026, accounts receivable due from the Bahamas government utility (WSC) stood at $22.6 million with approximately 75% classified as delinquent—delays that periodically stress operational liquidity [S2]. This raises the risk that CW-Bahamas could lack sufficient liquidity to continue uninterrupted operations and poses further downside risk to consolidated financial results through increased credit loss provisions or unrecognized revenue.

These near-term uncertainties dominate Consolidated Water's current operating picture despite an otherwise diversified portfolio generating steady demand across segments.

Business Model: Integrated Desalination with Multi-Channel Revenue Streams

Consolidated Water operates as a comprehensive water solutions provider focused primarily on seawater reverse osmosis desalination combined with complementary infrastructure services and manufacturing:

Retail Water Operations: Under an exclusive government-issued license dating back to 1990 (now under renegotiation), Consolidated Water produces potable water for residential, commercial and governmental end-users within select territories on Grand Cayman Island. Retail sales supplied by its owned desalination plants represented roughly one quarter of total revenue but contribute nearly half of gross profits due to stable pricing structures and exclusivity protections [S1][S2][S16][S21].

Bulk Water Operations: Supplying desalinated water wholesale to government utilities primarily in the Cayman Islands and The Bahamas under long-term contracts constitutes another quarter of revenues. These government contracts require strict adherence to minimum quantity, quality, and energy consumption benchmarks; failure risks penalties or termination [S1][S20]. Bulk water plants include six production facilities in Cayman (capacity

11.6 million gallons/day) and two large-scale plants in the Bahamas (14.8 million gallons/day) [S21].Services Segment: Largest single revenue source (~35%) encompassing design, construction management, operations & maintenance (O&M) for water production, wastewater treatment, reuse infrastructure mainly across the U.S. The acquisition of Ramey Environmental Compliance expanded coverage into Colorado’s Rocky Mountain regions; ongoing project development includes Kalaeloa Desalco’s seawater desalination plant under buildout in Oahu Hawaii [S9]. Services revenue relies on contract wins and renewals with municipalities/industrial customers alongside performance guarantees.

Manufacturing Segment: Produces specialized reverse osmosis equipment through Aerex Industries located in Florida (~14% revenue). This OEM offering enhances vertical integration by supplying proprietary membrane filtration components important for both internal plant builds and external clients [S9][S21].

Complementing these segments is an affiliate interest (~45% effective equity stake) in Ocean Conversion (BVI), which supplies bulk water under contract to British Virgin Islands authorities.

Revenue mechanics largely depend on contracted volumes (either fixed or variable based on consumption metrics), pricing adjustments linked to inflation/energy costs especially for bulk operations, recurring service fees from infrastructure management deals typically structured with guaranteed performance SLAs and product sales margins from manufacturing.

Margins concentrate benefit from exclusivity rights on retail sales allowing above-market pricing power while bulk supply contracts emphasize scale efficiency offset by stricter risk-sharing clauses. Services margin generation varies contract-to-contract depending on complexity and operational cost controls. Manufacturing contributes incremental margin from customized product line specialization.

The company's liquidity benefits considerably from high cash balances supported by conservative debt levels; however significant customer payment delays remain a vulnerability especially within government counterparty-heavy segments [F1].

Industry Structure & Competitive Position

Consolidated Water occupies a unique niche at the intersection of island-based potable water supply via desalination technology combined with complementary engineering-based services focused on municipal water infrastructure.

Key competitive moats include:

Exclusive Retail License: Only licensed supplier covering critical population centers granting protected revenue streams insulated from direct competition within Grand Cayman Island sectors served.

Long-Term Government Contracts: Bulk supply agreements anchor steady demand though introduce credit concentration risk tied to public-sector payment reliability.

Geographic Diversification: Multiple Caribbean jurisdictions plus a growing U.S.-based services footprint dilutes location-specific risks such as natural disasters or regulatory changes.

Integrated Service Offering: Vertical integration from manufacturing through treatment plant design/construction to operation provides customers enhanced value propositions and switching-cost barriers versus standalone competitors.

Technology Focus: Proprietary expertise centered on seawater reverse osmosis desalination technologies capitalizes on rising global demand for clean potable alternatives amid freshwater scarcity worldwide.

Competitive challenges originate notably from:

Regulatory uncertainties particularly with OfReg aiming for revised commercial terms potentially eroding exclusivity benefits.

Credit risk inherent in government customer payment delays notably within The Bahamas segment affecting cash flow visibility.

Increasing market entry by new players offering turnkey solutions may pressure pricing over time especially outside core licensed territories.

Growth Drivers

Several factors underpin potential long-term growth:

License Renegotiation Outcome: A resolution that sustains favorable economics would preserve high-margin retail cash flow critical for capital reinvestment capacity.

Expansion into New Markets: Geographic growth opportunities enabled through acquired service companies like PERC expand presence across U.S. states targeting municipalities seeking treatment upgrades or new desalination projects.

Infrastructure Renewal Trends: Aging municipal water infrastructures across North America support steady demand for design-build-operate contracts offered by Consolidated Water’s services segment.

Environmental Regulations & Freshwater Scarcity: Increased regulation demanding higher-quality discharge standards alongside climate-driven drought pressures boost adoption of advanced treatment technologies including seawater RO solutions.

Project Pipeline Development: Active new projects such as the Kalaeloa Desalco plant create forward backlog confirming near-term booked revenues beyond typical O&M contracts which tend toward recurring service appointments.

Strategic Acquisitions: Targeted M&A focused on complementary service offerings can accelerate expansion into underserved regions or technologically adjacent areas enhancing cross-selling opportunities.

Each driver connects closely to measurable KPIs: backlog/order book growth levels largely within services segment; licensing milestones related primarily to regulatory outcomes; renewal rates/high client retention underpin stable recurring services revenues; delinquencies/receivables aging metrics signal credit environment health impacting liquidity available to fund growth investments.

Risks & Watchpoints

Disruptive risks warrant close monitoring:

Retail License Renegotiation Risk: An unfavorable outcome could lead not only to reduced profitability but potentially impair asset values requiring write-downs impacting equity capital [S2][S25].

Receivables Delinquencies: Persistently high aged accounts receivable balances within CW-Bahamas expose liquidity pressure threats undermining operational continuity absent external financial support or resolution [S2][S22].

Cost Estimation Errors: Contract margins suffer if initial bids underestimate actual materials/labor expenses especially given inflationary pressures on inputs prone to volatility affecting manufacturing/service segments [S22].

Natural Disasters: Exposure predominantly through Caribbean plant locations vulnerable to hurricanes or earthquakes capable of damaging infrastructure causing outages/recovery costs disrupting supply continuity and customer relationships [S20].

Regulatory & Environmental Changes: Potential shifts including tariffs on imported equipment components or new stringent environmental compliance rules could raise operating costs unexpectedly undermining profitability if not passed through contractual mechanisms fully [S21][S24].

Contract Terminations & Customer Concentration: Government contracts sometimes include termination-at-will clauses reducing visibility beyond short contract periods requiring continuous renewals risking lost revenues if public policies shift abruptly [S20].

Monitoring developments around OfReg negotiations specifically for updates announcements is crucial given outsized financial ramifications associated with that outcome. Equally elevated scrutiny is warranted around CW-Bahamas receivables collections trends given scale relative to that segment’s working capital requirements.

What To Watch Next

Key upcoming milestones include:

- Progress updates or final resolutions regarding OfReg negotiations expected throughout remainder of 2026 as authorities finalize licensing terms that will shape retail earnings sustainability.

- Quarterly disclosure of accounts receivable collections performance particularly for CW-Bahamas providing signals on timing and scale of any recovery required measures acting as near-term liquidity indicators.

- Order booking trends within services segment including any further expansions into US municipal infrastructure markets highlighting diversification efforts beyond Caribbean incubator markets.

- Operational progress milestones reported regarding Kalaeloa Desalco’s ongoing Hawaii desalination project reflecting capability execution track record consistency critical for competing effectively in this space long term.

- Guidance commentary issued by management post-negotiations shedding light onto forecast visibility around revenue stability and capital allocation priorities given uncertain regulatory backdrop.

Financial Profile: Strong Liquidity Amid Operating Challenges

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $126mm | |

| 2026-03-31 | ||

| Current assets | $173mm | |

| 2026-03-31 | ||

| Current liabilities | $29mm | |

| 2026-03-31 | ||

| Current ratio | 6.04x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

While operating risks have intensified recently due to regulatory renegotiations and receivable issues affecting certain segments’ cash conversion cycles,[F1] shows Conservatively Managed Capital Structure supporting overall financial flexibility:

Available cash more than quadruples short-term liabilities providing cushion against delayed collections as seen in CW-Bahamas subsidiary — critical because total debt remains very low at sub-$0.5 million level even though externally dated ([F1]). Operating income generation continues positive with net income also comfortably profitable based on latest annual aggregates suggesting underlying core business economics still intact despite episodic challenges [F1].

Disclaimer: This analysis is based solely on publicly filed documents up through May 12th, 2026, without involving any confidential information or proprietary forecasts. It is intended purely for informational purposes without investment recommendations or price speculation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments