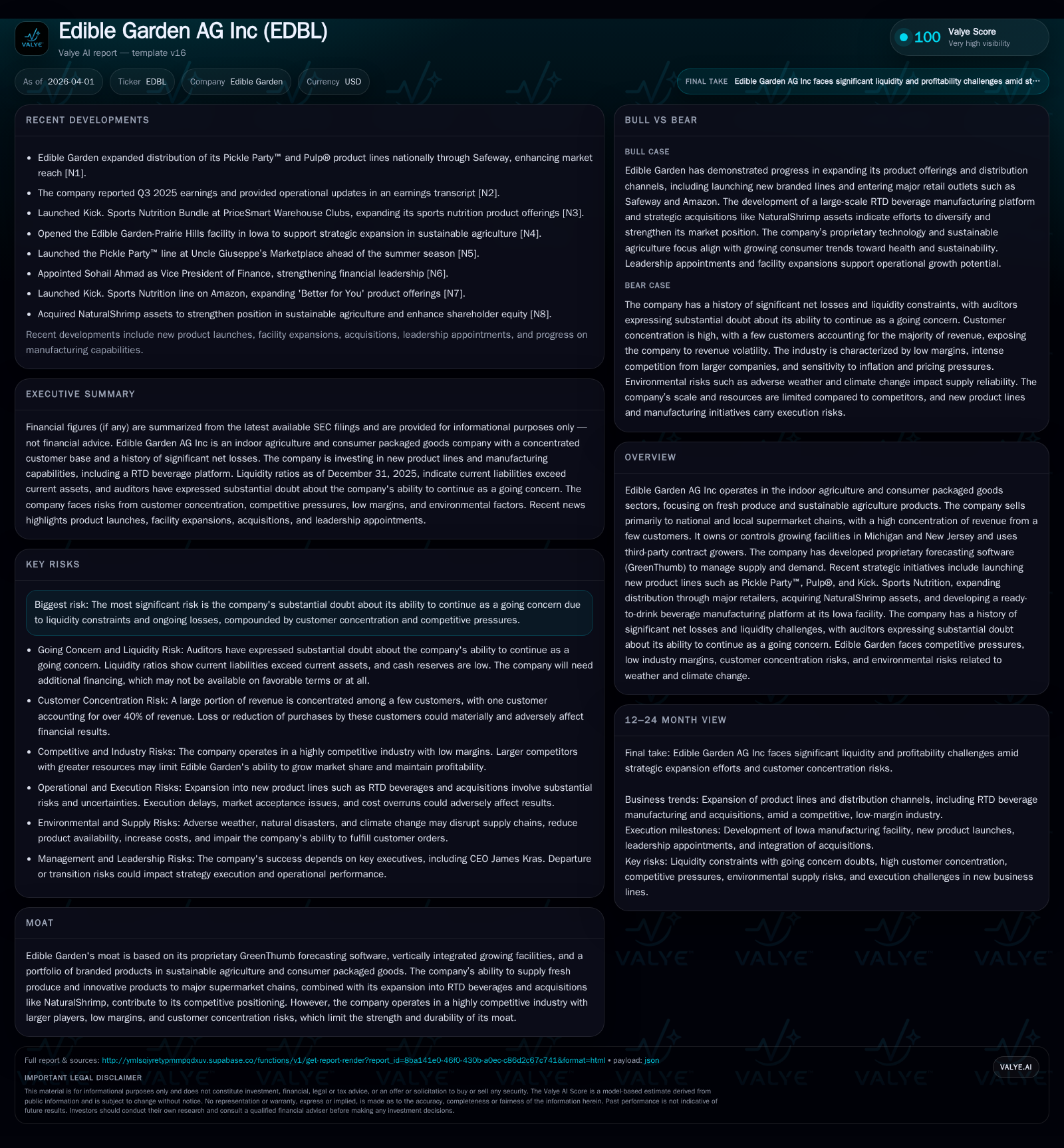

Edible Garden AG: Parsing Financial Struggles Against Expansion Ambitions

Edible Garden AG pursues innovative growth through vertical integration and product diversification while confronting severe liquidity challenges and customer concentration risks.

Edible Garden AG has embarked on ambitious expansion initiatives, including proprietary GreenThumb forecasting software, new branded product lines, and the development of a ready-to-drink beverage platform. However, these strategic efforts contrast sharply with a deteriorating financial profile marked by declining revenues, escalating operating losses, and substantial doubts about its ability to continue as a going concern. Customer concentration further exacerbates revenue volatility. Capital allocation prioritizes growth investments amid negative operating cash flow and weak liquidity, underscoring the delicate balance between innovation and financial sustainability.

Revenue and Operating Trends: Declining Top Line and Deepening Losses

Edible Garden AG's financial trajectory reveals an unsettling pattern of shrinking revenue alongside intensifying losses that frame its current challenges. The company's annual reported revenue peaked in FY2023 at approximately $14.05 million but subsequently fell to $13.86 million in FY2024 and further declined to around $12.81 million in FY2025—a cumulative contraction representing a decline of approximately 7.6% year-over-year last fiscal period alone [F1]. This downturn comes despite ongoing product launches and market expansion efforts.

Operating income tells an even starker story: Edible Garden’s operating loss ballooned from roughly -$9.27 million in FY2024 to an estimated -$15.8 million by FY2025—reflecting a sharp deterioration of over 70% in operating performance within just one year [F1]. Similarly, net income deteriorated from -$11.05 million in FY2024 to a deeper loss of approximately -$17.33 million in FY2025, worsening by more than 56% YoY [F1].

Operating cash flow follows suit with significant negative figures continuing unabated: CFO declined from -$8.5 million in FY2024 to -$11.8 million in FY2025—a near 39% acceleration of cash burn [F1]. Coupled with relatively modest capital expenditure increases (discussed later), this signals limited operational leverage or margin improvement despite expanding sales infrastructure.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 13 | -17 | -12 | -16 | -7.6% | -56.8% |

| 2024 | 14 | -11 | -9 | -9 | -1.4% | -8.5% |

| 2023 | 14 | -10 | -9 | -10 | +21.6% | +18.2% |

| 2022 | 12 | -12 | -9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | -12 | -138.7 |

| 2024 | -9 | -269.9 |

| 2023 | -10 | 3537.5 |

| 2022 | -11 | 571.2 |

Source: SEC companyfacts cache [F1].

The disconnect between revenue stabilization attempts via new product introductions and worsening profitability underscores critical operational challenges. These losses are partly driven by upfront sales and marketing investments required to expand the customer base and infrastructure build-out costs for emerging lines such as ready-to-drink (RTD) beverages.

Customer Concentration: A Double-Edged Sword

Customer concentration poses material volatility risks to Edible Garden's revenue stability and reflects a structural vulnerability in its business model [S4][S8]. In FY2025, approximately 88% of total revenues stemmed from just five customers, with one dominant client contributing roughly 42–43% alone [S4]. Such concentration magnifies the impact of any single customer's decision to reduce orders or terminate relationships without long-term contracts firmly tying demand.

While some Supply Agreements exist with major retailers—including Meijer through December 31, 2026—these agreements permit termination with only sixty days' notice without cause [S4], underscoring the fragility of these customer relationships.

Reliance on a handful of supermarket chains distributing fresh produce and specialty consumer packaged goods exposes Edible Garden to fluctuations driven by retail consolidation trends or changes in strategic priorities at these retailers [S6][S8]. The lack of durable contracts may also compel the company to divert resources reactively to meet short-notice volume demands from key customers.

This dynamic presents significant downside if one or more major accounts reduce volumes or encounter financial difficulties—a scenario that could materially impair revenue generation and profitability prospects.

Proprietary Advances and Product Expansion: GreenThumb Software and New Verticals

Edible Garden leverages vertical integration combined with proprietary technology as a competitive differentiator within a fiercely contested indoor agriculture and consumer packaged goods landscape [S6][S8]. Its GreenThumb forecasting software optimizes supply-demand synchronization across controlled growing facilities located strategically in Michigan and New Jersey while coordinating third-party contract growers downstream.

Vertical integration encompasses both growing operations and processing capabilities—allowing improved traceability, inventory management, and quality control amid perishable product constraints typical of fresh produce segments.

Complementing this foundation are branded product expansions including Pickle Party™, fresh/fermented pickles aimed at broadening condiment category penetration; Pulp®, targeting plant-based sauces; Kick.Sports Nutrition offering cleaner-label nutraceutical formulations; alongside an acquisition of NaturalShrimp assets adding protein diversification [S6][S8].

Crucially, Edible Garden is developing an aseptic ready-to-drink beverage manufacturing platform at its Iowa facility intended to cover functional beverages spanning protein-, plant-, dairy-, and nutraceutical-based drinks [S6]. Aseptic processing enables shelf-stable RTD products without preservatives—a value proposition aligned with health-conscious consumer trends but still early-stage.

These innovation efforts aim to build operational moats amid commoditized fresh produce markets characterized by low margins and intense price competition from larger incumbents backed by scale advantages.

Liquidity Challenges and Going Concern Doubts

Despite innovative ambitions, Edible Garden’s financial footing is precarious—highlighted emphatically by auditor-issued substantial doubt about its ability to continue as a going concern [S1][F1]. This reflects key liquidity constraints aggravated by heavy cash burn.

Cash on hand was reported at only $110,000 at end-2022 with current liabilities exceeding current assets (current ratio ~0.82) as of December 31, 2025 ([F1]). Operating activities consumed approximately $11.8 million during FY2025 alone—worsened from $8.5 million the prior year—and capital spending contributed further net negative free cash flow estimated near $12.4 million when adjusting CFO for capex [F1].

Management disclosed current capital resources would only finance operations into roughly Q2 2026 absent additional financing sources—an uncertain prospect given market conditions—and stressed continual losses tied both to growth investments as well as cost structure inefficiencies typical among smaller enterprises stretching capacity across diversified channels [S11][S13].

Debt obligations secured against material assets constrain flexibility while raising default risk if operational improvements do not materialize rapidly enough [S11].

Together, these factors paint a high-risk picture where failure to secure timely funding or reverse loss trends could jeopardize business continuity—potentially wiping out shareholder value entirely.

Capital Allocation: Cash Flows, Capex, and the Quest for Stability

Capital deployment reflects cautious attempts to balance investment in growth infrastructure against preserving liquidity amid adverse profitability metrics.

Capex rose markedly by approximately 110% from around $303K in FY2024 to $638K during FY2025 despite constrained cash flow ([F1]). This increase underscores targeted investment toward manufacturing capability—particularly around RTD beverage facilities—and packhouse expansions required for scaling vertically integrated operations [S14].

No dividends or share repurchase programs exist given financial constraints; instead equity levels improved substantially from deeply negative bases (-$288K FY23; -$2.18M FY22) up to $12.5 million booked at end-FY25 following recent financings likely accompanied by dilution risks highlighted in filings ([F1]).

Profitability metrics remain challenging—the rough estimate for return on equity extrapolated from last reported net loss versus equity stands near negative 139%, signaling acute inability thus far to generate returns commensurate with invested capital ([F1]).

Overall cash flow trends reinforce that substantial external capital infusions will be required until sustainable positive margins are achieved—or risk exit scenarios triggered by liquidity failure become imminent.

Risks from Competition, Regulatory Environment, and Supply Chain Pressures

Edible Garden operates within an industry sector marked by persistent challenges related primarily to sector-specific factors compounded by macroeconomic variables .

Intense competition arises from well-established players with greater economies of scale and diversified portfolios capable of exerting pricing pressure—a challenge for smaller firms lacking operating leverage ([S5],[S14]). Sustained inflation in key raw materials like fertilizers or aluminum directly compresses gross margins unless cost pass-throughs are feasible—a condition complicated by retailer bargaining power ([S5],[S14]).

Regulatory compliance adds complexity through FDA/USDA oversight encompassing food safety protocols spanning production processes through labeling/distribution which can elevate expenses materially ([S28]). Product contamination risks bring potential recalls causing direct costs plus reputational damage ([S7],[S22]). Intellectual property disputes present additional legal exposure affecting results ([S9],[S29]).

The operational model’s reliance on short-duration purchase orders rather than long-term contracts amplifies demand uncertainty raising inventory management challenges across perishable goods ([S6]). Labor shortages impacting skilled plant operators essential for RTD beverage production add execution risk affecting timelines ([S20]).

Outlook: What to Monitor in Edible Garden’s Forward Trajectory

Absent explicit numerical forecasts beyond existing SEC disclosures, investors should closely watch several pivotal developments determining whether Edible Garden can reconcile innovation ambitions with financial viability:

- Commercialization progress of the RTD beverage manufacturing platform at Iowa—including operational ramp-up milestones—is crucial given potential margin uplift relative to commoditized fresh produce lines ([S6]).

- Customer diversification beyond highly concentrated top five clients will be key indicators mitigating concentration risk—monitor shifts in revenue mix where available ([S4],[S6]).

- Quarterly cash burn rates approaching or exceeding projections could foreshadow liquidity crises absent refinancing or capital raises ([F1],[S13]).

- Market acceptance trajectories for products such as Pickle Party™, Pulp®, Kick.Sports Nutrition provide early signs on brand momentum outside core categories ([S6]).

- Material margin improvements or pricing power shifts would bolster outlook amid historically low gross margins across sector peers ([S14],[S6]).

- Legal/regulatory developments including food safety compliance audits or intellectual property litigation must be monitored due to potential cost burdens ([S7],[S9],[S29]).

In sum, Edible Garden’s balance sheet fragility combined with execution complexity amid competitive pressures makes its path forward contingent upon timely achievement of strategic milestones while managing ongoing financial headwinds.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments