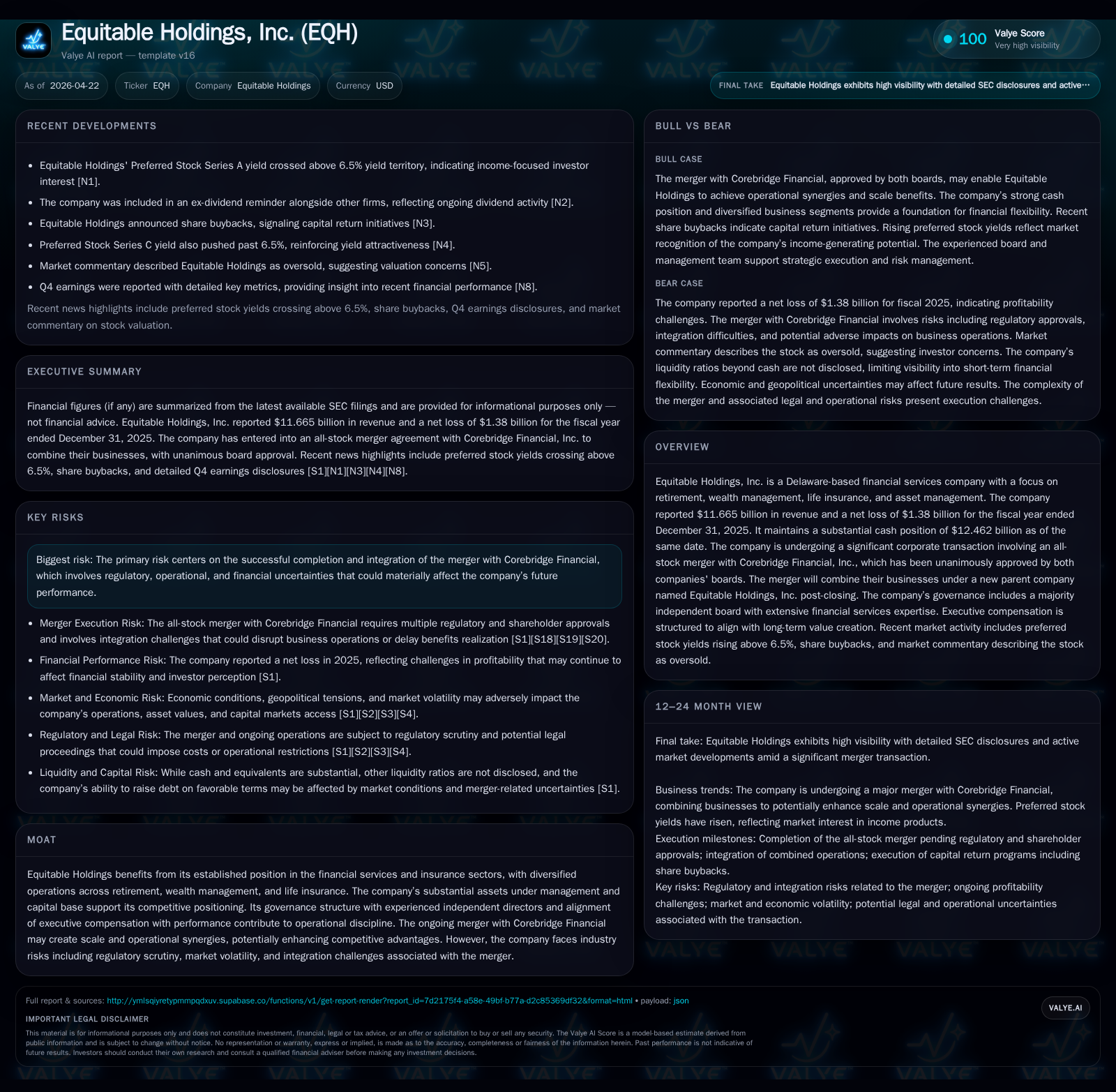

Equitable Holdings Leverages Merger Momentum to Strengthen Market Footprint

Recent SEC filings reveal Equitable Holdings' strategic capital actions and merger preparations as it aims to leverage scale and synergy.

Equitable Holdings' latest 10-Q and 8-K filings highlight management’s active exploration of share repurchases prior to closing its all-stock merger with Corebridge Financial, signaling confidence in operational flexibility amid transactional uncertainties. The company’s core business, spanning retirement solutions, wealth management, and life insurance, remains structurally robust with record retirement sales and asset inflows reinforcing growth opportunities. However, 2025 marked a notable net loss year driven by merger-related costs and market pressures, underscoring integration risks as the combined entity pursues expense rationalization and enhanced competitive positioning through scale. Key upcoming milestones revolve around regulatory approvals, cost synergy realization, and capital allocation clarity that will inform a growth trajectory reshaped by the pending transaction.

Latest Operating Update: Insights from the 10-Q and Event Filings

Equitable Holdings’ latest quarterly report filed November 7, 2025 [S2] alongside a recent April 16, 2026 event filing [S3][S6] reveal proactive capital management activities tied directly to the pending all-stock merger with Corebridge Financial announced March 26, 2026 [S1][S13]. Management is actively exploring the possibility of repurchasing common shares before the merger closes—conditional upon waivers from Corebridge to bypass standard contractual prohibitions during the deal pendency. Though noncommittal regarding timing or magnitude of buybacks, this move signifies a degree of confidence in balance sheet flexibility despite transactional complexity.

Liquidity remains robust with cash and equivalents reported at $12.46 billion as of December 31, 2025 [F1], providing ample runway to support both strategic capital returns and integration-related expenditures. Such flexibility is essential given ongoing risks flagged around regulatory clearance delays and integration execution hurdles outlined in risk disclosures [S7][S25].

Decoding Equitable's Business Model and Product Quality

Equitable Holdings operates a multi-segment financial services model emphasizing retirement products (notably registered index-linked annuities or RILA), wealth management advisory services, life insurance offerings, and asset management functions [S1]. Revenue streams derive primarily from premium inflows on life insurance products, contractual fees on retirement portfolios including variable annuities with living benefits attached to RILAs, plus advisory fees from assets under advisement (AUA) within wealth management.

FY2025 highlights included record Retirement sales reaching $22.4 billion (+7% year-over-year) fueled by standout performance in RILA sales which grew by 8%, cementing leadership in this nuanced niche balancing principal protection with market participation [S1]. Parallel advances occurred within tax-exempt accounts benefiting from heightened demand for municipal-bond-linked structured products (+28%). Wealth Management experienced an outsized surge with advisory net flows skyrocketing +76% year-over-year to $8.4 billion, swelling total assets under advisement beyond $120 billion (+20%) [S1]. This indicates genuine client adoption ramping alongside increased penetration into high-net-worth segments.

Importantly, management has prioritized operational discipline through a multi-year expense reset initiative targeting sustainable cost bases allowing reallocation towards higher-return investments [S1]. Already achieving $120 million run-rate expense savings by end-2025 places the company on track for a $150 million target by 2027—a notable accomplishment given legacy complexity across segmented platforms [S1]. These efforts support improved product delivery quality via accelerated digital tools deployment for investment decision layering and risk oversight enhancements.

Competitive Positioning within Financial Services and Insurance

Equitable's competitive moat stems chiefly from scale advantages embedded in its substantial AUM/AUA footprint coupled with diversified revenue mix across less correlated segments—retirement annuities cushion against wealth advisory cyclicality while insurance underwriting stabilizes margins amid volatile markets [F1][S1]. The company holds preferred positions within the registered index-linked annuity sector—a growing market where principal protection features meet increasing longevity risk concerns among aging demographics.

Governance frameworks emphasize independence with a majority independent board comprised of seasoned financial services professionals ensuring strategic prudence and long-term value alignment [S1][S28]. Executive compensation is calibrated around performance metrics tied to sustained earnings growth and expense reduction accomplishments fostering operational rigor.

However, margin pressures observed alongside declining annual revenues (-6.2% in FY2025 per [F1]) reflect headwinds including unfavorable market movements impacting asset valuations as well as heightened mergers-related costs. Regulatory scrutiny remains intense given evolving frameworks governing indexed annuities product disclosures and capital adequacy standards exerting compliance cost burdens that partially erode pricing power [S7][N2]. Analyst sentiment such as Raymond James’ recent rating upgrade highlights respect for Equitable’s resilience but acknowledges sector cyclicality risks persisting [N1].

Growth Catalysts and Integration Risks Amid Merger Plans

The all-stock combination with Corebridge signals a transformational growth catalyst poised to create one of the largest U.S.-based diversified financial services firms under the Equitable Holdings name post-closing [S1][S3]. The merger agreement carefully structures governance equality with equal board representation from both entities ensuring balanced influence; executive leadership roles are split between legacy CEOs to promote continuity while enabling focused integration oversight —the current Equitable CEO assumes Executive Chair duties while Corebridge's CEO steps into President-CEO role for HoldCo [S10].

Strategic rationale revolves around unlocking operational synergies chiefly via merging overlapping functions such as back-office processing, technology platforms, scaling distribution efforts across retirement and wealth channels plus diversifying product offerings accessible cross-sell between client bases [S11]. The expected run-rate expense savings — estimated upwards of $150 million — align well with historical efficiency achievements postulated during pre-merger diligence phases.

Nonetheless, this transformation faces contingent execution risks: regulatory approvals remain uncertain given antitrust considerations surrounding combined market power; cultural harmonization challenges could delay synergy realization; unexpected merger costs or displaced client relationships may temporarily impact earnings trajectories; talent retention amidst integration-induced distraction constitutes another vulnerability [S25]. The company acknowledges these issues openly in filings underscoring careful mitigation planning but transparent about inherent deal uncertainty levels.

Key Developments to Monitor in the Coming Quarters

Observers should prioritize tracking progress on securing all requisite regulatory approvals—a gating item dictating closing timelines—and scrutinize subsequent proxy statements influencing shareholder voting outcomes essential for deal consummation [S3][S6]. Achieving announced run-rate cost savings targets by incremental benchmarks throughout the post-close phases will signal tangible integration traction.

Monitoring operating flow metrics including net flows within retirement products and advisory fees growth post-merger will indicate whether combined distribution channels realize anticipated cross-selling uplift. Meanwhile, management communication regarding capital deployment strategies—particularly if early share repurchases materialize as hinted—will shed light on confidence levels about pro forma free cash flow generation capacity.

Clarity on goodwill impairment exposure or other one-time charges related to combination accounting should also be assessed closely given their sizable impact on reported profitability metrics seen in FY2025 results discussed below.

Financial Profile Underpinning Strategic Outlook

Over the past three fiscal years ending December 31:

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|

| 2025 | 11.7 | -1380 | 0.7 | -6.2% | -205.6% |

| 2024 | 12.4 | 1307 | 2.0 | +18.1% | +0.4% |

| 2023 | 10.5 | 1302 | -0.2 | -24.9% | -27.1% |

| 2022 | 14.0 | 1785 | -0.9 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | ROE% |

|---|---|---|

| 2025 | 1450 | 1864.9 |

| 2024 | 1014 | 82.5 |

| 2023 | 919 | 49.2 |

| 2022 | 849 | 107.7 |

Source: SEC companyfacts cache [F1].

The flat-to-declining revenue trajectory in FY2025 contrasts with robust growth vectors reported in core retirement sales (+7%) reflecting pressures elsewhere possibly tied to equity markets or legacy contract runoff effects ([S1]). The substantial net loss of $1.38 billion primarily incorporates merger-related expenses including transaction costs, goodwill impairments attributable to fair value adjustments following deal announcement public disclosures ([S1]). Despite profitability softness at the bottom line, operating cash flow remained positive at $714 million supporting working capital needs and ongoing capital programs.

The erosion turning equity negative (-$74 million by end-2025) flags balance sheet stress likely linked to intangible asset writedowns inherent in merger accounting but mitigated by substantial liquidity reserves poised to fund near-term obligations safely ([F1]). Stock repurchase activity accelerated into FY2025 ($1.45 billion), demonstrating active shareholder return efforts even amid transformative transactions.

In sum, while short-term financials bear signs of transition turbulence exacerbated by transactional charges compounded with sector cyclicality effects—Equitable’s liquidity stronghold combined with proven expense control initiatives provide foundational stability underpinning strategic ambitions in concert with its merger partner Corebridge.

This analysis synthesizes Equitable Holdings' recent SEC filings and market disclosures without offering investment advice or price predictions. Readers should consider the presented facts alongside broader market information before forming conclusions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments