Dole plc's Strategic Portfolio Simplification and Margin Pressure in 2025

Dole's 2025 financials reflect a strategic exit from fresh vegetables and port operations, influencing profitability amid ongoing industry headwinds.

Dole plc reported weaker profitability in 2025, with operating income falling over 20% year-over-year and net income down nearly 60%. The company completed the sale of its Fresh Vegetables division for $140 million and is set to divest Ecuadorian port assets for approximately $75 million. Despite these divestitures reducing some operational complexity, margin pressure persists due to external factors like trade policies and weather disruptions. Capital allocation remains disciplined with stable dividends and controlled capex, supporting liquidity amid these transitions.

Company Overview and Business Segments

Dole plc operates through three main reportable segments: Fresh Fruit; Diversified Fresh Produce – EMEA; and Diversified Fresh Produce – Americas & ROW [S4]. The Fresh Fruit segment primarily sells bananas, pineapples, and plantains sourced mainly from Dole-owned or leased farms in Latin America, distributed across North America, Europe, Latin America, and Asia. This segment also includes a commercial cargo business utilizing company-owned vessels for transporting produce between key regions.

The Diversified Fresh Produce segments cover a wide range of fruits and vegetables sold through retail, wholesale, e-commerce, and food service channels across Europe, South Africa, Brazil (EMEA segment), and the Americas including North and South American countries (Americas & ROW segment) [S4].

Historical Financial Performance

Based on SEC filings data [F1], Dole’s operating income grew from $114 million in FY2022 to about $280 million in FY2024 before declining by 20.5% to $223 million in FY2025. Net income similarly peaked near $125 million in FY2023 and FY2024 but dropped sharply by 59.1% to approximately $51 million in FY2025.

Operating cash flow experienced significant variability with a strong rebound leading to estimated free cash flow of about $117 million in FY2025 after capital expenditures rose nearly 50% to over $121 million [F1]. Dividend payments remained consistent near $32 million annually despite earnings fluctuations.

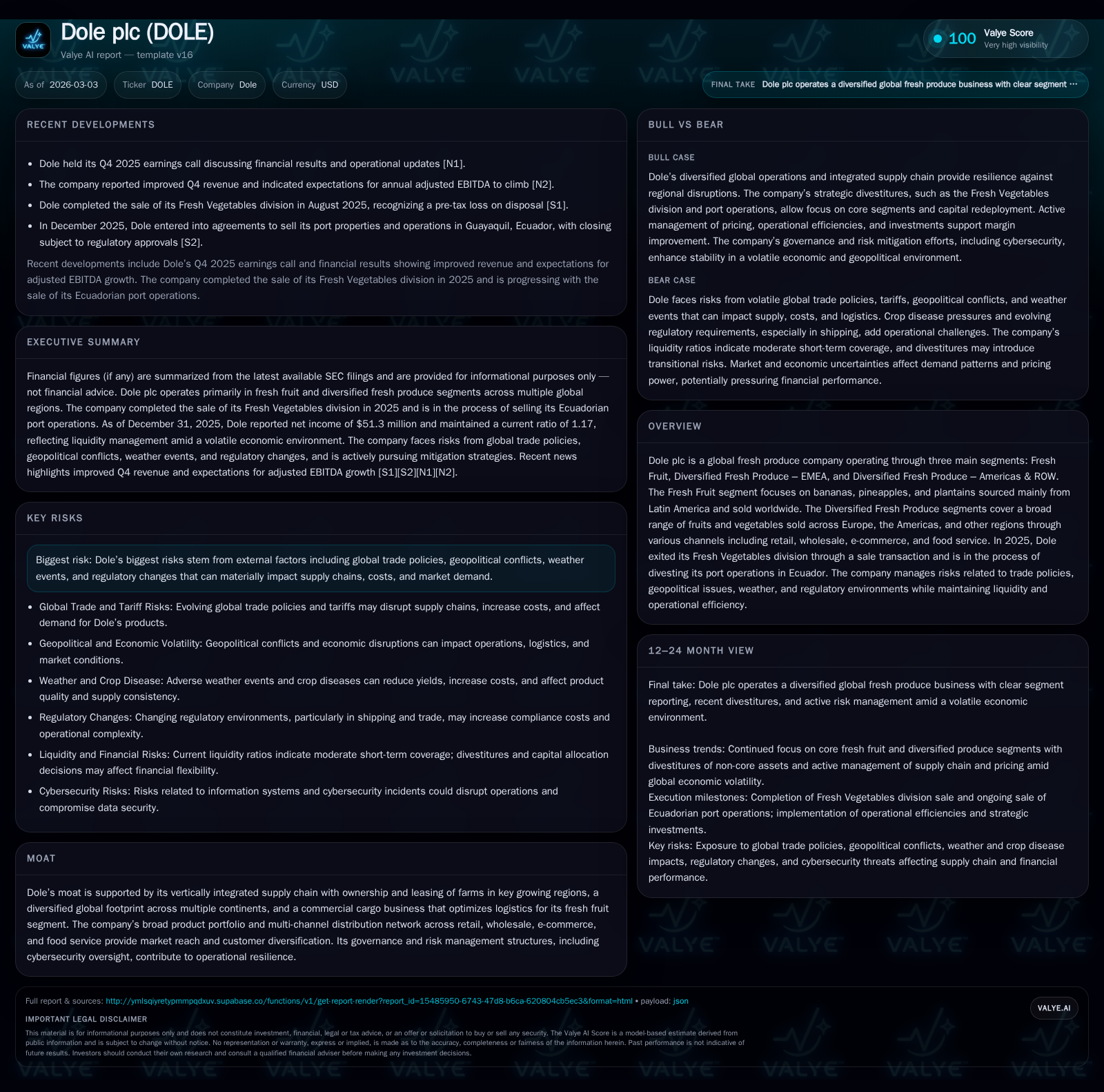

Historical performance (annual)

| FY | Net ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 51 | 223 | 121 | -59.1% |

| 2024 | 126 | 281 | 82 | +1.2% |

| 2023 | 124 | 272 | 78 | +43.4% |

| 2022 | 86 | 114 | 98 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | ROE% |

|---|---|---|

| 2025 | 32 | 3.8 |

| 2024 | 31 | 9.7 |

| 2023 | 31 | 9.9 |

| 2022 | 31 | 7.4 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow data is unavailable for recent years except FY2022; dividend figures approximate annual totals [F1].

Strategic Divestitures Impacting Growth

In August 2025, Dole completed the sale of its Fresh Vegetables division for approximately $140 million (including cash and seller note components), recognizing a pre-tax loss of about $14.7 million [S1][S4]. Proceeds were mainly used to reduce debt under the Corporate Revolving Credit Facility.

Additionally, agreements were signed at year-end for selling port properties and related operations in Guayaquil, Ecuador, expected to close during 2026 with net proceeds estimated near $75 million [S2]. Post-sale, Dole will continue using these port facilities under arm's-length service agreements.

These disposals reflect a deliberate focus on core fresh fruit businesses while simplifying the overall portfolio.

Future Growth Prospects and Risks

Dole aims to leverage scale efficiencies within its Fresh Fruit segment alongside diversified produce offerings across global markets [S4]. However, growth faces headwinds including:

- Trade policy uncertainties impacting tariffs and logistics costs [S7]

- Geopolitical conflicts affecting supply chains and currency volatility [S7]

- Weather-related crop risks exemplified by recent tropical storms [S7]

- Regulatory changes increasing compliance costs particularly in shipping [S7]

- Crop disease pressures necessitating ongoing agricultural management efforts

Management is actively responding through pricing strategies, operational efficiencies, targeted investments, and supply chain agility to mitigate these challenges [S7].

Capital Allocation and Returns

Dole demonstrates disciplined capital management balancing reinvestment with shareholder returns amidst restructuring phases. Dividend payments have remained stable near the low-$30 million range annually despite earnings volatility [F1][S8][S20].

Capital expenditures increased significantly by approximately 47% from FY2024 to FY2025 as investments support focused growth areas post-divestitures [F1]. Equity has grown steadily but returns on equity have moderated to about 3.8% in FY2025 reflecting transitional impacts [F1].

Free cash flow generation remains robust due to asset sale proceeds; however, operational risks warrant cautious outlooks.

Operational Resilience Through Governance Frameworks

Cybersecurity risk management is integral at Dole with dedicated governance structures overseeing identification and mitigation efforts across global operations [S1][S23]. The Board of Directors maintains oversight through regular reporting from executive committees ensuring comprehensive risk controls vital for business continuity.

Summary Analysis

Fiscal year 2025 highlights Dole’s transition towards a streamlined portfolio focusing on high-volume fresh fruit categories while exiting non-core vegetable production and port operations. Profitability declined amid margin pressures but was partially offset by cash inflows from disposals aiding debt reduction.

Ongoing risks from trade policies, geopolitical tensions, weather events, and regulatory shifts remain challenges for future performance. Nevertheless, Dole’s integrated supply chain model spanning multiple continents provides competitive advantages.

Investors should monitor tariff developments and geopolitical dynamics impacting critical sourcing regions primarily in Latin America.

This analysis is based exclusively on publicly available SEC filings up to March 3rd, 2026 ([F1],[S1],[S2],[S4],[S7],[S8],[S20]) and relevant news transcripts ([N1],[N2]). No forward-looking statements beyond documented disclosures are included.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments