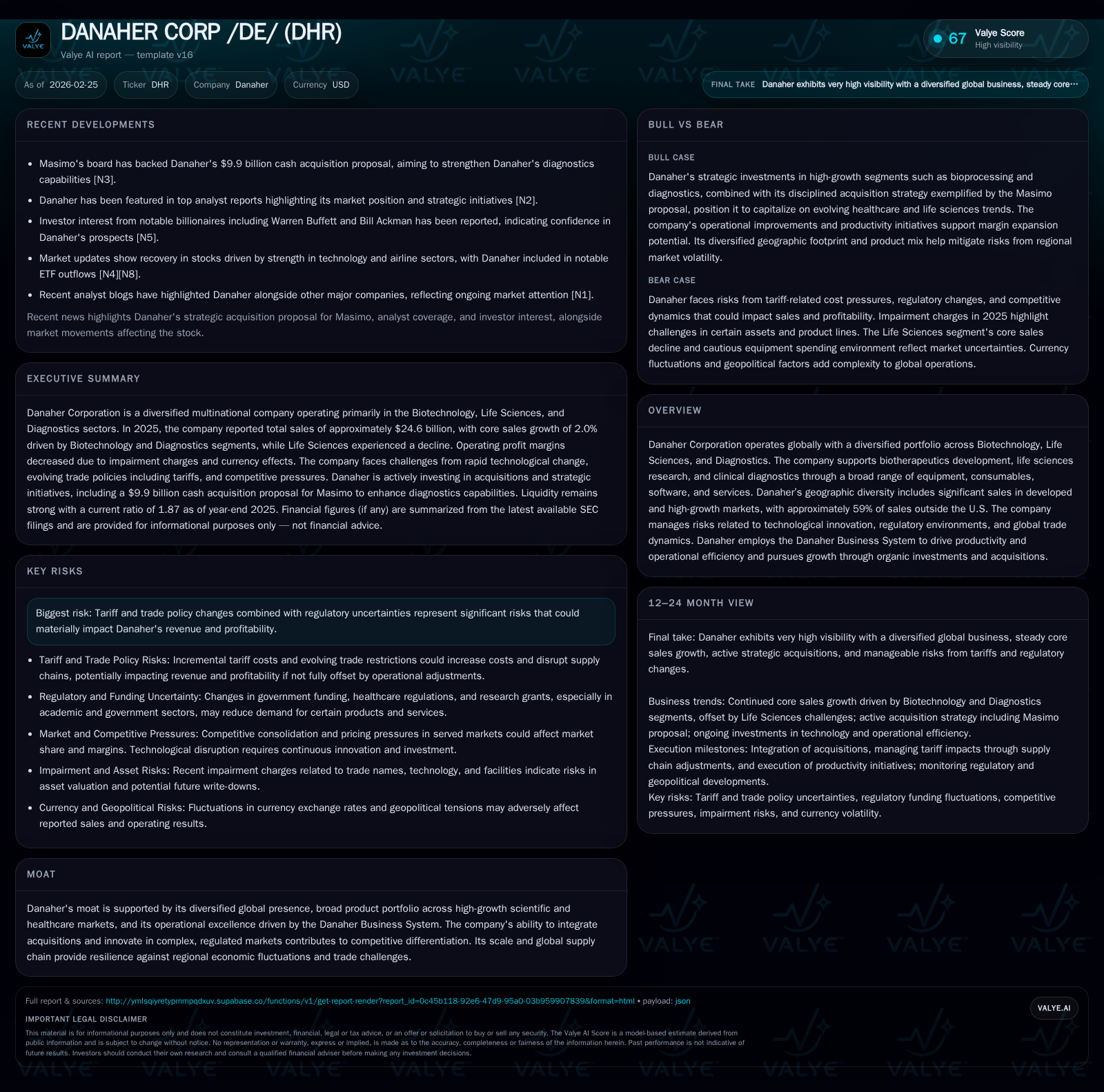

Danaher’s Growth and Margin Dynamics Amid $9.9 Billion Masimo Acquisition and Trade Cost Pressures

Danaher navigates moderate organic growth, margin headwinds, and strategic expansion in diagnostics with the acquisition of Masimo.

Danaher Corporation delivered modest revenue growth of 3% in 2025 driven by Biotechnology and Diagnostics segments while Life Sciences showed softness. Operating income declined slightly on increased tariff-related costs and impairments. The company’s return on equity softened to around 6.9%, with strong free cash flow generation supporting dividend increases and a sizable share repurchase program. Danaher’s recent $9.9 billion Masimo buyout expands its diagnostics footprint amid challenging trade tariffs that pressure margins. Continued innovation, geographic diversification, and operational efficiencies via the Danaher Business System underpin longer-term growth prospects amid evolving regulatory and trade environments.

Company Overview and Business Model

Danaher Corporation operates globally across three core segments: Biotechnology, Life Sciences, and Diagnostics, offering scientific instruments, consumables, software, and services that support biotherapeutics development, life sciences research, and clinical diagnostics [S1][S4]. Approximately 59% of revenues come from international markets including both developed geographies—primarily North America and Europe—and high-growth regions where China remains a challenging but significant contributor [S14][S18]. Danaher leverages a proprietary Danaher Business System to drive continuous operational improvements and productivity enhancements.

Historical Financial Performance

Danaher exhibited steady revenue growth over recent years with a reported increase of roughly 3% in overall revenues for FY2025 compared to FY2024 [F1], mainly fueled by strength in Biotechnology (+7.5% core sales) and Diagnostics (+2%) while Life Sciences experienced slight declines [S14][S19]. Currency translation added approximately 1% uplift to reported sales owing largely to favorable exchange rates against the U.S. dollar [S18]. Price increases contributed about 0.5% year-over-year growth mitigating inflationary pressures from tariffs [S14].

Operating income declined by approximately 3.6% to $4.69 billion in FY2025 due to a mix of tariff-driven cost increases approaching several hundred million dollars annually [S22], impairment charges totaling $548 million pre-tax year-to-date [S13], unfavorable product mix shifts, partially offset by incremental productivity gains [S16]. Net income declined by around 7.3% year-over-year to $3.61 billion reflecting these margin pressures along with increased operating expenses [F1].

Historical performance (annual)

| FY | Net ($bn) | CFO ($bn) | OpInc ($bn) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 3.6 | 6.4 | 4.7 | 1156 | -7.3% |

| 2024 | 3.9 | 6.7 | 4.9 | 1392 | -18.2% |

| 2023 | 4.8 | 7.2 | 1.3 | 1383 | -33.9% |

| 2022 | 7.2 | 8.5 | 8.7 | 1152 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($bn) | FCF ($bn) |

|---|---|---|---|

| 2025 | 878 | 3.1 | 5.3 |

| 2024 | 768 | 6.0 | 5.3 |

| 2023 | 821 | 5.8 | |

| 2022 | 818 | 7.4 |

Source: SEC companyfacts cache [F1].

*Note: Certain metrics for FY2024 revenue are not explicitly available in the provided tags; operating income and net income reflect reported values from [F1].

Segment Performance Highlights

Biotechnology

This segment demonstrated robust growth with core sales up approximately mid-to-high single digits, driven mainly by consumables for bioprocessing solutions supporting monoclonal antibodies, vaccines, gene therapy manufacturing [S19][S20]. Equipment demand softened mildly amid cautious investment spending trends but was offset by higher-margin consumables sales contributing to stable operating margins around mid-20%s [S20].

Diagnostics

Core sales were up mid-single digits aided significantly by new offerings in respiratory testing and pathology diagnostics outside China where regulatory reforms have depressed volumes [S15][S14]. The recent acquisition of Masimo for $9.9 billion expands Danaher’s footprint in advanced monitoring technologies strengthening competitive positioning [N1][N3]. Operating margins improved slightly through scale efficiencies despite tariff interruptions.

Life Sciences

This segment faced headwinds from reduced funding at emerging biotech customers and academic research clients primarily in North America leading to core sales decline just below low single digits [S11][S19]. Equipment sales softened while filtration consumables showed pockets of growth across aerospace and microelectronics end-markets.

Capital Allocation & Returns

Danaher continues generating strong operating cash flow exceeding $6 billion annually though showing an approximate decline of ~4% from FY24 levels driven by lower net earnings [F1][S7]. Capital expenditures moderated significantly (down ~17%), reflecting disciplined investment strategies focusing on capacity optimization rather than expansion [F1][S19]. Free cash flow remains healthy at about $5.26 billion (operating cash flow minus capex) supporting consistent dividend growth—with dividends rising over prior years—and substantial share repurchase programs which totaled approximately $3 billion in FY2025 down from nearly double that level in FY2024 after an aggressive buyback spree earlier [F1][S23].

Return on equity has moderated to roughly 6.9%, tempered by lower net income combined with a steady increase in shareholders’ equity base following acquisitions like Masimo and retained earnings accumulation [F1].

Recent Developments: Masimo Acquisition & Market Environment

In February 2026, Danaher announced its approval of a $9.9 billion all-cash offer for Masimo Corporation aimed at extending its capabilities in patient monitoring technology within Diagnostics—a strategic move expected to diversify revenue streams further into diagnostic devices with high barriers to entry given regulatory complexities [N1][N3][S3]. This deal follows Danaher’s approach of acquiring high-growth platforms complementary to its existing portfolio while integrating them under its business system for margin improvements.

Trade environment challenges persist: The US government’s evolving tariff policy has introduced incremental costs estimated at several hundred million dollars annually impacting production inputs, prompting surcharges on customers or price hikes that could dampen demand elasticity moderately [S22]. A pending Supreme Court case regarding the statutory authority for some tariffs creates uncertainty; however, Danaher has so far largely mitigated margin erosion through supply chain redesigns and cost-saving initiatives.

Industry & Competitive Context (Analysis)

Danaher's performance is set against broader life sciences industry dynamics including accelerated adoption of cell/gene therapies driving biotechnology consumables demand but coupled with uncertain academic funding impacting foundational research equipment sales globally.

Additionally, regulatory scrutiny intensifies especially in China where government healthcare procurement reforms impact pricing power particularly for diagnostics consumables.

Precision instrumentation makers face rising material costs due to tariffs on electronics components compounded by geopolitical volatility affecting supply chains requiring agile sourcing strategies—a competitive advantage tied closely to operational excellence frameworks like Danaher's Business System.

What To Watch Going Forward (Analysis)

Key milestones include successful integration outcomes from the Masimo acquisition within FY2026 impacting segment reporting next year; monitoring tariff developments following Supreme Court rulings; execution on R&D product pipeline aligning innovations towards AI-enabled diagnostic tools; sustaining organic core sales momentum especially within high-growth Asia-Pacific markets outside China; managing foreign currency fluctuations as reported international revenues comprise majority of total sales; and maintaining robust free cash flow to balance reinvestment needs against shareholder returns.

Risks Highlighted By Management

Potential risks center on sustained volatility from fluctuating trade policies impacting supply cost structures unpredictably; shifting regulatory landscapes especially around intellectual property protections in China; military conflicts influencing regional operations or customer demand; continuing macroeconomic pressures including inflation affecting end-market healthcare budgets; execution risks associated with large acquisitions including cultural integration or unforeseen liabilities; foreign currency translation impacting consolidated results; plus legal contingencies inherent in complex multinational operations [S1][S13][S29].

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data as of early-2026 without any endorsement or investment recommendation.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments