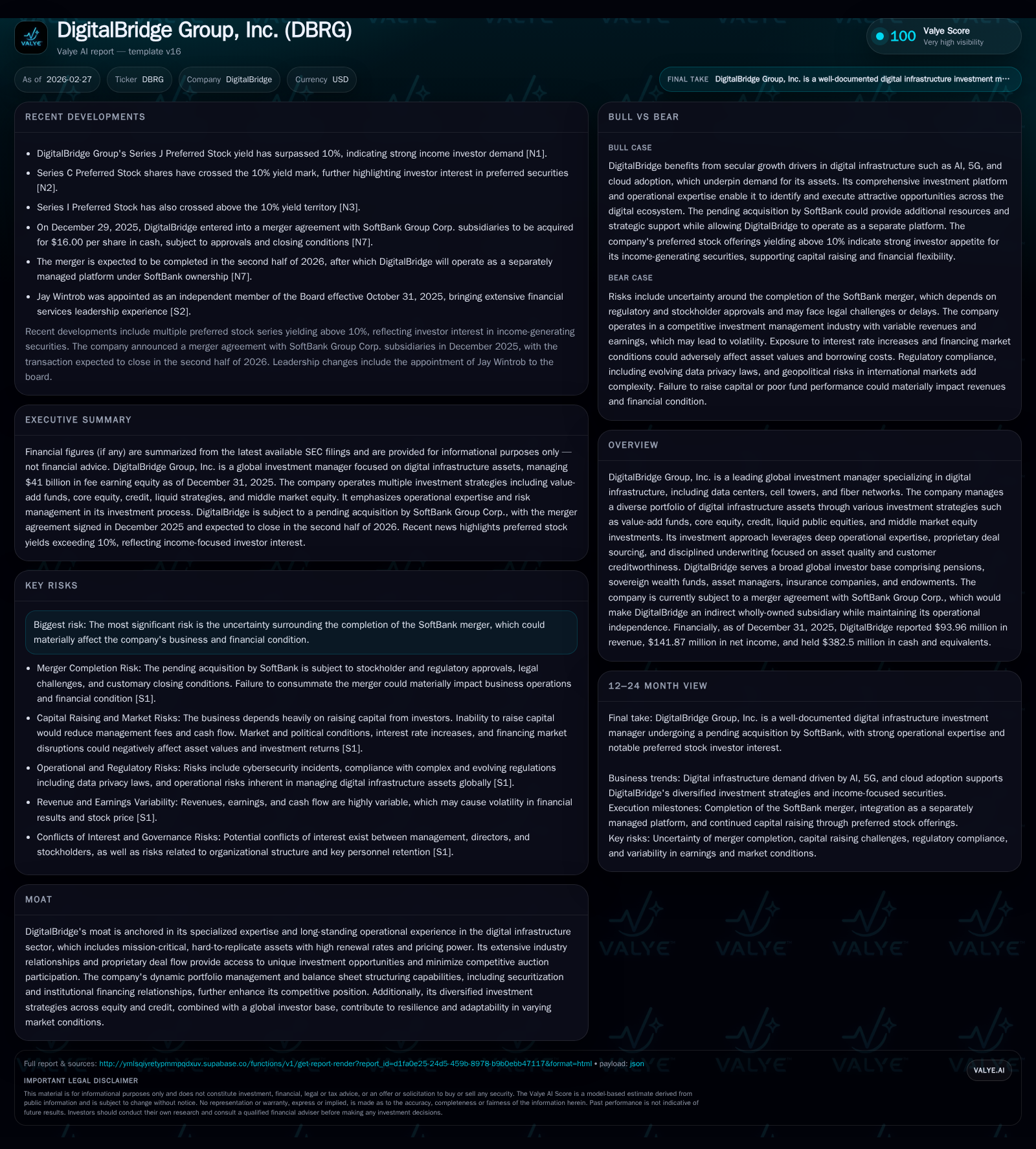

DigitalBridge Group’s Revenue Collapse and Strategic Resilience in 2025

Despite an 84.5% plunge in revenue during 2025, DigitalBridge fortified its cash flow and net income amid market challenges and merger uncertainties.

In fiscal year 2025, DigitalBridge Group, Inc. experienced a dramatic revenue decline from $607 million in 2024 to just under $94 million — an 84.5% year-over-year drop — yet managed to nearly double its net income and post a more than threefold increase in operating cash flow. This paradox reflects the firm's operational discipline, leveraging asset quality, underwriting rigor, and capital structuring expertise within its digital infrastructure investment strategies. The ongoing merger with SoftBank introduces material execution risks, though DigitalBridge’s entrenched relationships and proprietary deal flow buttress competitive positioning. The firm maintained prudent capital allocation with sustained dividends but no share repurchases, pointing to conservative stewardship amid industry headwinds and regulatory scrutiny.

Sharp Reversal in Revenue Amid Digital Infrastructure Market Dynamics

DigitalBridge Group faced a precipitous revenue contraction during fiscal year 2025 when total reported revenues shrank by approximately 84.5%, plunging from $607 million in 2024 to just about $94 million in 2025 [F1]. This unusually steep drop contrasts with a simultaneous doubling of net income to nearly $142 million over the same period — a rare occurrence that signals significant earnings volatility within the firm’s operating model.

This disparity likely reflects changes in fund performance fees tied to investment realizations or dispositions along with episodic recognition of earnings components not directly correlated with top-line assets under management growth. The sharp revenue decline could be attributable partly to lowered management or incentive fees as capital raising slowed under challenging market conditions or strategic rebalancing of investment vehicles [S1]. However, the firm's ability to report positive net income despite the collapse underscores cost controls and profitable asset-level performance.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 94 | 142 | 259 | 1 | -84.5% | +101.2% |

| 2024 | 607 | 71 | 60 | 4 | -26.1% | -61.9% |

| 2023 | 821 | 185 | 234 | -28.2% | +157.6% | |

| 2022 | 1145 | -322 | 263 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 7 | 258 | |

| 2024 | 7 | 0 | 57 |

| 2023 | 6 | 0 | |

| 2022 | 2 | 55 |

Source: SEC companyfacts cache [F1].

Revenues contracted by four-fifths while net income rebounded sharply. Negative net income in FY2022 reflects prior impairments or significant charges.

Driving Factors Behind DigitalBridge’s Operational Cash Flow Surge

While revenue collapsed in fiscal year 2025, DigitalBridge’s operating cash flow experienced an extraordinary surge of over 331%, jumping from roughly $60 million in the prior year to nearly $260 million [F1]. This remarkable cash generation improvement was coupled with sharply reduced capital expenditures: down over 60% year-over-year to just $1.35 million.

The combination highlights DigitalBridge’s exceptional ability to convert earnings into real cash flows through disciplined portfolio management within the digital infrastructure sector [S4–S6]. Key factors include:

- Rigorous underwriting emphasizing asset quality measures such as location advantage, replacement costs, and high renewal rates underpin sustainable recurring revenues.

- Detailed credit analysis targeting counterparties with strong financial profiles and long-duration contractual arrangements reducing default risk.

- Active portfolio company engagement leveraging operational expertise to enhance cash flows while managing cost of capital through tailored financing structures.

- Use of structured debt products featuring seniority and covenant protections allowing downside loss mitigation.

These dynamics reflect a sophisticated approach blending investment discretion with asset-level operational control fundamental to resilient cash flow profiles despite top-line pressure.

Navigating Uncertainty: Impact and Implications of the SoftBank Merger Deal

DigitalBridge is currently engaged in a definitive merger agreement whereby it will become an indirect wholly owned subsidiary of SoftBank Group Corp., maintaining operational independence post-close [N2, S1]. The transaction remains subject to significant uncertainty regarding completion timing or potential termination.

The protracted deal timeline has introduced several risk vectors:

- Investor apprehension around merger closure may dampen capital raising or management fee growth just as external market volatility challenges asset valuations.

- Retention of key executives and senior investment personnel hinges partly on clarity about future organizational structure and incentives.

- Litigation risks arise from shareholder challenges potentially disrupting the agreed terms or delaying consummation [S7–S9].

- Competitive positioning must be balanced against potential shifts in business strategy post-merger integration.

Given these structural risks embedded within pending M&A activity, maintaining steady operations while managing stakeholder expectations is imperative for preserving firm value ahead of close.

Capital Discipline, Leverage, and Structuring: The Backbone of Portfolio Management

DigitalBridge employs nuanced capital structuring emphasizing prudential leverage calibrated to align with risk profiles and underlying asset cash flow characteristics [S4–S6]. This involves:

- Structuring debt investments with seniority focus ensuring priority claims on borrower capital structure for downside protection.

- Deploying securitization mechanisms pioneered by senior team members that optimize leverage capacity while controlling interest costs via fixed rate instruments with favorable amortization schedules.

- Continuous monitoring of portfolio diversification across sectors and geographies to avoid concentration risk.

- Regular dialogue with borrowers supporting dynamic credit risk adjustments through quarterly reviews enabling proactive loss mitigation efforts.

This strategic use of layered financing solutions coupled with diligent portfolio oversight constitutes a core pillar sustaining DigitalBridge's investment platform resilience amid shifting market conditions.

Returns Snapshot: ROE, Dividends, and Shareholder Value Considerations

Despite volatility in earnings streams over recent years, DigitalBridge reported an approximate return on equity (ROE) of about 6.7% for fiscal year 2025 based on net income relative to equity base approximated at $2.11 billion [F1]. This accrual was complemented by dividend payments totaling roughly $7.15 million amidst no share buybacks since FY2023 signaling controlled capital distribution policies during a transitional phase.

This modest but positive return profile underscores balanced stewardship prioritizing liquidity maintenance—highlighted by ending cash and equivalents exceeding $382 million—to underpin ongoing operations and investment funding needs given uncertain near-term corporate developments.

Industry Positioning Leveraging Hard-to-Replicate Assets and Sector Relationships

DigitalBridge's moat derives largely from its specialized expertise managing mission-critical digital infrastructure assets—data centers, cell towers, fiber networks—characterized by high market entry barriers due to their hard-to-replicate nature and high contractual renewal rates conferring significant pricing power [S6, S13].

Complementing asset quality is deep operational experience cultivating enduring partnerships across leading global carriers, hyperscale cloud providers, and content companies forming its client base. This network fosters proprietary deal sourcing often circumventing more competitive auction environments thus preserving return thresholds.

Additionally, institutional relationships facilitating securitization issuances enable innovative capital access enhancing balance sheet efficiency across portfolio companies enabling tactical agility uncommon among peers within digital ecosystem investing spaces [S20].

Risks in Litigation, Regulatory Environment, and M&A Execution

The most prominent risk for DigitalBridge remains uncertainty surrounding completion of the SoftBank merger including possible legal challenges delaying or preventing closing that would impose substantial business continuity risks alongside financial burdens related to termination fees if qualifying conditions arise [S1].

Moreover:

- Ongoing litigation exposure includes shareholder derivative suits typical during transformative transactions which absorb managerial focus and escalate defense costs but entail unpredictable outcomes potentially impacting stock valuation [S7–S9].

- Regulatory scrutiny spans extensive jurisdictional compliance mandates covering anti-corruption laws (e.g., FCPA), anti-money laundering initiatives and evolving data privacy regimes such as GDPR adding complexity especially given DigitalBridge’s multinational footprint [S19–S25].

- The private investment fund industry focus from watchdogs like SEC assessing fee disclosures and governance heightens operational compliance demands potentially resulting in monetary penalties or reputational damage notwithstanding corrective efforts implemented historically [S10,S14].

- Talent risk arises as prolonged transactional ambiguity may erode key personnel retention critical for sustaining specialized relationship-driven deal origination capabilities essential for competitive positioning.

Overall these regulatory and litigation factors constitute notable headwinds requiring diligent risk management alongside strategic communication with stakeholders.

Disclaimer: This analysis synthesizes publicly available filings as of February 27, 2026 alongside recent news reports without extrapolating unaudited forward-looking statements or independent forecasts. It aims solely to provide investors with context for DigitalBridge’s financial performance within its evolving corporate structure environment absent conjectural investment guidance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments