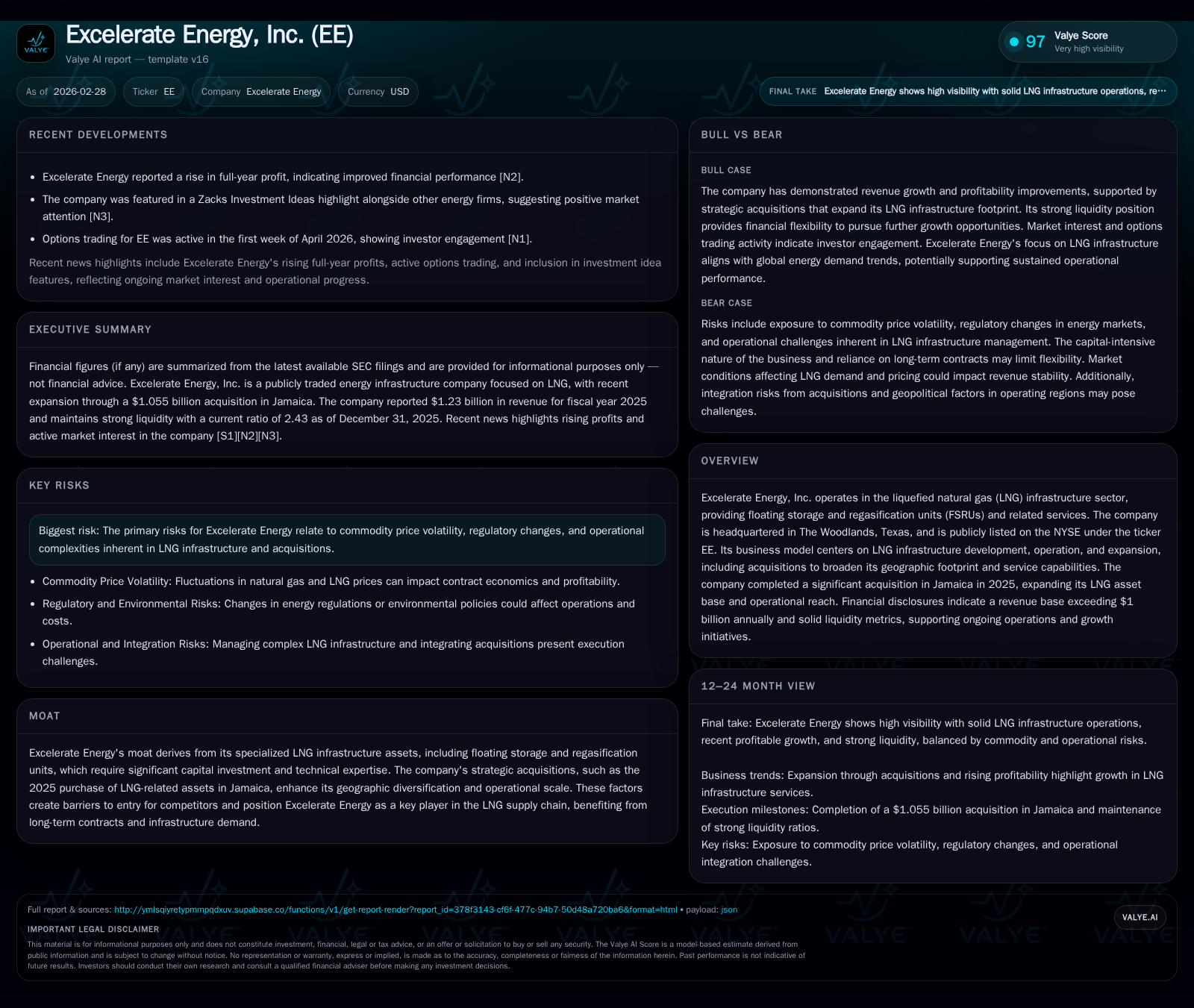

Excelerate Energy Expands Global LNG Reach with Strategic Acquisitions and Robust Cash Flows

The company's steady revenue growth and liquidity bolster its position in global LNG infrastructure amid expanding contract backlog and recent acquisitions.

Excelerate Energy, Inc. has evolved its financial profile from revenue fluctuations tied to project timings toward a more stable operating cash flow base, supported by a globally diversified fleet of floating regasification terminals. The 2025 acquisition of LNG assets in Jamaica expanded its operational footprint across 14 countries, reinforcing its scale advantages amid rising LNG demand. Key contracts secured for new floating regasification terminals signal further revenue visibility, while disciplined capital allocation has enhanced liquidity and shareholder returns through dividends and buybacks.

Strong Foundations: Historical Revenue and Profit Dynamics

Excelerate Energy’s financial history over the last four fiscal years reveals pronounced top-line variability driven by project ramp-ups, asset acquisitions, and operational expansions. Revenue peaked at approximately $2.47 billion in FY2022 but contracted sharply to $1.16 billion in FY2023 before rebounding to $1.23 billion in FY2025 [F1]. Operating income followed an upward trajectory from $187 million in FY2022 to nearly $267 million by FY2025. This growth in profitability despite fluctuating revenues signals improving operational efficiency and higher capacity utilization across Excelerate’s fleet of floating storage and regasification units (FSRUs).

Operating cash flows consistently grew from $225 million in FY2022 to over $461 million in FY2025, marking an 88.7% jump last year—an indicator of strong cash conversion fueled by long-term take-or-pay contracts underpinning baseline revenues [F1]. Dividends paid showed a modest yet steady rise parallel to free cash flow expansion.

Historical performance (annual)

| FY | Rev ($bn) | CFO ($mm) | OpInc ($mm) | Rev YoY |

|---|---|---|---|---|

| 2025 | 1.2 | 461 | 267 | +44.3% |

| 2024 | 0.9 | 244 | 215 | -26.5% |

| 2023 | 1.2 | 232 | 211 | -53.1% |

| 2022 | 2.5 | 225 | 187 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) |

|---|---|

| 2025 | 9 |

| 2024 | 3 |

| 2023 | 3 |

| 2022 | 1 |

Source: SEC companyfacts cache [F1].

Note: Revenues sharply declined after FY2022 due primarily to timing shifts associated with project completion phases and the absorption of acquired assets.

Driving Factors Behind Revenue Volatility and Growth Drivers

Several factors have contributed to revenue swings including delays or accelerated timelines of new terminals and variable contributions from legacy asset portfolios as projects complete or transition into steady-state operations [S1]. Project startup delays or cancellations potentially reduce short-term revenues but allow Excelerate to avoid cost overruns amid inflationary pressures noted in global supply chains.

The major acquisition completed in early-2025—the purchase of Jamaica LNG assets for approximately $1.055 billion—not only broadened the company’s geographical footprint but also bolstered near-term revenue streams [S1][S16]. The acquisition integration presents opportunities for operating cash flow accretion but entails managing integration risks discussed in filings [S1].

The company’s business model leans heavily on take-or-pay agreements which require customers to pay irrespective of usage volumes, providing predictable cash flows that help buffer against natural gas commodity price volatility [S1]. Regasification service demand has been affected by LNG market cycles; however, Excelerate’s emphasis on flexible FSRUs enables faster deployment relative to fixed onshore infrastructure, creating competitive advantages.

Global Footprint Expansion: The Impact of Recent Key Acquisitions

Excelerate operates or controls eleven floating regasification terminals worldwide alongside one onshore facility and a cogeneration plant [S1]. Its presence extends across fourteen countries including strategic coverage in energy-importing nations like Argentina, Bangladesh, Brazil, Finland, Germany, Jamaica (since acquisition), Iraq, Pakistan, UAE, and the United States.

The Jamaican acquisition notably enhanced the company’s footprint within the Caribbean LNG import sector—a region benefiting from increased energy security initiatives and reduced carbon footprints via natural gas substitution [S1][N11]. Operating floating storage regasification units (FSRUs)—vessels that can be redeployed—form the backbone of Excelerate’s infrastructure moat due to their mobility, relatively lower capital cost compared to land-based terminals, and quick turnaround times essential for dynamic global LNG markets.

Underlying Demand Trends in LNG Infrastructure Services

Secular trends supporting robust demand for LNG infrastructure include growing reliance on natural gas as a cleaner transitional fuel within power generation mixes aiming at decarbonization [S1][N14]. Increasing LNG consumption across emerging economies drives regas capacity utilization upward. Notable service activities such as ship-to-ship transfers—exceeding 3,800 transactions since inception—underline Excelerate’s operational expertise vital for maintaining uptime amid complex logistical challenges inherent to flexible floating terminals [S1].

However, sector cyclicality remains a factor as spot LNG price oscillations influence pipeline export volumes globally impacting contracted throughput levels; nonetheless, Excelerate mitigates this risk through diversified long-term contracts across regions with varying market dynamics.

Readying for Growth: Contract Backlog and Pipeline Prospects

Looking forward, Excelerate is commissioning a new floating regas terminal built by Hyundai Heavy Industries expected online Q3 2026 under a firm five-year contract with Iraq's Ministry of Electricity [S1]. This addition exemplifies ongoing capital investments designed to expand capacity underpinned by secure contractual revenue.

The company also benefits from contract renewal efforts globally alongside potential synergies from its Jamaican acquisition—a source of incremental operating cash flow accretion highlighted in recent disclosures [N3][N8][N11]. Long-term take-or-pay contracts solidify revenues by ensuring minimum throughput usage payments even amid demand fluctuations.

Capital Allocation Discipline: Cash Flow Strength, Dividends, and Buybacks

Excelerate demonstrates disciplined capital allocation aligned with operational cash flow growth evidenced by an increase from $244 million CFO in FY2024 to over $461 million in FY2025 (+88.7%) [F1]. Free cash flow approximates $460 million after accounting for capex indicating excess funds available for shareholder returns and debt servicing.

Dividend distributions have steadily risen year-over-year reaching ~$8.5 million in FY2025 from just over $1.3 million in FY2022 reflecting management's measured enhancement of shareholder returns concurrent with balance sheet strengthening [F1][S6][S8].

Share repurchase activity has been regularly disclosed across multiple quarters suggesting another avenue of capital return accompanying dividends though specifics vary per announcement periods . Such strategies underscore a commitment to delivering value while preserving flexibility amid ongoing project developments.

Financial Health Snapshot: Liquidity, Debt Profile, and ROE Analysis

Liquidity metrics reflect robust short-term financial health with a current ratio of approximately 2.43 at fiscal year-end 2025 highlighting ample buffer between current assets ($753 million) and liabilities ($310 million) [F1].

Equity grew meaningfully over four years culminating at $2.23 billion end-FY2025 driven primarily by retained earnings retention commensurate with infrastructure investment cycles [F1]. Despite increasing equity base profitability ratios remain modest; return on equity approximates a subdued ~0.6% owing largely to capital-intensive nature typical for floating LNG assets where depreciation schedules weigh on net income realization [F1].

Debt arrangements carry covenants tied explicitly to floating terminal collateralization limiting leverage flexibility but securing favorable financing terms critical given heavy capex demands documented within filings [S1][S14]. Maintaining conservative leverage remains paramount amid potential regulatory approvals needed for expansions.

Operational Risks and Regulatory Headwinds in LNG Markets

Risks articulated include vulnerability to cost inflation affecting materials and labor leading to delayed project startups or cancellations which can materially impact revenues temporarily [S1]. Regulatory permitting complexity varies significantly across jurisdictions requiring sustained effort to secure environmental approvals essential for construction and operation.

Geopolitical instability in certain countries poses political risks that can disrupt operations directly or indirectly through supply chain constraints. Operational uptime is critical given LNG commodity supply volatility; any disruptions or capacity constraints within regas facilities can incur penalty costs or customer dissatisfaction.

Crew shortages—a notable issue within maritime sectors post-pandemic—may impact terminal staffing costs potentially elevating operating expenditures while precision logistics around ship-to-ship transfers demand experienced coordination failing which operational efficacy would suffer dramatically [S1].

Investor Takeaways: What to Watch in Upcoming Earnings and Guidance

Market observers should focus on upcoming earnings releases expected between Q2/Q3 calendar year 2026 which will reveal commissioning progress on new South Korean-built terminal serving Iraqi power needs alongside early integration results from the landmark Jamaican asset acquisition reported earlier this year [N3][N8][N11]. Key performance indicators include EBITDA margin trends reflecting operating leverage gains as newer units commence steady operations.

Additionally important are updates regarding contract renewal pipelines especially within core markets such as Argentina or Bangladesh where contract extensions can secure future revenue streams insulating against cyclicality noted within spot LNG markets.

Accruals around operating cash flow expansion remain crucial as these funds directly drive dividend growth potential plus capacity for opportunistic share repurchases reinforcing shareholder returns amidst selective capex deployment targeting high-return projects.

This analysis synthesizes reported data and public disclosures as of February 28, 2026 without speculative forecasts or investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments