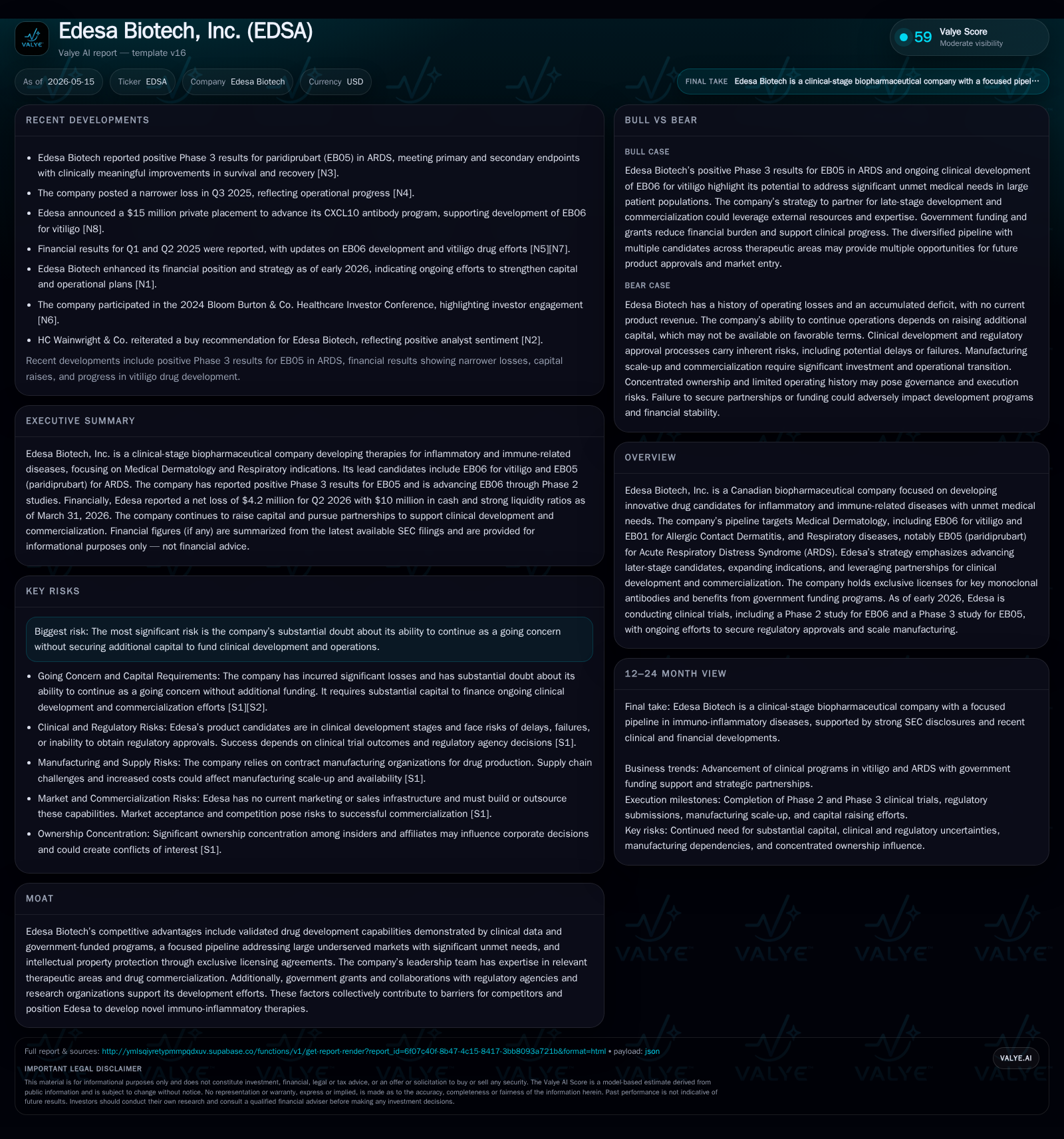

Edesa Biotech’s Strategic Focus on Immuno-Inflammatory Pipeline and Capital Outlook

Edesa Biotech advances pivotal immuno-inflammatory drug candidates while balancing financial sustainability in a capital-intensive development phase.

In its latest quarterly filing, Edesa Biotech disclosed continued clinical progress in its immuno-inflammatory pipeline, notably a Phase 2 initiation for EB06 targeting vitiligo and completion of a positive Phase 3 study for EB05 in ARDS. The company leverages exclusive licensing and government grants to fund development but remains challenged by funding needs beyond current liquidity. Its business model focuses on advancing late-stage drug candidates for large-unmet medical needs in Medical Dermatology and Respiratory diseases, underpinned by outsourcing manufacturing to control costs. Key risks include capital adequacy constraints despite a decent current ratio and inherent regulatory uncertainties. Upcoming milestones include enrollment commencement for EB06 and further regulatory interactions, critical to maintaining development momentum.

Latest Operating Update: Trials and Development Milestones

Edesa Biotech’s recent quarterly disclosure dated May 14, 2026, reveals significant clinical advancements that anchor the company's near-term operational narrative. The company is poised to initiate enrollment for EB06’s Phase 2 proof-of-concept trial targeting moderate-to-severe nonsegmental vitiligo by mid-2026, pending U.S. FDA approval, following Health Canada’s earlier clearance [S2][S3][S1]. This milestone represents a critical validation step for the anti-CXCL10 monoclonal antibody candidate aimed at an autoimmune skin disorder with limited approved therapies.

Simultaneously, Edesa reported results from a truncated Phase 3 study of paridiprubart (EB05) in hospitalized patients with acute respiratory distress syndrome (ARDS), demonstrating statistically significant reductions in adjusted 28-day mortality across diverse patient subgroups including those with comorbidities like sepsis and acute kidney injury [S1][S9]. The data underpin the unique positioning of this host-directed therapeutic (HDT), designed to modulate immune responses during severe respiratory failure conditions originating from infections or chemical exposures.

The ongoing US government-funded platform study further complements EB05’s clinical profile and is concurrently supported by Canadian government grants aimed at covering late-stage development costs including manufacturing scale-up [S1][S9]. These federal collaborations provide both funding leverage and regulatory engagement advantages.

Business Model: Focused Pipeline and Leveraged Development

Edesa operates a lean biopharmaceutical model emphasizing acquisition and development of promising drug candidates rather than basic research. The company primarily in-licenses clinical-stage assets—such as the CXCL10-targeting EB06 and TLR4-targeting EB05—from academic or biopharma sources, streamlining costs associated with discovery phases [S1].

Manufacturing is outsourced exclusively to third-party contract manufacturing organizations (CMOs) that handle both clinical trial material supply and prospective commercial production. This approach reduces capital expenditure demands on building proprietary infrastructure while enabling scalable production as candidates advance toward commercialization [S1].

Revenue prospects depend largely on future license agreements or partnerships to commercialize assets like EB01 (daniluromer cream for Allergic Contact Dermatitis), which is currently staged for partnering [S1]. The company’s strategy leverages selective late-stage development investments combined with external funding mechanisms—including government grants—to preserve cash while enhancing pipeline value.

Competitive Positioning Within Immuno-Inflammatory Therapeutics

Edesa’s competitive moat is anchored by validated monoclonal antibody technologies targeting immuno-inflammatory pathways that are clinically underserviced. For instance, EB06 neutralizes CXCL10—a chemokine implicated in autoimmune depigmentation—with demonstrated preclinical efficacy translating into an attractive dermatological indication lacking approved targeted biologics [S1]. Likewise, EB05 targets Toll-like receptor 4 to temper hyperinflammation during ARDS episodes where mortality remains high despite standard care.

Intellectual property exclusivity arises from exclusive licensing agreements secured since inception (e.g., Yissum License Agreement) combined with ongoing patent filings such as provisional claims covering new paridiprubart indications extending patent protection through the early to mid-2030s [S1][S19].

Further competitive advantages stem from established governmental relationships facilitating program grants—which help offset development risk—and from clinical data that substantiate differentiation versus generic immunosuppressive approaches or off-label polypharmacy commonly employed within these difficult indications.

Nevertheless, competition remains notable given the intense focus globally on immuno-inflammatory diseases; however, Edesa’s focus on niche indications backed by mechanism-driven novel biologics helps isolate it within these crowded research landscapes.

Key Growth Drivers: Clinical Progress and Strategic Partnerships

Edesa’s growth trajectory hinges critically on multiple quantifiable operational levers:

- Clinical Progress: Initiation of Phase 2 enrollment for EB06 stands as a leading indicator of execution ability and potential future market entry timing. Positive safety/tolerability evidence supports this advance [S2][S3].

- Regulatory Engagement: Satisfactory interactions with Health Canada have been replicated with the FDA preparatory dialogue reflecting progress toward US study initiation—a key market expansion opportunity.

- Commercial Partnerships: The dermatology asset EB01 is actively being positioned for partnering deals which could unlock upfront payments or royalties; such collaborations are essential given Edesa’s outsourced commercialization model [S1].

- Government Funding: Sustained grant support from Canadian government programs underpins financial coverage of pivotal trials and manufacturing scale-up expenses—critical enablers mitigating upfront capital burden [S1][S19].

- Pipeline Expansion: Additional indications exploration for paridiprubart—including chronic disease applications—and potential identification of new immuno-inflammatory candidates through licensing supports long-term portfolio growth.

These factors together provide multiple touchpoints to assess momentum via enrollment rates, partnership deal announcements, government milestone payments received, and regulatory submission timelines.

Risks and Constraints: Capital Adequacy and Market Acceptance

Despite operational strengths, Edesa explicitly states substantial doubt about its ability to continue as a going concern without securing additional financing beyond present resources [S1][S2]. Its cash runway is limited relative to ongoing R&D expenditures given zero revenue generation as of the last report period [F1].

While Q1 2026 balance sheet metrics reveal $10 million in cash equivalents supported by a current ratio of approximately 4.76—implying good short-term liquidity—the absence of revenues coupled with continued costly late-stage trials highlight acute dependency on raising external capital through equity raises or partner-funded programs [F1].

Additional risks encompass:

- Regulatory outcomes that could delay or deny marketing approvals;

- Competitive pressures inserting newer therapies into target markets;

- Reimbursement uncertainties affecting product uptake post-launch;

- Manufacturing scale-up complexities inherent in biologic therapeutics;

- Compliance challenges including cybersecurity threats or legal disputes impacting operations [S12][S16][S20].

These factors collectively suggest that near-term valuation will pivot on successful capitalization events intertwined with clinical pipeline de-risking.

Monitoring Points: Regulatory Pathways and Capital Raise Timing

Key upcoming milestones warrant close observation:

- FDA acceptance of IND/CTA protocols allowing EB06 Phase 2 patient enrollment slated midyear 2026.

- Receipt of regulatory decisions post-completion of the pivotal ARDS Phase 3 study with paridiprubart.

- Updates on partnering discussions regarding dermatology assets like EB01 signaling commercial traction.

- Progression details on ongoing U.S. government platform studies evaluating EB05's efficacy across diverse ARDS etiologies.

- Announcements related to additional fundraising rounds or licensing deals critical to sustaining development momentum.

Each catalyst carries asymmetric informational value offering sharp inflection points either validating business continuity vectors or flagging execution bottlenecks.

Financial Profile: Liquidity Snapshot and Funding Outlook

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $10mm | |

| 2026-03-31 | ||

| Current assets | $10mm | |

| 2026-03-31 | ||

| Current liabilities | $2mm | |

| 2026-03-31 | ||

| Current ratio | 4.76x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Date |

|---|---|---|

| Cash & Equivalents | 10,000,000 | |

| 2026-03-31 | ||

| Current Assets | 10,417,727 | |

| 2026-03-31 | ||

| Current Liabilities | 2,187,921 | |

| 2026-03-31 | ||

| Current Ratio | 4.76 | |

| 2026-03-31 |

As reported at quarter-end March 31, 2026, Edesa holds $10 million in cash equivalents backed by approximately $10.4 million in current assets against roughly $2.2 million current liabilities yielding a comfortable current ratio near 4.76 [F1]. This suggests short-term obligations are well-covered financially.

However, absence of product revenues places substantial reliance on future capital markets access or partnership-generated funds to bridge operational expenses predominantly linked to ongoing clinical trial activities [S2][S3].

This analysis is based solely on information publicly disclosed by Edesa Biotech as per SEC filings through May 14, 2026. It aims to provide an objective assessment of operating developments within the constraints imposed by available data without offering investment advice or predictions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments