Elme Communities Accelerates Asset Liquidation in Strategic Wind-Down

Elme Communities reports significant progress in its Plan of Sale and Liquidation with key property sales advancing toward completion.

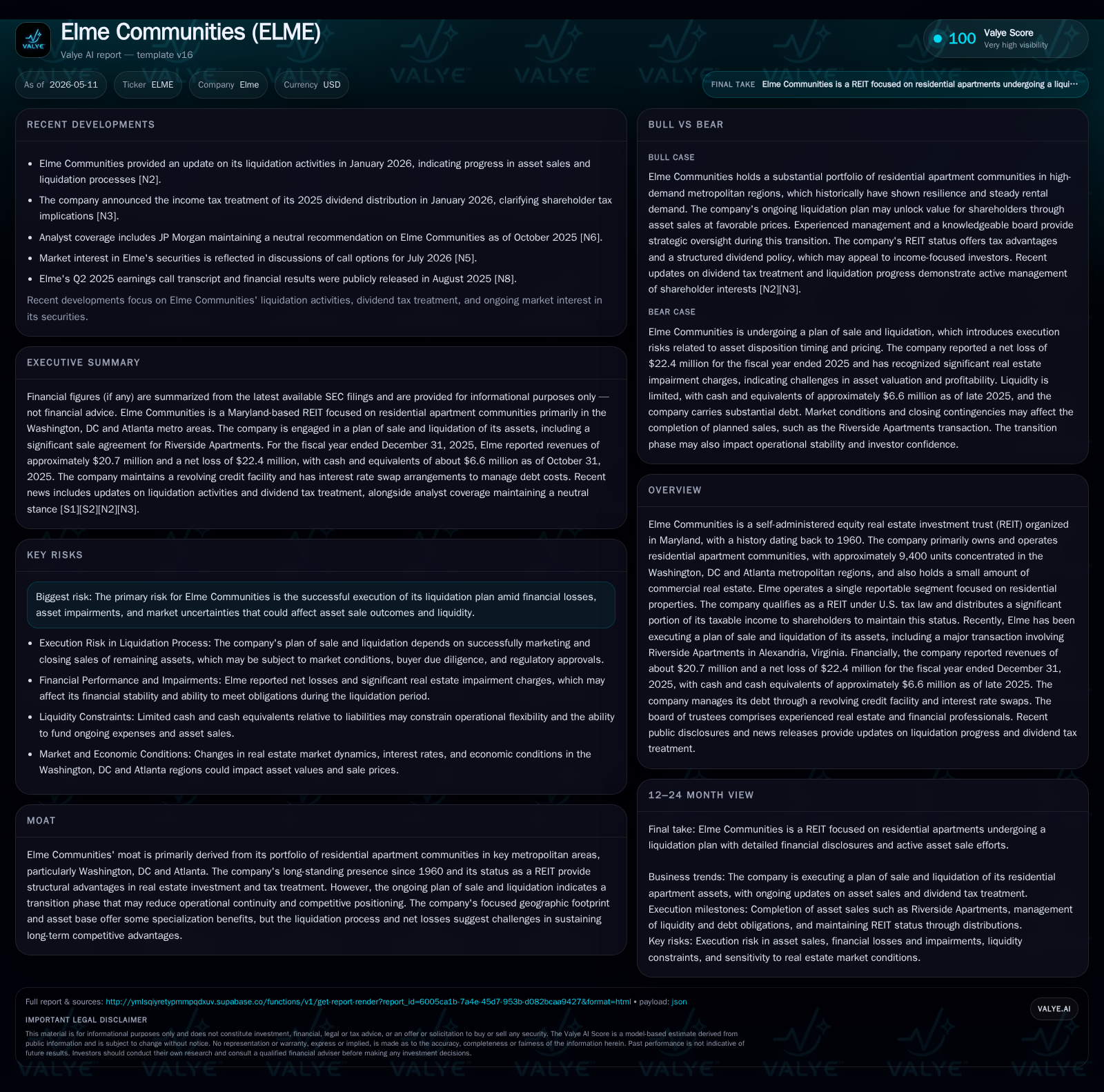

In its latest quarterly filing dated May 11, 2026, Elme Communities disclosed the sale of five out of ten remaining properties following a 19-asset portfolio transaction last November. A major sale agreement for Riverside Apartments, a 1,222-unit community in Alexandria, Virginia, valued at $280 million is underway with closing expected by July 6, 2026. Operating under a shareholder-approved Plan of Sale and Liquidation, Elme’s business model is transitioning from active residential REIT operations toward winding down via asset dispositions. Though asset sales are progressing, persistent net losses and liabilities highlight the challenges inherent in the liquidation process. Monitoring contract closings and liquidity execution milestones remains critical.

Quarterly Operating Update: Progress on Asset Sales

Elme Communities’ most recent quarterly report filed on May 11, 2026 [S2] alongside an associated current report [S3] provides a detailed update on the progress of its approved Plan of Sale and Liquidation. Since the November 12, 2025 completion of a significant portfolio sale comprising 19 assets to Cortland Partners’ affiliate, Elme has sold five out of the ten residual properties it retained post-transaction. This substantiates meaningful advancement toward the wind-down of its real estate holdings.

A particularly notable transaction within this liquidation effort is the May 8, 2026 executed purchase and sale agreement for Riverside Apartments in Alexandria, Virginia. This asset, totaling 1,222 residential units plus undeveloped land, carries a contract price of $280 million [S2]. The deal terms outline a $4.5 million aggregate earnest money deposit with staged installments tied to inspection period milestones—$1.5 million due within two business days post-signing and $3 million due upon inspection period expiration on June 4, after which only seller breach contingencies allow termination without forfeiture.

The closing date is set for on or before July 6, 2026 albeit subject to customary real estate transaction contingencies [S2]. While these contractual conditions introduce typical operational risks over timing and consummation certainty, the arrangement signals Elme’s ability to orchestrate large-scale asset transfers under its liquidation plan. Concurrently, Elme holds four additional purchase agreements for remaining properties outside ongoing inspection periods equating to potential aggregate gross proceeds approximating $431 million [S3].

Business Model Overview and Portfolio Composition

Established in Maryland with operations dating back to 1960, Elme Communities has historically functioned as a self-administered equity real estate investment trust (REIT) focused predominantly on ownership and operation of multifamily residential communities [S1]. The company currently manages approximately 9,400 residential units concentrated strategically within Washington DC and Atlanta metropolitan areas—a footprint offering geographic specialization but also concentration risk given market-specific dynamics [S1].

Revenue generation principally derives from rental income streams across residential leasing contracts complemented by ancillary commercial property rental revenue from a nominal commercial asset base [S1]. As a qualified REIT under U.S. tax law requirements, Elme distributes most taxable income to shareholders to maintain favorable tax treatment.

The company presently reports all operations within one single reportable segment centered on residential real estate [S1]. However, an active Plan of Sale and Liquidation approved by shareholders in October 2025 marks a transition from ongoing property management toward systematic portfolio divestiture culminating in dissolution. This shift imposes revenue contraction pressures coupled with elevated operating expenses related to severance, retention incentives, wind-down administrative overheads, and impairment charges linked to asset write-downs recorded in recent quarters [F1], [S3].

Competitive Position and Market Footprint

Elme’s competitive stance is defined by its focused exposure to urban apartment communities within two major metropolitan regions. Such geographic concentration potentially enables operational efficiencies deriving from localized property management expertise and deeper understanding of regional housing demand drivers [S1]. However, the scale is modest relative to larger diversified or institutional multifamily REIT peers that can leverage expansive portfolios across multiple markets achieving enhanced liquidity and capital deployment options.

The company’s ongoing liquidation diminishes its operational scale further as assets exit the portfolio—undermining continuity benefits typically associated with large REITs competitively positioned for rental growth or redevelopment opportunities [S2], [S3]. Moreover, the pace at which core assets like Riverside Apartments are monetized will materially impact relative market valuation positioning compared with competitors maintaining stable or growth-oriented holdings.

Strategically strong locations such as Alexandria influence buyers’ appetite given local housing demand fundamentals; nonetheless potential regulatory hurdles such as tenant purchase rights legislated at county or city levels require active navigation during transaction closings [S20], adding complexity uncommon for buyers accustomed to more streamlined acquisition processes.

Growth Opportunities Within Wind-Down Strategy

Despite the cessation of traditional growth trajectories implicit in active property operations or acquisitions, Elme’s value creation pivotally depends on execution discipline around sale timing optimization to maximize gross proceeds versus market conditions [S2], [S3]. The successful negotiation of multi-property contracts evidences buyer interest supporting throughput velocity.

Capitalizing on rising housing demand cycles or availability bottlenecks within core metro regions could enhance pricing outcomes if sellers effectively coordinate sales windows rather than forced fire sales constraining valuation ambitions. Additionally, efficient management of liquidation costs encompassing legal fees, brokerage commissions (noted explicitly among transaction expenses), severance packages for retained employees pivotal during transition phases contributes positively toward net distributable proceeds estimates [S3], [S14].

Maintaining tenant occupancy or stabilizing cash flow ahead of closing events can also support working capital generation alleviating interim liquidity pressures intrinsic to winding operations down while avoiding precipitous drops in underlying asset valuations triggered by distress indicators visible to market observers.

Risk Factors Impacting Liquidation and Execution

A primary risk lies in successfully completing all pending transactions within established deadlines including Riverside Apartments whose contractual inspection period expires June 4 followed by an anticipated close prior to July 6 - failure here would materially disrupt projected cash flow timing and distribution schedules [S2]. Although standard seller breach clauses provide some contractual recourse protection against deposit forfeiture scenario risks remain around buyer diligence findings or financing contingencies.

Regulatory risk overlays related to preservation of REIT status during liquidations impose compliance cost burdens; failure to adhere could trigger adverse tax consequences diminishing net distributable value or complicating trust dissolution timelines [S20], [S1]. Further legal uncertainties include latent litigation from disgruntled stakeholders dissatisfied with timing or distribution allocations post-liquidation initiation.

Upcoming Catalysts and Monitoring Points

Key near-term events warranting monitoring encompass:

- Expiration of Riverside Apartments’ buyer inspection period scheduled June 4, post which earnest money deposit becomes nonrefundable absent seller breach - signaling elevated commitment level from buyer side [S2].

- Anticipated closing deadline for Riverside Apartments near July 6; successful consummation confirms substantial liquidity milestone critical for further liquidating distributions.

- Progress updates regarding other properties under contract where three out of four have cleared inspection periods underscoring forward momentum toward full portfolio disposition following completion of initial large-scale Cortland portfolio sale [S3].

- Announcements regarding final schedule plans for trust dissolution including timing around ceasing public listing obligations given natural dependencies upon asset monetization completeness.

- Watch points include any deviations announced relating to transaction cost assumptions impacting available distributable funds or unexpected capital requirement escalations extending operational overhead duration beyond prior guidance.

Financial Snapshot: Liquidity, Leverage, and Earnings

From a financial perspective supported by filings up through late FY2025 endpoints: Elme reported revenue approximating $20.7 million contrasted against an operating loss exceeding $122 million over latest periods examined while incurring net losses close to $22.4 million annually highlighting sustained profitability pressures amidst liquidation activities [F1]. Cash reserves stood at roughly $6.58 million near October quarter-end indicating constrained liquidity vis-à-vis estimated outstanding debts which collectively approached $85.3 million net leverage when factoring estimated debt levels less cash balances harmonized with prior debt disclosures from earlier periods given absence of precise recent total debt confirmations pending updated filings [F1], [S3].

Debt funding arrangements tied notably to a $520-million senior secured term loan underpin financing necessary for transitional capital needs throughout sales process including bridge funding obligations related to retained properties until closing events occur; timely repayment hinges primarily upon successful disposal proceeds conversion per planned sequence outlined in corporate disclosures [S18], [S24]. Managing interest expense load amid contracting earnings remains an execution focus alongside efficient administration cost controls during ongoing wind-down overhead realization budgets inclusive of retention incentives disclosed driving increased operating expense lines thereby compressing marginal distributable funds available after covering explicit attritional operating liabilities.[S8],[S12]

This analysis synthesizes available SEC disclosures reflecting Elme Communities' ongoing transformation from an operator toward complete liquidation under shareholder-sanctioned plans designed explicitly for orderly asset disposition aimed at maximizing shareholder returns despite operational headwinds inherent in such transitions. Investors should closely monitor upcoming transactional milestones referenced above as critical indicators shaping ultimate value realization achievable through completion probabilities realized within established contractual frameworks.

This content is intended solely for informational purposes derived from publicly available SEC filings as indicated by citation markers; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments