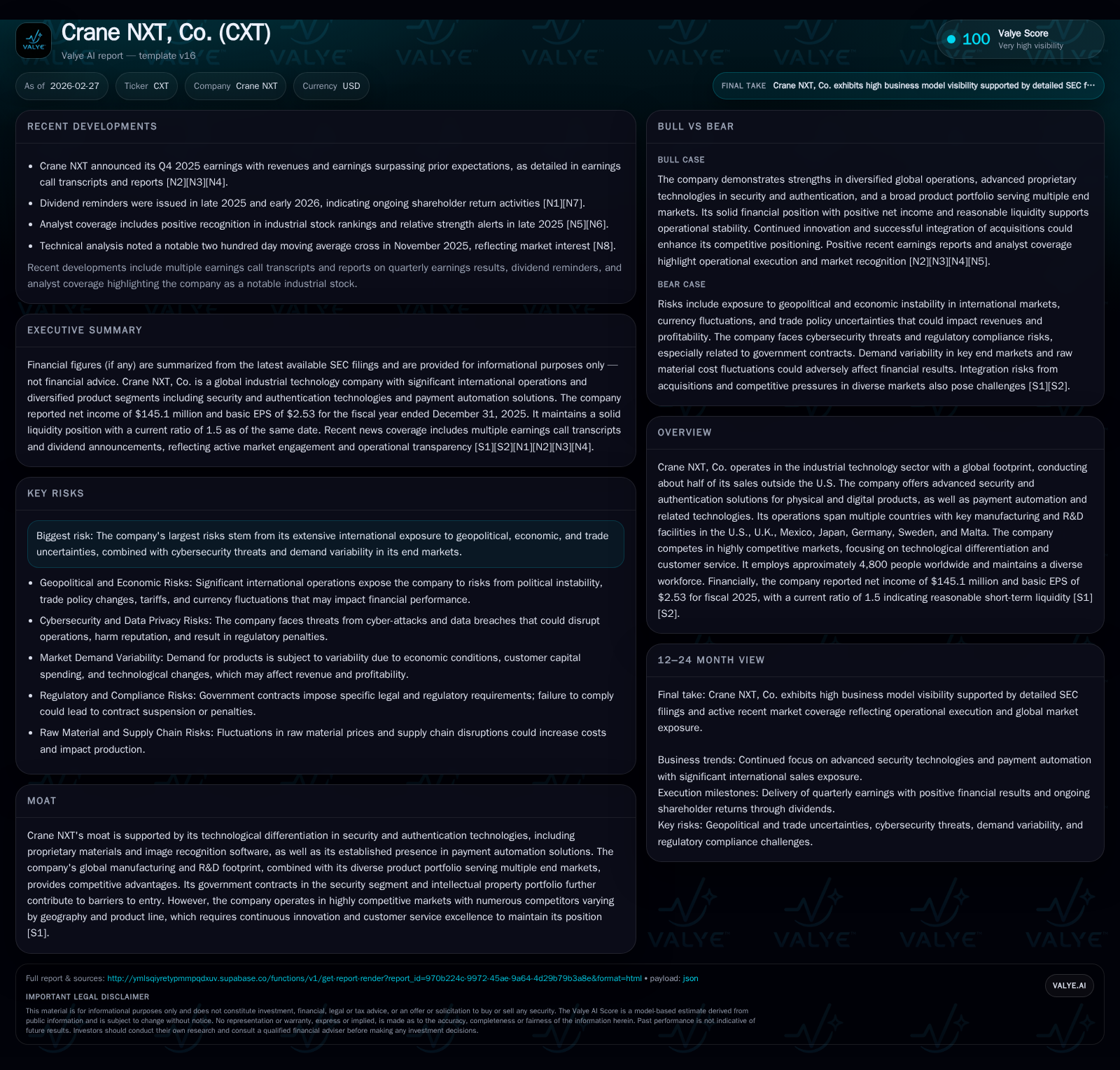

Crane NXT's Shifting Growth and Profitability Dynamics in 2025

Robust revenue growth in 2025 contrasts with operating income decline amid rising global risks and competitive pressures.

Crane NXT, Co. reported a remarkable 338% surge in revenue for fiscal 2025 driven by expansion in its security and payment automation segments and international markets. However, operating income contracted by 8.2% year-over-year, pressured by escalating costs, geopolitical uncertainty, and investment in product innovation. The company’s global footprint exposes it to currency fluctuations and trade tensions that complicate profitability management. Capital allocation reflects strong cash flow generation but a more cautious stance on buybacks despite stable dividend payouts. Key future catalysts include contract awards in security technologies and navigating tariffs impacting its Mexican manufacturing hub.

Revenue Surge and Historical Growth Trends

Fiscal year 2025 marked a watershed moment for Crane NXT with revenues leaping to approximately $3.37 billion, representing a striking year-over-year increase of 338% compared to fiscal 2024 [F1]. This surge followed periods of significant volatility between fiscal years 2019 to 2024 where revenue oscillated between roughly $770 million (FY2021) and near $3 billion (FY2020). The rebound suggests successful scaling particularly in core divisions encompassing security authentication technologies (SAT) and payment automation solutions [S1][S11]. Geographic expansion likely contributed alongside new product introductions leveraging proprietary image recognition algorithms.

This marked acceleration signals the company's capitalizing on rising demand for advanced anti-counterfeiting solutions amid global concerns about product authenticity and digital payment innovations that streamline transaction automation.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 145 | 242 | 247 | 43 | -21.2% |

| 2024 | 184 | 214 | 269 | 45 | -2.2% |

| 2023 | 188 | 276 | 287 | 31 | -53.1% |

| 2022 | 401 | -152 | 370 | 58 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 39 | 198 | 11.6 |

| 2024 | 37 | 169 | 17.3 |

| 2023 | 24 | 245 | 19.5 |

| 2022 | 106 | -210 | 21.1 |

Source: SEC companyfacts cache [F1].

Operating Income Decline: Exploring Underlying Factors

Despite top-line strength, Crane NXT experienced an operating income dip of approximately 8.2%, settling at $246.7 million for FY2025 [F1]. This divergence underscores margin compression attributable to a confluence of factors: intensified competition among global peers applying downward pricing pressure; elevated costs from raw material inflation; supply chain disruptions; and strategic ramp-up in R&D supporting next-gen authentication technologies [S1][S16].

Management commentary highlights investments aimed at sustaining technological differentiation through proprietary materials and algorithmic advancements which naturally weigh on short-term profitability but are expected to fortify the moat long term [S1]. Industry dynamics also suggest operating leverage challenges manifest when rapid revenue increase coincides with higher variable cost structures.

Global Footprint Risks and Market Dynamics

Crane NXT’s extensive international presence means approximately half its sales derive from outside the United States, exposing operational performance to complex geopolitical risks including economic instability, foreign exchange volatility predominantly involving Japanese yen, British pound, euro, and Swedish krona, as well as evolving trade policies [S6][S7][S8][S15].

The company benefits operationally from Mexico-based manufacturing facilities participating under the Maquiladora program—a key tariff-reducing mechanism facilitating lower-cost assembly for export products—but is not insulated from U.S.-Mexico trade tensions or potential tariff escalations [S6][S17]. The broader environment includes cybersecurity threats affecting both internal systems and client-facing solutions given the sensitive nature of authentication services.

Currency swings affect reported USD results given translation exposure; combined with tariff-driven cost uncertainties, these factors contribute volatility to margins despite pricing initiatives geared toward offsetting tariff impacts [S1][S17].

Technological Moat and Competitive Differentiation

Crane NXT maintains a defensible position through its portfolio of differentiated technologies which comprise advanced proprietary materials used for anti-counterfeiting printing and surface applications along with sophisticated image recognition software facilitating digital authentication across physical goods and online platforms [S1][S11]. It leverages an IP-rich environment with numerous patents protecting innovation in both security printing for banknotes and brand protection for consumer goods.

Government contracts provide additional entry barriers due to compliance demands including disclosure requirements and sourcing conditions unique to public-sector deals [S7]. This mix of high-tech product specialization coupled with strict regulatory adherence fosters customer lock-in while competitive peers vary widely across geographies.

Strategic Outlook: Growth Prospects and Industry Challenges

Looking ahead, Crane NXT faces opportunities fueled by accelerating digital payment adoption and sustained government spending on secure currency production aligned with anti-fraud initiatives [N1][N3][S1]. The company actively pursues enhancements in payment automation technologies aimed at retail vending sectors whose profitability depends on fuel prices, credit availability, and innovative financing models that impact equipment upgrades [S8].

Challenges emanate from cyclicality tied to end-market demand—particularly in gaming and retail where discretionary spending affects purchase plans—and macroeconomic uncertainties including inflationary pressures dampening capex cycles among customers [N2][S1][S18]. Pursuit of product innovation remains critical yet costly given the pace required to maintain technological edge amid competitive intensity.

Capital Allocation Priorities: Dividends, Buybacks, and Cash Flow Analysis

Crane NXT reported operating cash flow growth to roughly $241.5 million in FY2025 representing a 12.8% uplift compared to FY2024, highlighting solid cash generation capabilities despite margin headwinds [F1]. Capital expenditures were moderated at $43.2 million, slightly down from prior years, sustaining investment without excess capex build-up.

Applying this cash flow profile yields free cash flow near $198 million enabling shareholder distributions alongside strategic reinvestments [F1]. Dividends increased moderately to approximately $39 million paid out during the year reflecting confidence in sustainable earnings streams while share repurchases saw a marked reduction post a peak buyback phase around FY2022 [$204M repurchased], indicating a shift toward conserving liquidity amid global uncertainty [F1][S4][S5].

Equity balances diminished relative to previous highs culminating at about $1.25 billion for FY2025 with an approximate return on equity calculated near 11.6%—consistent with mid-tier performance metrics typical within industrial technology cohorts balancing growth investment against risk mitigation [F1]. Liquidity remains adequate demonstrated by a current ratio around 1.5 offering reasonable short-term asset coverage against liabilities [F1][S4].

What to Watch: Key Milestones and Market Signals

Investors should monitor several pivotal developments over forthcoming quarters including the cadence and size of contract awards particularly within the Security Authentication Technologies segment serving central banks whose procurement timelines substantially influence quarterly revenue patterns [N1][N3]. Additionally, watch for any policy shifts impacting trade relations especially concerning Mexico operations where the Maquiladora benefits heighten exposure to tariff alterations or regulatory tightening [N1][N3][S6].

Quarterly earnings updates will be important barometers validating assumptions regarding pricing power retention versus inflationary cost pass-through effectiveness amidst volatile forex conditions.

The execution pace of new product launches integrating cutting-edge image recognition enhancements will also signal management's ability to sustain competitive advantages required in their multifaceted markets.

This analysis is rooted strictly in publicly available financial disclosures as of the latest fiscal year-end filings combined with recent earnings commentary; it does not incorporate speculative forward projections beyond documented guidance or observed market conditions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments