Diebold Nixdorf’s Resilient Revenue Growth Faces Profit and Liquidity Pressures in Early 2026

Despite surpassing Q4 revenue expectations, Diebold Nixdorf contends with margin compression and liquidity challenges amid volatile market sentiment.

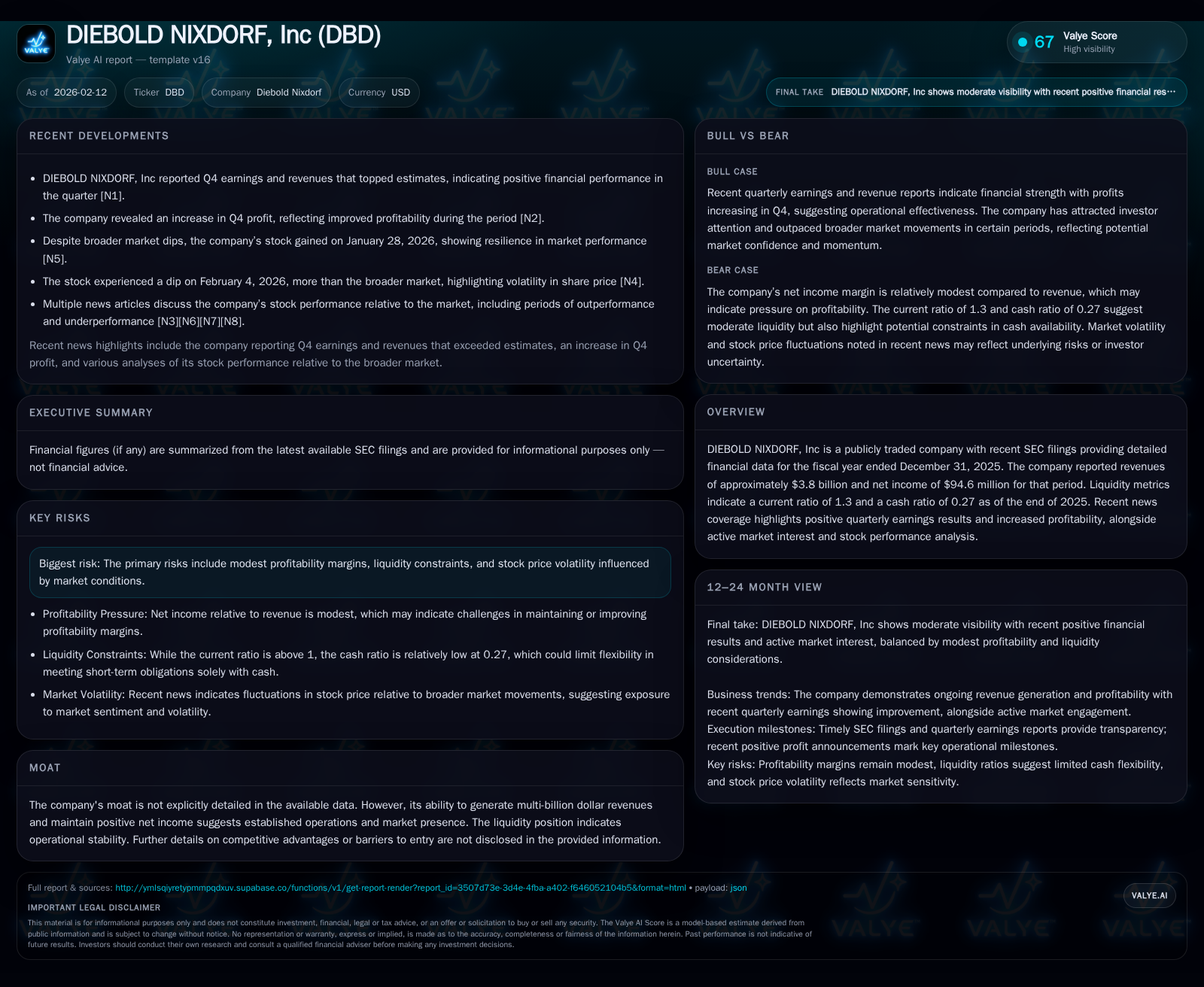

Diebold Nixdorf closed fiscal 2025 with revenues near $3.8 billion and a net income of approximately $94.6 million, exceeding recent quarterly expectations. However, profitability margins remain modest relative to top-line growth, highlighting operational and cost pressures. Liquidity ratios indicate adequate but constrained financial flexibility, contributing to ongoing investor caution reflected in stock volatility. The company's sizeable operational scale suggests an implicit competitive moat, even as Wall Street perspectives balance bullish outlooks against discernible risks ahead.

Surpassing Q4 Expectations: Revenue and Profit Highlights

Diebold Nixdorf's most recent earnings report for Q4 and the full fiscal year ended December 31, 2025, delivered a welcome surprise to markets by beating revenue and profit expectations. The company generated approximately $3.8 billion in total revenue for the year [F1], underpinned by increased sales activity across its product and service segments. Net income reached about $94.6 million [F1], representing an uptick compared to prior quarters and surpassing analyst forecasts reported in February 2026 news [N1][N2]. This top-line strength has arguably been the cornerstone event galvanizing market interest in early 2026.

The earnings beat signals that Diebold Nixdorf could manage steady demand dynamics within its end markets despite broader economic uncertainties impacting technology and financial services sectors where it operates [N1]. However, while revenues showcased resilience, the path beyond topline momentum reveals some underlying complexities impacting profit realization.

Profitability Under the Microscope: Challenges Amid Growth

Diving deeper into profitability paints a more nuanced picture. The company’s net income margin remains slim considering the magnitude of revenue—less than 2.5% when comparing net income against total revenues of nearly $3.8 billion [F1]. This relatively modest profitability highlights persistent cost structures or pricing pressures that have circumscribed expanded earnings leverage even as sales volumes rose.

According to disclosures in the latest SEC 10-K filing [S1], Diebold Nixdorf acknowledges risks tied to margin compression driven by competitive pricing environments, rising input costs, and investments to support digital transformation initiatives essential for future growth. These initiatives while important can blunt near-term profit expansion as spending prioritizes innovation and infrastructure over immediate earnings gains.

Such challenges underscore the difficulty of sustaining improved net margins when balancing growth investments with ongoing operational expenses—a reality routinely emphasized in their risk factors section [S1]. Maintaining earnings robustness amidst these pressures will require effective cost management and potentially strategic reprioritization moving forward.

Liquidity and Financial Health: Stability or Constraint?

On the liquidity front, Diebold Nixdorf’s balance sheet portrays a position of operational adequacy yet with signs that financial flexibility is not overly abundant. The current ratio stands at about 1.3 as of December 31, 2025 [F1], indicating the company holds sufficient current assets ($1.79 billion) relative to current liabilities ($1.37 billion) to cover short-term obligations comfortably but without a large buffer.

More critical is the cash ratio of roughly 0.27, reflecting that immediately liquid assets (cash & equivalents around $369 million) cover only about a quarter of short-term liabilities [F1]. This constrained cash cushion points to reliance on receivables or other current assets for meeting near-term commitments. Management commentary in the MD&A section of the recent filing discusses this aspect cautiously, noting capital allocation decisions must carefully balance operational needs against debt servicing and investment plans [S1].

While no acute liquidity crisis appears imminent, these ratios emphasize the importance of efficient working capital management and possible sensitivity to any abrupt cash flow disruptions or macroeconomic shocks.

Market Pulse: Stock Volatility Amid Mixed Sentiment

Reflecting these fundamental dynamics is notable stock price volatility that has punctuated Diebold Nixdorf’s trading activity during early February 2026. Several Nasdaq reports chronicle episodes where DBD shares outpaced general market gains following positive earnings releases [N9][N10], but also moments where stock dipped significantly despite broader indices rallying [N4][N7].

Such swings suggest investors are parsing positive quarterly earnings surprises through a lens tinted by cautious scrutiny of margin sustainability and liquidity considerations [N5]. The trending nature of the stock embodies heightened speculative interest—as well as underlying indecision—about how well future performance drivers can manifest.

Contributing macro factors include ongoing global economic uncertainties affecting technology adoption cycles in banking infrastructure markets where Diebold Nixdorf primarily operates. These external conditions amplify sentiment oscillations despite encouraging company-specific headlines.

Competitive Positioning: Moat Implied Through Operational Scale

Though no explicit narrative around a durable competitive moat is presented in public disclosures or analyst commentary, Diebold Nixdorf’s consistent generation of multi-billion dollar revenues combined with positive net income indicates established market presence and operational scale provide implicit barriers against smaller rivals.

The company operates within specialized niches including ATM manufacturing, banking automation solutions, and secure transaction technologies—which benefit from long-standing client relationships and integration complexity that typically raise entry hurdles for new competitors [valye_report_excerpt]. Its scale facilitates breadth across products and geographies that simultaneously drives cost efficiencies and customer stickiness.

While intangible moat factors like brand recognition or proprietary IP specifics are not clearly detailed, such persistent operational capacity alongside continued revenue growth hints at competitive advantages grounded largely in market positioning rather than disruptive innovation presently.

Wall Street Takes: Bullish Sightlines Versus Risk Factors

Investor-facing narratives balance optimism with caution. Analyst coverage referenced in Nasdaq insights highlights bullish sentiment fueled by top-line growth momentum and recent earnings beats [N3]. Some optimistic views focus on anticipated benefits from ongoing digital transformation initiatives embedded within Diebold’s strategy roadmap.

Simultaneously, company-acknowledged risks outlining margin pressures, liquidity constraints, and stock price volatility temper unbridled enthusiasm [S1]. This duality shapes a market landscape where buy-side stakeholders weigh durable revenue foundations against challenges in converting growth into meaningful bottom-line expansion and managing capital effectively under fluctuating conditions.

These contrasting perspectives have shaped diverse investor convictions seen in share price fluctuations—reflecting varying interpretations of risk-reward balance plus timing for re-rating given execution uncertainties.

Strategic Outlook: What Lies Ahead for Diebold Nixdorf?

Strategically, management disclosures shed light on the balancing act faced going forward—continuing investments aimed at enhancing product offerings and expanding digital services while addressing margin pressures through efficiency improvements [S1][N1]. The company articulates intent to leverage technology modernization across core banking automation systems alongside service portfolio enhancements designed to capture evolving client requirements.

Recent earnings commentary suggests focus areas include optimizing supply chain responsiveness, scaling software-driven solutions with higher recurring revenue potential, and rationalizing fixed costs aligned with strategic priorities [N1]. Capital allocation will likely be cautious given liquidity constraints but aims at sustaining innovation capabilities needed for competitive differentiation.

Execution efficacy here will be pivotal; success may unlock improved profitability metrics consistent with sustained revenue trends observed thus far while failure necessitates potential strategic recalibrations.

Investor Takeaway: Weighing Promise Against Perils

Synthesizing these facets reveals a company with credible topline growth demonstrating resilience despite operational headwinds limiting margin advancement—an interplay central to gauging future value creation prospects for shareholders.

Liquidity metrics point toward stable yet tight capital positions requiring ongoing vigilance to forestall adverse impacts from any unforeseen stressors affecting cash flows or debt servicing ability. Market reactions underscore an environment rife with uncertainty where positive news triggers enthusiasm but does not fully dispel concerns about sustainable profit expansion amid evolving macroeconomic challenges.

Investor discourse captured in recent analyses debates if current valuation levels present timely buy opportunities versus calls for patience awaiting clearer margin improvement signals [N8][N11]. This tension reflects inherent complexities embedded within Diebold Nixdorf’s transitional phase: robust sales momentum paired with deliberate efforts needed to extract fuller earnings potential within defined financial constraints.

Ultimately, stakeholders engaging with Diebold Nixdorf must navigate this dynamic landscape—balancing confidence drawn from demonstrable growth achievements against measured caution prompted by structural profit limitations and liquidity management needs highlighted consistently across filings and market commentary.

Disclaimer: This analysis is for informational purposes only and does not constitute investment advice or recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments