EVEREST GROUP's Earnings and Strategic Shifts Unpacked

EVEREST GROUP blends steady revenue growth with strategic renewal rights sales and leadership changes amid regulatory complexities.

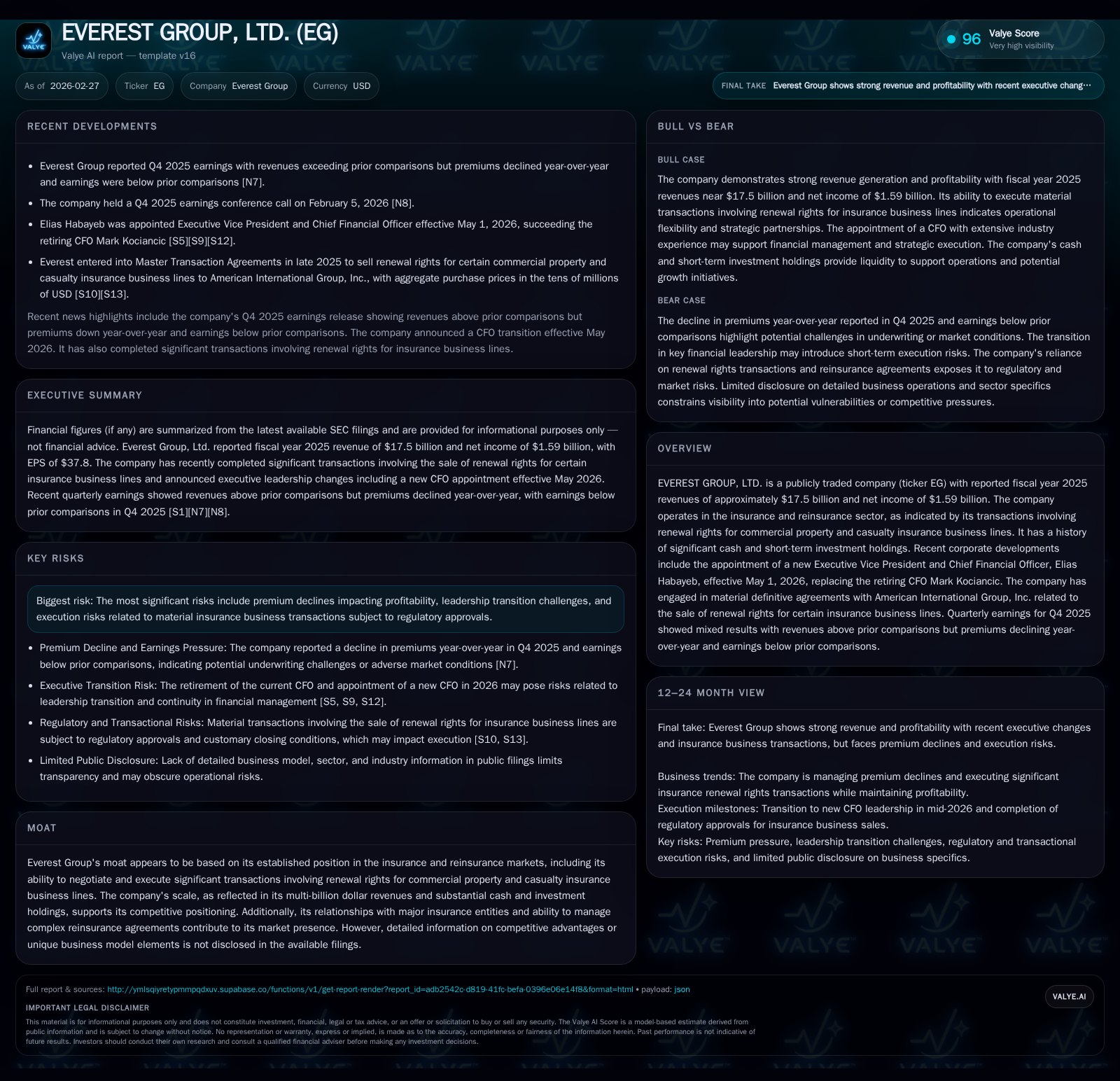

EVEREST GROUP delivered modest top-line expansion in fiscal year 2025, reaching $17.5 billion in revenues with a net income recovery after prior dips, underscored by execution of substantial renewal rights transactions with AIG. While its premium income shows pressure, particularly in Q4 2025, strategic asset sales and adept capital deployment through sizable share repurchases underscore management’s focus on portfolio optimization and shareholder returns. The upcoming CFO transition introduces execution risks but also potential strategic recalibration as the company navigates regulatory approvals tied to its multi-jurisdictional insurance business dealings.

Revenue Growth Trajectory and Profit Volatility From 2023 to 2025

Across the latest three full fiscal years ending December 31, Everest Group has demonstrated consistent top-line progression albeit at a decelerated pace recently. Revenues advanced from $14.6 billion in FY2023 to nearly $17.5 billion in FY2025—a compound gain of over 6% across two years but moderating to an annual increase of just 1.2% between FY24 and FY25 [F1]. This rebound masks underlying volatility: net income peaked at $2.52 billion in FY23 before retreating sharply then rebounding to $1.59 billion by end-2025, indicating fluctuations driven by underwriting outcomes and perhaps investment returns.

Gross written premiums (a key industry metric) trends implicitly influenced these earnings swings as Everest cycles through renewal book adjustments and exposure containment strategies common in commercial property and casualty reinsurance markets [S1]. Meanwhile, equity grew steadily from approximately $13.2 billion in FY23 to $15.46 billion by FY25, supporting stable risk capital buffers that underpin underwriting capabilities [F1]. Approximate return on equity calculated around 10.3% at fiscal year-end 2025 reflects moderated profitability consistent with a disciplined reserve and risk load posture.

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 17.5 | 1.6 | 3.1 | +1.2% | +15.9% |

| 2024 | 17.3 | 1.4 | 5.0 | +18.5% | -45.5% |

| 2023 | 14.6 | 2.5 | 4.6 | +21.0% | |

| 2022 | 12.1 | 3.7 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 797 | 10.3 |

| 2024 | 200 | 9.9 |

| 2023 | 0 | 19.1 |

| 2022 | 61 |

Source: SEC companyfacts cache [F1].

Note: Revenue YoY and Net Income YoY reflect the change from previous fiscal year; CFO YoY computed where comparable data exists.[F1]

Impact of Renewal Rights Sales on Everest’s Business Model

A salient development shaping Everest’s operational landscape is the strategic sale of renewal rights related to its commercial property and casualty insurance books spanning multiple geographic footprints, notably agreements concluded with American International Group (AIG). These transactions include the ROW Master Transaction Agreement consummated October 26, 2025, involving Everest’s branches in Australia and Singapore plus select U.S.-based businesses, aggregating purchase consideration around $252 million plus an additional $30 million fee for transaction origination services [S11][S15].

Parallel to this is the EU Master Transaction Agreement concerning certain UK-based commercial lines with a purchase price of approximately $49 million contingent on customary regulatory approvals including those from the European Commission [S11][S15]. Under these accords, Everest conveys renewal rights—the privileged ability to renew or replace insurance policies explicated under sophisticated contract terms—for defined lines of business while continuing policy administration supported via transition service fees of roughly $10 million monthly for a nine-month period into early/mid-2026.

This approach constitutes a form of deliberate 'book management' where Everest selectively monetizes segments of its policy renewal stream to optimize capital use while mitigating portfolio concentration risks—a common strategy within P&C reinsurance sectors facing margin pressure . Upfront proceeds bolster liquidity allowing for reinvestment or capital returns as evidenced elsewhere.

Quarterly Dynamics: Premium Declines Versus Revenue Beats in Q4 2025

The fourth quarter of calendar year 2025 painted a nuanced picture: despite reported revenues surpassing analyst targets, gross written premiums experienced a year-over-year decrement—highlighting tension between volume contraction and pricing or fee enhancements [N6][N8][S3][S9]. This dichotomy speaks to Everest's premium base encountering headwinds from competitive pricing environments and potential risk retentions by cedants.

Underwriting income metrics reflected heightened loss ratios influenced by attritional claims frequency underpinning combined ratio pressures—where the ratio encompasses loss payouts plus expenses relative to earned premiums vital for evaluating underwriting profitability [N9]. Investment margins partially offset underwriting softness but not sufficiently to fully counterbalance decline in premiums.

Such quarterly trends warrant vigilance given their implications for full-year balance sheet health and signal challenges for traditional reinsurance players grappling with cyclical premium cycles amid evolving catastrophe loss landscapes .

New CFO Appointment and Leadership Transitions: Implications for Strategy

Leadership shifts surfaced as prominent corporate milestones with Elias Habayeb slated to assume the Executive Vice President and Chief Financial Officer mantle effective May 1, 2026 following Mark Kociancic's retirement post Q1 reporting cycle [N7][S19][S21]. Habayeb arrives from Corebridge Financial with prior high-level finance roles at AIG indicating deep sector expertise aligned with Everest’s strategic imperatives.

This transition carries inherent 'leadership transition risk' principally through potential disruption of financial planning continuity amid active material deals governance including renewal rights realization and capital structure adjustments [S21]. Compensation arrangements suggest strong retention incentives signifying importance attached by Everest board to smooth handover.

Given Habayeb’s anchoring experience at entities engaged in sizeable insurance portfolios realignment strategies, his influence may presage further pragmatic capital discipline or portfolio optimization initiatives organically fitting Everest's trajectory . However, near-term execution diligence remains paramount.

Capital Allocation: Share Repurchases, Dividend Policy, and ROE Analysis

Everest has demonstrated aggressive share repurchase activity juxtaposed with absence of recent dividend payments—a hallmark indicating prioritization of stock buybacks as primary shareholder return mechanism over cash dividends [F1][S8][S14]. Notably:

- In FY25, Everest repurchased shares worth approximately $797 million versus just $200 million in FY24 representing nearly a fourfold increase aimed at capital structure refinement.

- No notable dividends were paid during recent years reflecting management's preference or possibly constraints on distributable cash given insurance regulatory frameworks.

- Operating cash flow experienced a pronounced decline from approximately $4.96 billion in FY24 to $3.07 billion in FY25 (-38%), raising questions around claims payment timing or working capital fluctuations that merit monitoring despite sustained profitability.

- Equity capital base expanded steadily maintaining solid capitalization ratios underpinning roughly a consistent ROE near the low double digits (~10.3%)—a solid if unspectacular return metric within reinsurance norms.

This constellation delineates a capital deployment mix balancing shareholder value extraction against operational demands inherent in volatile reserve-driven industry dynamics .

Regulatory and Execution Risks from Major Transaction Agreements

The material definitive agreements implemented around renewal rights are encumbered by customary regulatory approvals particularly highlighted by requisite antitrust clearances within the European Union jurisdiction affecting the EU Master Transaction Agreement closing prospects [S4][S6][S11]. Such approvals represent non-trivial execution risk factors given cross-border complexities typical of P&C insurance arrangements altering control or influential policy segments.

Moreover, contingent purchase price adjustments linked to actual premium performance thresholds introduce potential post-closing financial considerations adding another layer of transactional uncertainty [S11][S18]. Litigation or challenge risks appear limited based on disclosures but remain monitored normative hazards.

These execution factors resonate universally within complex insurance M&A/fundamental portfolio realignment efforts where multi-stakeholder consents swing timelines—highlighting importance of milestone tracking for investors focused on definitive deal outcomes completion.

What to Watch: Upcoming Approvals, Premium Trends, and Underwriting Metrics

Moving forward investors should carefully observe several critical indicators shaping Everest’s near-term narrative:

- Status updates on EU antitrust clearance completion for renewal rights deals along with any disclosed modifications or conditions.

- Commercial P&C premium trends across post-renewal books signaling either stabilizing pricing environment or further tightening impacting revenue base.

- Evolution of combined ratio metrics reflecting loss experience offsetting—or failing to offset—expense structures specifically excluding realized investment gains/losses.

- Official announcements concerning closing milestones for both ROW and EU Master Transaction Deals which materially affect expected future cash flows.

- Transition progress under CFO Elias Habayeb focusing on messaging around financial discipline post-May 2026 assuming office.

Additionally, competitive premium pricing behaviors observable across peers such as Assurant or RGA (see accompanying sector news) provide broader context for comparative analysis within reinsurer cohorts navigating similar market dynamics [N2][N3][N4][N14].

Disclaimer: This report synthesizes publicly filed data without offering investment recommendations or forecasts beyond documented disclosure.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments