Viant Technology's Q1 2026: Platform Enhancements and Market Shifts in Programmatic Advertising

Viant’s latest quarter underscores platform evolution amid intensifying industry privacy shifts and competitive dynamics.

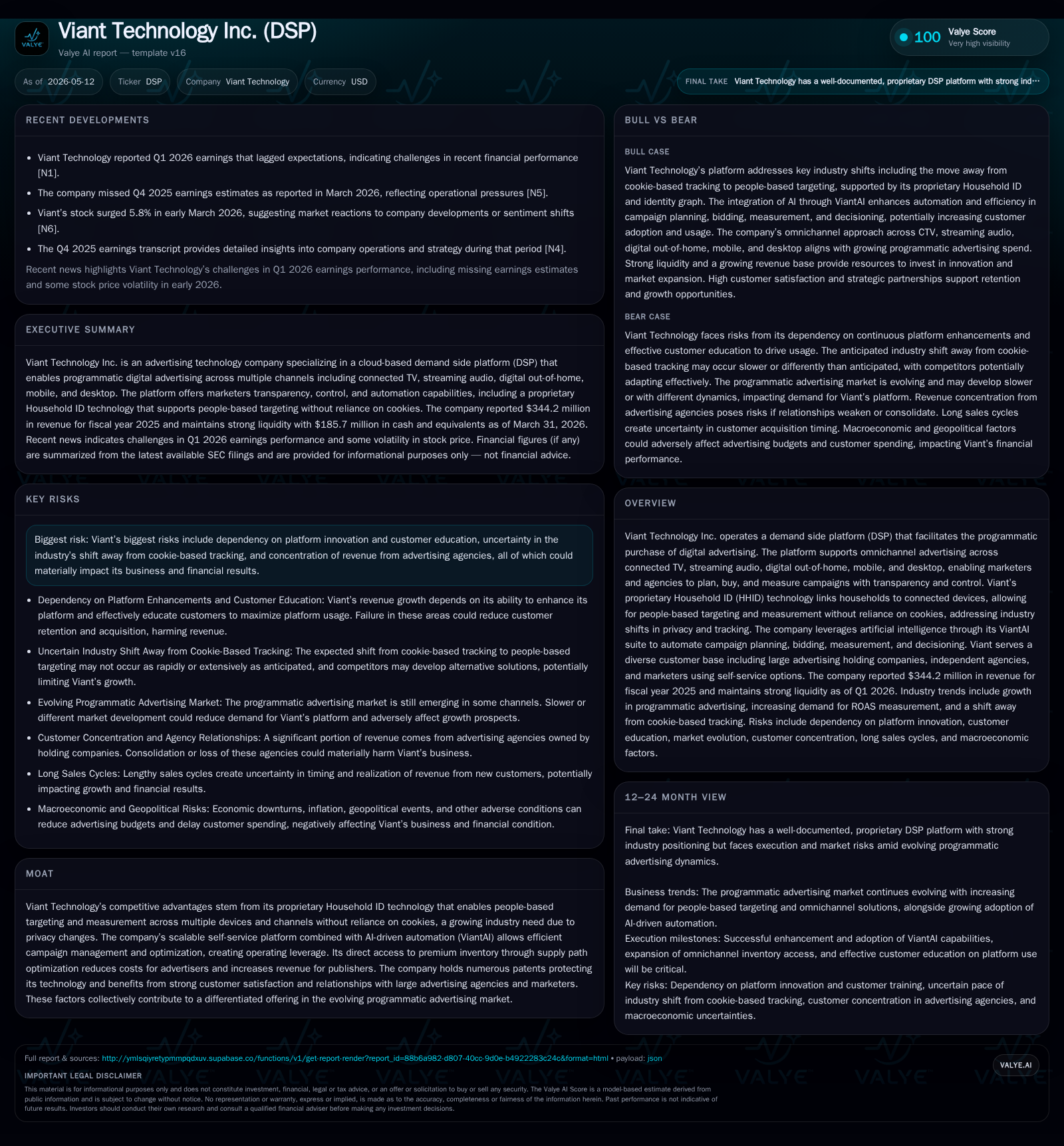

In Q1 2026, Viant Technology navigated a complex programmatic advertising landscape marked by slower-than-expected revenue growth and evolving customer adoption patterns. The company’s proprietary Household ID and AI-powered ViantAI suite remain central to its differentiation in a cookie-less ecosystem. Although Viant lagged earnings estimates, ongoing investments in omnichannel inventory integration, autonomous campaign management, and strategic acquisitions point toward a deliberate push for scaling market share. Risks persist from long sales cycles, competitive pressures from dominant tech platforms, and regulatory uncertainties on data privacy.

Latest Quarterly Operating Update: What Changed and Why It Matters

Viant Technology’s Q1 2026 (ending March 31) results, filed on May 11 [S2], revealed revenue growth that undershot market projections per contemporaneous reporting [N1]. While exact top-line figures for the quarter are not isolated in the filing, commentary highlights ongoing operational challenges tied to client ramp-up timing and competitive pressures. Management emphasized continued enhancements in their proprietary demand-side platform (DSP), including incremental functionality within the ViantAI automation suite aimed at simplifying campaign execution for customers.

The quarter was also notable for the April announcement of the TVision Insights acquisition [S24], which is expected to broaden Viant’s footprint into audience measurement beyond pure ad-buying technology. This move aligns with strategic intentions disclosed in prior disclosures to expand product offerings through acquisitions [S5]. However, the TVision business carries litigation risks due to ongoing patent infringement suits involving Nielsen [S23], which investors should monitor closely given scheduled jury trials in mid-2026.

Operationally, client adoption cycles remain elongated due to the complexity inherent in programmatic marketing platforms. Viant reiterated its commitment to investing in customer training and certification programs as key enablers of platform utilization growth [S17]. Despite these headwinds, Viant continues to leverage its AI-driven autonomous management capabilities coupled with people-based targeting technology as primary differentiators.

Business Model and Product Offering: How Viant Delivers Value

Viant operates a cloud-based DSP offering programmatic purchasing capabilities across diverse digital advertising channels including connected TV (CTV), streaming audio, digital out-of-home (DOOH), mobile devices, and desktop environments [S1]. Its core business model earns revenue by enabling marketers and agencies to plan, buy, optimize and measure advertising campaigns via an integrated self-service platform or managed service options.

A foundational element of Viant’s value proposition lies in its patented Household ID (HHID) system that circumvents traditional third-party cookie dependencies by linking over 125 million households to approximately one billion devices [S1]. This people-based identity resolution facilitates more precise targeting without compromising consumer privacy amid changing industry standards.

The company’s automation engine—ViantAI—augments this identity graph by orchestrating machine learning algorithms that autonomously handle media planning decisions including real-time bidding (RTB), inventory sourcing through private marketplaces and programmatic guaranteed deals. By automating thousands of iterative campaign adjustments based on performance signals, ViantAI aims to increase advertisers’ return-on-ad-spend (ROAS) while lowering manual operational burdens [S1,S22].

Customers range widely from large holding companies managing multiple agencies to independent marketers utilizing self-service tools. Contract models are flexible with pricing based on either spend percentages or fixed CPM fees depending on client preference [S17].

Industry Positioning and Competitive Advantages

In the fragmented yet fiercely competitive DSP landscape dominated by entrenched players such as The Trade Desk alongside divisions of tech giants Google and Amazon [S4,S21], Viant stakes its competitive position on technological independence, transparent operations, and integrated data capabilities.

Its proprietary HHID technology delivers a significant moat given industry secular trends away from cookie-reliant targeting methods fueled by regulatory privacy constraints [S1,S15]. Unlike many competitors dependent on external data providers or legacy cookie frameworks, Viant offers end-to-end integration of identity resolution attached directly within its DSP architecture [S22].

Moreover, ViantAI’s autonomous campaign management suite constitutes a structural advantage by enabling scalable growth with minimal proportional staffing increases—a critical factor in an industry where labor-intensive manual optimization is costly [S22]. The company also emphasizes direct access relationships with premium supply-side platforms fostering supply path optimization that reduces costs for buyers while increasing yield for publishers.

This combination of patented technology (backed by over 65 issued patents), AI-driven workflow automation, broad multichannel inventory access (CTV to DOOH), plus high-touch customer support provides an increasingly rare value proposition as many incumbents either lack autonomy or suffer from fragmented service stacks [S4,S15,S22].

Growth Drivers: AI Automation, Data Identity, and Omnichannel Reach

Viant’s trajectory rides on multiple interlocking growth vectors: first is accelerating displacement of cookie-based programmatic targeting by identity solutions like HHID that overcome tightening privacy regulations; second is expanding demand for advanced autonomous bidding technologies embodied by the ViantAI suite; third is the rise of omnichannel advertising budgets encompassing streaming video/audio alongside legacy digital formats.

Industry-wide shifts toward connected TV advertising provide fertile ground for increased DSP adoption given explosive CTV spend growth compared to traditional desktop display ads. Additionally, advertisers seek platforms that unify fragmented inventory across environments without sacrificing precision targeting or measurement granularity.

Viant’s recent extension into digital out-of-home through new supply integrations bolsters this omnichannel inventory strategy further diversifying addressable spend pools. Concurrent investment in seamless first-party data onboarding meets marketer demand for control over data assets amidst cookie depreciation challenges.

AI-powered tools like ViantAI automate laborious optimization routines allowing clients—especially those leaning on self-service—to achieve improved efficiency at scale. This feeds into operating leverage as incremental revenue gains do not necessitate parallel cost increases in human oversight [S22]. Concurrently expanding sales efforts focus both on new client acquisition in verticals like automotive/retail/healthcare via bespoke HUD-enabled targeting plus deeper penetration within existing agency portfolios via certification/training programs drives pipeline maturation efforts [S17,S19].

Risks and Watchpoints: Platform Adoption, Industry Shifts, and Customer Concentration

Fundamental risks emerge primarily from still-lengthy sales cycles characteristic of complex DSP implementations which impede predictable near-term revenue visibility [S2,S18]. Customer education remains pivotal; failure to fully train users or convince large-scale advertisers to migrate budgets onto new platforms could stall adoption momentum.

The overall programmatic market development pace remains uncertain—the anticipated rapid shift away from cookie-based tracking might not fully materialize or may be competitively countered by incumbents offering alternative tracking solutions undermining HHID advantages [S1,S20]. Revenue concentration risk persists as several major advertising agency holding companies represent significant portions of total billings leaving exposure if client budgets contract or strategic priorities shift abruptly.

Intensifying competition from deep-pocketed internet giants could pressure pricing structures leading to margin compression; these competitors may bundle ad offerings or leverage proprietary walled gardens limiting the total addressable market accessible through open DSPs like Viant’s [S15].

Regulatory scrutiny relating to data privacy laws globally introduces ongoing compliance costs along with potential liability risks from missteps—compounded by complex multi-jurisdictional governance over personal information usage in advertising contexts [S18,S26,S29]. Finally, patent litigation linked to the acquired TVision business presents contingent legal risks warranting careful monitoring due mid-2026 trial dates [S23].

Outlook: Key Milestones, Guidance, and Execution Markers for Investors

Looking ahead through 2026’s second quarter onward [S3], critical success factors center around accelerating customer conversions currently impeded by long sales cycles; tracking progressive traction of autonomous campaign execution modes within installed base; integrating TVision's analytics offerings effectively without disruption; extending partnerships across additional omnichannel supply sources; refining supply path optimization tools for better cost structures; and signaling tangible margin improvements driven by operating leverage from automation enhancements.

Continued salesforce expansion paired with branding initiatives promoting ViantAI distinctiveness versus entrenched players is expected. Investors should watch announcements around expanded data partnerships enabling richer HHID linkages or new inventory types added under direct access agreements. Regulatory developments influencing cookie deprecation timelines or data usage restrictions will be pivotal external events shaping demand forecasts.

Financial Profile: Liquidity, Capital Structure, and Profitability Snapshot

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $186mm | |

| 2026-03-31 | ||

| Current assets | $338mm | |

| 2026-03-31 | ||

| Current liabilities | $118mm | |

| 2026-03-31 | ||

| Current ratio | 2.87x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

Viant entered 2026 with a strong liquidity position supporting unleveraged balance sheet strength as a base for investment in growth initiatives. At March 31st quarter-end, cash & equivalents stood at $185.7 million with zero reported debt liabilities (net debt negative at -$185.7 million) yielding a current ratio of 2.87 evidencing solid short-term solvency [F1]. Recent net income measured $8.35 million at fiscal year-end December 31st provides profitability evidence amidst reinvestment phases while operating income rose to $12.08 million during FY25 reflecting underlying margin improvement trends noted prior quarters [F1].

| Metric | Value |

|---|---|

| Cash & Equivalents | $185.7 million |

| Total Debt | $0 |

| Current Ratio | 2.87 |

| Latest Reported Net Income | $8.35 million |

This financial flexibility affords Viant leeway despite macroeconomic uncertainty affecting ad spend overall.

This analysis synthesizes publicly available SEC disclosures as of May 2026 alongside contemporaneous news intelligence reflecting recent quarterly results focusing on operational dynamics within programmatic advertising markets subject to technological disruption and regulatory evolution. It does not constitute investment advice or specific stock recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments