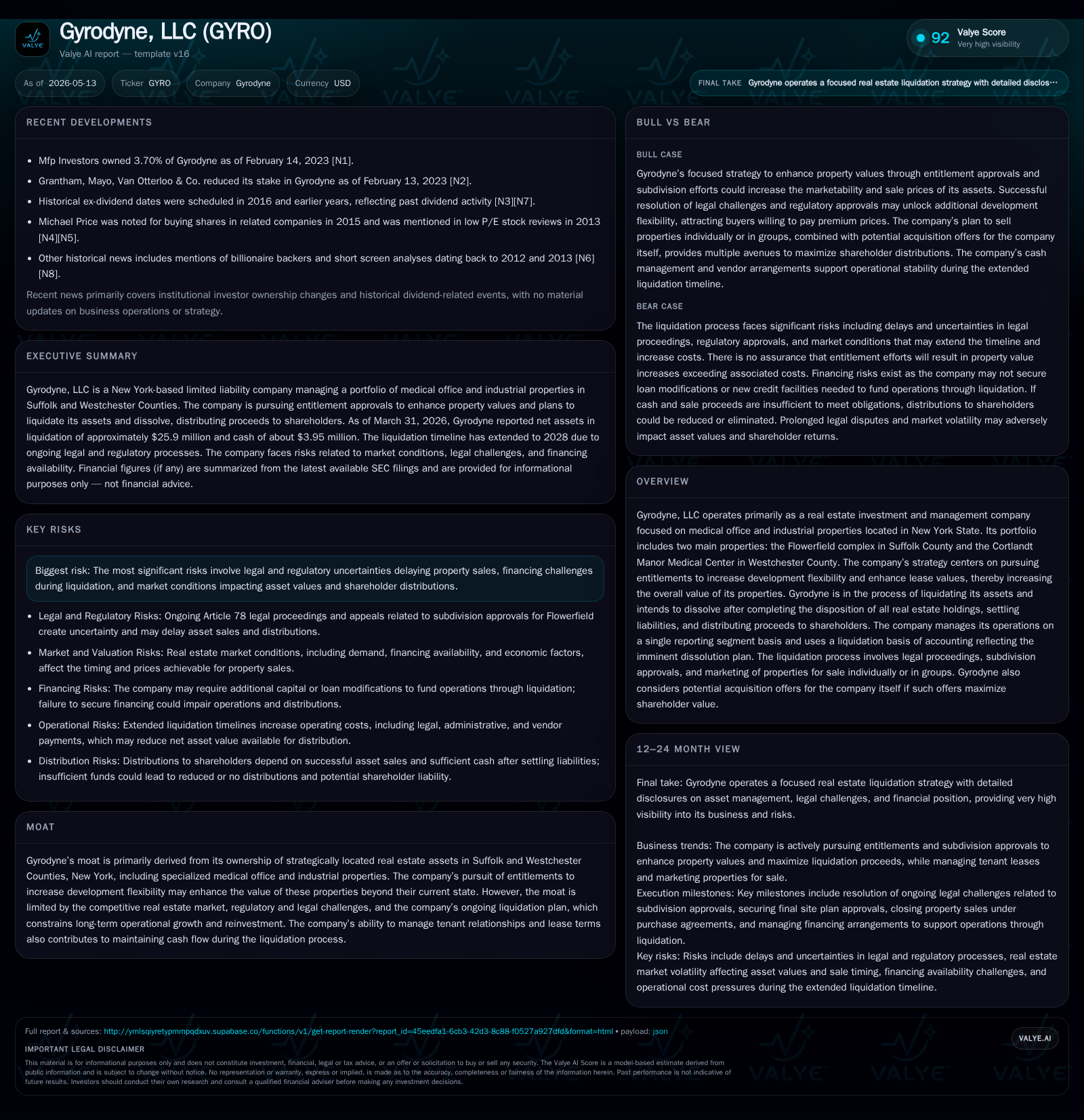

Gyrodyne’s 2026 Strategy to Maximize Asset Value Amid Liquidation

Gyrodyne is advancing entitlement approvals and managing strategic sales to enhance property value during its liquidation phase.

The May 2026 quarterly filing outlines Gyrodyne’s continued pursuit of entitlements to increase development flexibility at its Flowerfield and Cortlandt Manor properties. The company operates under a liquidation basis with a plan to dissolve after disposition of all real estate assets. Growth is anchored on subdivision approvals expected in late 2026 and 2027, alongside lease enhancements to sustain cash flow. Risks from regulatory delays, community opposition, and financing challenges remain key constraints underpinning the timeline and distributable value. The current capital structure includes approximately $10.8 million in debt offset by $4.0 million in cash, supporting ongoing operations through the liquidation horizon.

Latest Operating Update: Quarterly Filing Insights

Gyrodyne’s latest quarterly report filed May 13, 2026 [S2] reinforces the company’s core strategy focused on increasing the underlying value of its two principal properties—the Flowerfield Complex in Suffolk County and the Cortlandt Manor Medical Center in Westchester County—through entitlement achievements and lease term enhancements. The company expects subdivision approval for Flowerfield by Q3 2026 with Cortlandt Manor’s anticipated in 2027, though these timelines remain sensitive to zoning backlogs, labor shortages within local planning authorities, and environmental review challenges.

Operating under a single reporting segment given its streamlined portfolio management during liquidation, Gyrodyne continues marketing efforts while conducting negotiations aimed at maximizing sale values through enhanced development flexibility offered by successful entitlement milestones. This orderly disposition plan conforms to their accounting policy applying the liquidation basis reflecting an imminent corporate dissolution following complete asset divestiture.

Business Model: Real Estate Focus with Medical and Industrial Leases

Gyrodyne functions effectively as a specialized real estate investment manager concentrating on medical office buildings and industrial properties situated within New York State’s regulatory landscape [S1][S12]. Its revenue generation hinges predominantly on leasing these properties to diversified tenants including healthcare providers affiliated with Stony Brook University Hospital at Flowerfield and multiple healthcare services operators at Cortlandt Manor.

Most leases incorporate provisions where tenants reimburse the company for utilities, insurance, maintenance, repairs, and real estate taxes that otherwise shift landlord cost exposure downward—critical in preserving cash flow during a drawn-out liquidation process [S1]. Property valuation enhancement derives from securing land-use entitlements that expand potential development scenarios for prospective buyers, thereby driving higher sale prices upon portfolio disposition [S1]. Nonetheless, the company explicitly warns that resultant value additions may not surpass incremental entitlement investment costs.

Competitive Positioning and Industry Structure in New York Real Estate

Within Suffolk and Westchester counties’ fragmented real estate markets where demand sustains specialized medical office properties alongside industrial spaces supporting regional commercial activity [S1], Gyrodyne’s assets occupy strategic positions enabling targeted lease revenue streams. However, execution complexities arise from entrenched local regulatory environments characterized by protracted zoning approvals exacerbated by public sector labor constraints [S2].

Community activism further complicates entitlement progress. Opposition groups have raised concerns about environmental impacts, increased traffic congestion, and preserving historical site integrity around the Flowerfield subdivision proposal—a factor provoking Article 78 legal actions challenging prior approvals [S1]. These dynamics heighten the risk profile relative to competitors who may enjoy scale or flexibility advantages absent such persistent localized resistance.

Nonetheless, tenant switching frictions due to infrastructure specialization—especially among regulated healthcare service providers requiring specific facility standards—helps stabilize occupancy levels despite overall market uncertainties.

Growth Drivers: Entitlement Approvals and Lease Enhancements

The primary growth levers reside in successful receipt of subdivision approvals facilitating greater lot-level transaction flexibility at Flowerfield slated for Q3 2026 [S2], enabling parcel sales aligned with developer intentions. Similar land-use optimizations at Cortlandt Manor forecasted for 2027 would unlock latent property value but are subject to heightened timing risks given legal proceedings.

Parallel efforts target enhancing lease profiles via proactive early renewals and attracting new tenants or expanding existing ones to reduce vacancy durations amid asset disposition phases [S1]. This lease pipeline management is vital not only for maintaining predictable cash flows but also sustaining property valuations until eventual sale consummation.

Each entitlement milestone acts as a potential catalyst recalibrating appraisals upwards, thereby increasing prospective sale proceeds available for shareholder distributions [S19]. The company's marketing partnership with JLL undertakes national outreach to identify purchasers attuned to acquiring partially entitled parcels or entire complexes contingent on regulatory outcome clarity.

Risks and Constraints: Regulatory, Legal, and Market Challenges

Gyrodyne operates under significant regulatory uncertainty risks amplified by ongoing Article 78 litigation targeting the Flowerfield subdivision endorsement which threatens delays or potentially reversals impairing strategic timelines [S1]. Environmental permitting hurdles coupled with community activism centered around traffic impact studies impose additional bottlenecks requiring time-consuming mitigations.

Financial constraints are material given reliance upon debt facilities secured against underlying assets; inability to refinance or modify existing loans favorably could stress liquidity especially amid prolonged entitlement horizons [S16][S23]. Moreover, mandatory credit terms include prepayment penalties linked to mortgage loans constraining flexible deleveraging options before maturity phases ending October 2026 (with possible extensions) [S2].

Furthermore, macroeconomic factors such as elevated interest rates, inflation persistence, residual COVID-19 pandemic effects on office leasing patterns, and regional recession risks compound valuation uncertainties diminishing sell-side momentum.

These combined risks introduce potential variance between estimated net realizable asset values reflected in financial statements under liquidation accounting versus ultimate cash proceeds realizable for shareholders [S5][S18].

Key Near-Term Watchpoints: Approvals, Sales Progress, and Cash Flow

Investors should monitor several upcoming milestones closely including:

- Confirmation of Smithtown Planning Board approval for Flowerfield subdivision anticipated in Q3 2026 which directly impacts the execution of the B2K purchase agreement valued up to approximately $28.7 million subject to final site plan approvals [S19].

- Progress toward rezoning or entitlement refinements at Cortlandt Manor expected through calendar year 2027 given elongated timelines influenced by external opposition [S2].

- Leasing activity updates such as new tenancy agreements signed post-2025 year-end that may improve occupancy metrics during disposition phases [S13].

- Updates regarding litigation outcomes stemming from Article 78 proceedings capable of materially affecting timing or sale terms [S1].

- Debt facility modification negotiations as the current mortgage maturities approach October 2026 with penalties imposed on early prepayments yet some extension option available affecting refinancing flexibility [S2][S27].

- Cash flow adequacy measured against ongoing operating expenses including legal fees linked to entitlement contests crucial to sustaining the company’s operations through forecasted liquidation completion by end-2028 [S8][S14].

Financial Snapshot: Capital Structure and Liquidity Status

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3.95 million | |

| 2026-03-31 | ||

| Total debt | $10.79 million | |

| 2026-03-31 | ||

| Net debt | $6.84 million | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026, Gyrodyne reported cash and cash equivalents totaling approximately $3.95 million alongside total debt obligations near $10.79 million yielding net debt around $6.84 million using latest XBRL data validated via quarterly filings [F1][S2].

The capital stack includes:

- A $4.95 million mortgage loan initiated September 15, 2021 with Signature Bank (now Rialto Capital), bearing annual interest of 3.75%, maturing October 10, 2026 with an option to extend five years subject to interest rate resets; prepayment penalties range from five percent (first year) declining annually thereafter if prepaid early [S2][S27].

- A $1.5 million term loan secured December 27, 2023 from LLYR Resources utilized primarily for working capital needs [S2].

- Outstanding non-revolving credit lines related to Flowerfield industrial park financing maturing through mid-2028 at fixed rates ~3.85% plus amortization schedules detailed in earlier disclosures yet anticipated for modification following subdivision completions [S20][S21].

All forward-looking statements are subject to inherent uncertainties outlined within company disclosures.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments