FitLife Brands Advances Profitability Amid Market Skepticism

FitLife Brands reported profitable fiscal year 2025 results while facing market concerns over income declines and transparency.

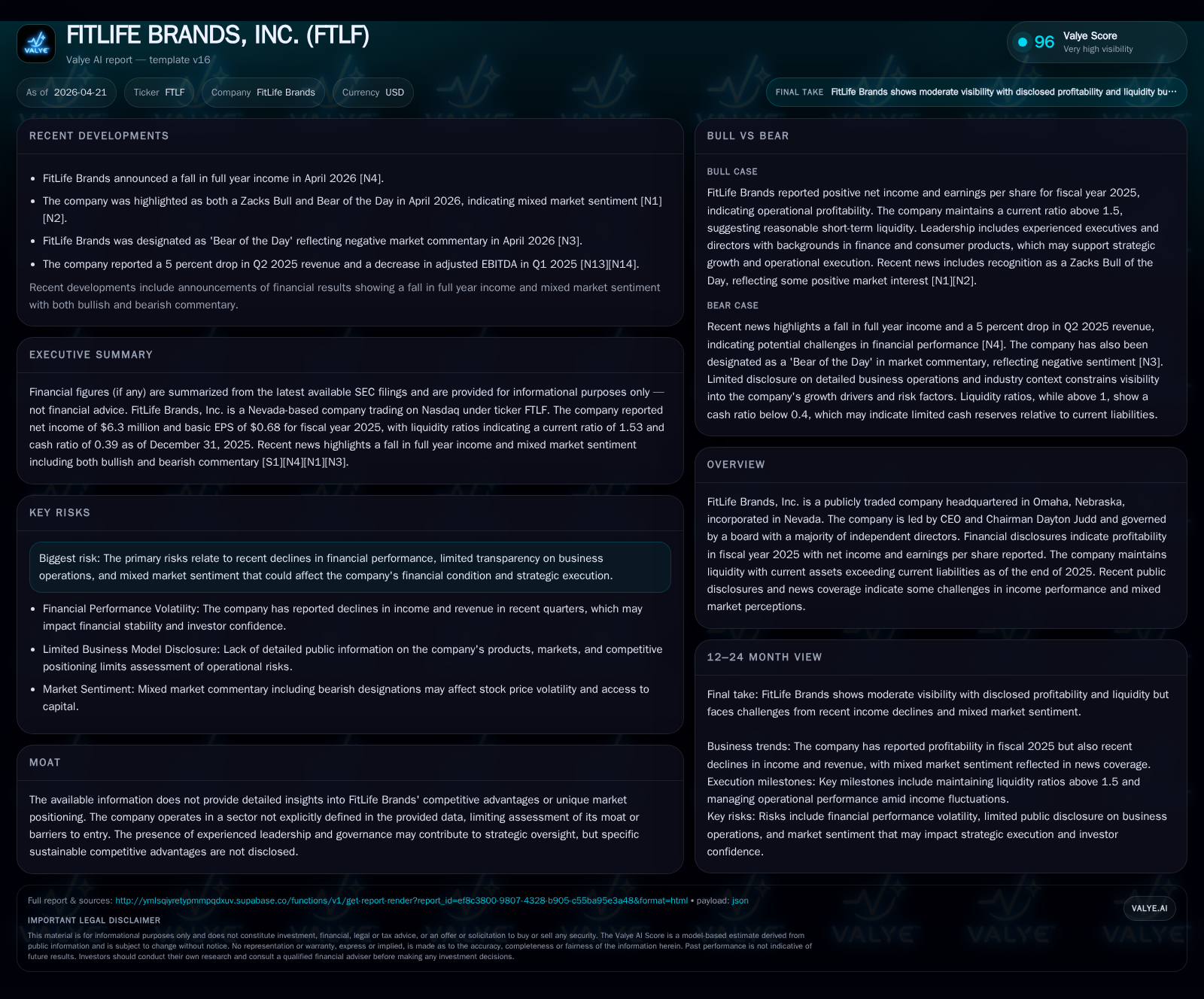

In its latest operating disclosures culminating in the April 2026 annual amendment and earnings call, FitLife Brands, Inc. affirmed profitability in FY2025 with $10.1 million operating income and $6.3 million net income despite a marked year-over-year decline from 2024 levels. The company sustains a solid liquidity position with a current ratio of 1.53 as of year-end 2025. However, market sentiment remains mixed amid ongoing challenges to income performance and limited clarity on business operations. FitLife’s business model centers on health and fitness-focused consumer brands, led by experienced governance but without disclosed structural moats. Growth catalysts rest on strategic market expansion and product relevance improvements, although risks related to financial volatility and perception linger.

Latest Operating Update: Q3 Trends and FY2025 Earnings Call Insights

FitLife Brands’ most recent quarterly report filed November 13, 2025 ([S2]) delivers the latest snapshot of operational performance entering the final quarter of the fiscal year. The company reported continued profitability for FY2025 featuring an operating income of approximately $10.1 million and net income near $6.3 million ([F1]). However, these figures represent meaningful declines compared to FY2024 — operating income fell by about 23% while net income dropped near 30%. Despite this erosion, liquidity remains strong with current assets at $33.1 million surpassing current liabilities of $21.6 million, yielding a healthy current ratio of approximately 1.53 ([F1]).

This financial foundation was reinforced in the April 1, 2026 earnings call ([S3]), where management acknowledged the downward pressure on full-year income but emphasized resilience through disciplined cost control and strategic focus shifts to stabilize margins. The attached transcript reveals a nuanced view: while revenues appear steady or modestly growing relative to prior periods, profitability pressures stemmed from increased operational expenses and marketing investments aimed at long-term brand reinforcement. Liquidity management also surfaced as a key theme underpinning ongoing operational flexibility.

These filings collectively sharpen near-term outlook clarity by confirming that FitLife maintains positive bottom-line results alongside cautious navigation of cost structures even amidst more challenging market conditions.

Business Model and Product Suite: Revenue Drivers and Customer Value

FitLife Brands operates primarily within the consumer health, wellness, and fitness sectors — segments characterized by robust but competitive demand for branded nutritional supplements, fitness products, and related lifestyle offerings ([S1]). The company’s revenue streams principally derive from sales of branded consumer products through direct-to-consumer channels including e-commerce platforms enhanced by digital marketing strategies.

While detailed product segment disclosures remain limited in publicly available filings, leadership commentary highlights efforts to optimize product-market fit by leveraging consumer trends emphasizing holistic health solutions and personalization. The strategic alignment towards omnichannel distribution aims to sustain customer engagement via subscription models combined with targeted social media outreach.

However, there is no explicit articulation of defensible moats such as proprietary formulations or exclusive distribution partnerships in filings ([S1], [F1]). Instead, FitLife appears reliant on brand equity cultivation supported by experienced management teams possessing domain expertise — notably CEO Dayton Judd who retains substantial equity stakes exceeding 58%, potentially aligning management incentives closely with shareholder value creation.

Competitive Positioning: Market Context and Industry Dynamics

FitLife operates within an intensely fragmented industry populated by both legacy players with entrenched shelf presence and agile digitally native brands capitalizing on e-commerce growth ([S1], analysis). The competitive set includes producers of nutritional supplements, fitness consumables, and wellness-focused personal care products where brand differentiation often hinges on innovation cycles coupled with marketing efficacy.

The company’s governance framework enforces oversight through independent directors exerting discipline across audit and compensation committees ([S20], [S21]). Notably absent are indications that regulation or supply chain constraints materially impair operational capacity or pricing power as per risk disclosures ([S4])— suggesting that competitive dynamics rather than external factors presently constrain margin expansion.

Nonetheless, the sector’s pricing environment is pressured by proliferation of lower-cost alternatives online alongside intensifying customer acquisition costs in digital channels — conditions that necessitate continuous innovation to maintain share.

Growth Drivers: Expansion Opportunities and Demand Catalysts

FitLife’s growth agenda encompasses penetrating broader consumer demographics via enhanced digital commerce capabilities alongside product portfolio innovation ([S3], [S1]). Recent board appointments reinforce emphasis on scaling capabilities: director Shannon Pappas brings extensive experience in consumer digital commerce transformations within health-related businesses ([S26]).

Targeted investments towards direct-to-consumer infrastructures seek to leverage personalized marketing tactics intended to increase customer retention rates—a critical factor for sustainable revenue increases given subscription-based model prevalence among competitors.

Moreover, sustained free cash flow generation provides financial flexibility to support selective capital expenditures focused on technology upgrades rather than heavy asset buildouts ([F1]). This aligns with sector trends favoring asset-light models incentivizing agility amidst rapidly evolving consumer preferences.

Constraints and Risks: Profitability Headwinds and Market Perceptions

Key risks revolve around the declining trajectory in operating metrics despite stable revenue bases: net income dipped nearly 30% year-over-year even as revenues grew moderately (~11%) indicating rising costs or margin pressure ([F1]). This divergence has attracted mixed analyst sentiment typified by bearish media narratives highlighting challenges scaling profitably in crowded wellness markets ([N3]).

Furthermore, limited transparency around granular business operations complicates investor confidence; public disclosures lack detailed segment breakdowns limiting clear visibility into drivers behind margin compression ([S2], [S4]). Market skepticism may also reflect concerns regarding capital structure flexibility given recent liquidity-focused communications amid conservative spending ([S5], [S9]).

Operational risks include dependency on digital channel effectiveness amid heightened competition for advertising real estate alongside emerging regulatory scrutiny typical for supplement-related claims—a standard sector challenge though not explicitly flagged as acute here.

Next Steps to Monitor: Guidance, Execution Milestones, and Market Signals

Investors should closely observe forthcoming quarterly reports expected post-April formulation updates for FY2026 guidance clarity ([S3]). Milestones worth tracking comprise sequential profitability trends balancing top-line growth against expense control efforts articulated during the earnings call.

Additional signals include any alterations in capital allocation strategies such as share repurchases or dividend initiation that might indicate confidence levels regarding cash flow sustainability ([S10]–[S15]). Operational execution pertaining to expansion of digital commerce infrastructure alongside measurable improvements in customer acquisition economics will further validate growth investment returns.

Closer attention is warranted towards disclosures illuminating competitive responses to market pricing pressures alongside any regulatory developments affecting product labeling or marketing practices within the wellness sector broadly.

Financial Snapshot: Performance Metrics and Balance Sheet Health

The table below summarizes key financial metrics juxtaposing FY2024 versus FY2025 results based on SEC XBRL data ([F1]):

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 6 | 7 | 10 | 42000 | -29.6% |

| 2024 | 9 | 10 | 13 | 10000 | +69.6% |

| 2023 | 5 | 4 | 8 | 106000 | +19.6% |

| 2022 | 4 | 4 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 7 | 14.5 | |

| 2024 | 10 | 24.9 | |

| 2023 | 0 | 4 | 19.6 |

| 2022 | 779000 | 20.7 |

Source: SEC companyfacts cache [F1].

Noteworthy observations:

- Revenue grew moderately validating some top-line resilience.

- Operating income declined substantially signaling margin contraction perhaps due to escalated marketing or administrative costs.

- Net income followed a similar declining pattern yet remained profitable affirming underlying business viability.

- Operating cash flow retained strength (~$7.4M), supporting ongoing liquidity alongside minimal capital expenditures reflecting an asset-light footprint.

- The current ratio above one indicates prudent working capital management conducive to near-term obligations coverage.

- Shareholders’ equity rose significantly suggesting retained earnings accumulation or issuance dynamics enhancing balance sheet robustness.

In sum, FitLife Brands demonstrates ongoing profit generation capability tempered by evident pressures constraining margin sustainability amid competitive wellness markets alongside marketplace skepticism requiring close monitoring of strategic execution outcomes.

This analysis is based exclusively on information extracted from SEC filings referenced herein and publicly available sources up to April 21, 2026; it does not constitute investment advice but aims to provide an informed perspective on FitLife Brands’ operational standing relative to disclosed evidence.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments