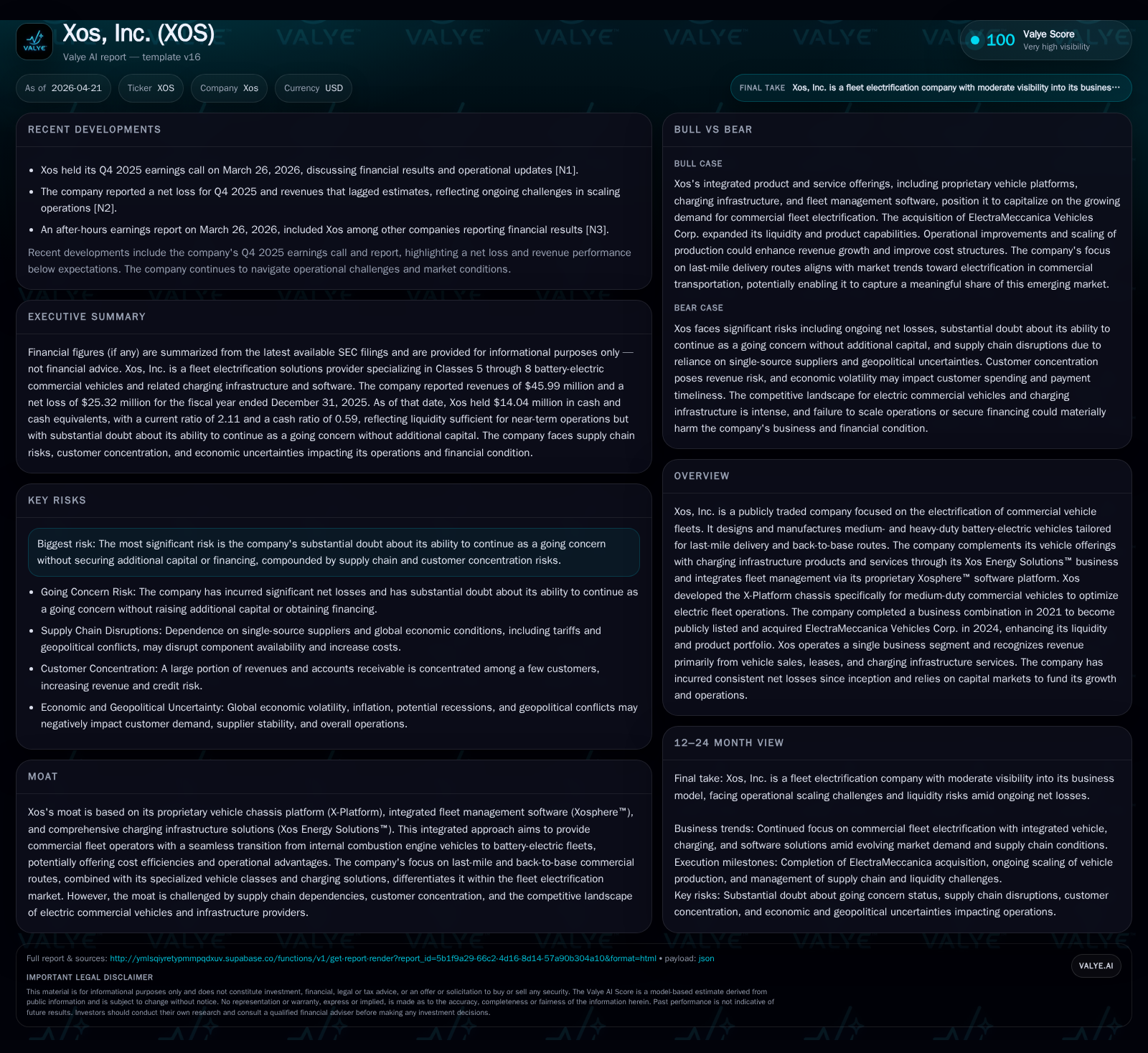

Xos, Inc. Advances Fleet Electrification Amid Liquidity Challenges

Xos’s latest filing reveals ongoing liquidity pressures despite strategic platform integration and an expanded product portfolio in commercial fleet electrification.

In its most recent 10-Q and subsequent filings, Xos, Inc. highlights persistent doubts about near-term liquidity despite restructuring of convertible notes and leveraging the acquisition of ElectraMeccanica to enhance its EV product line. The company’s business model centers on a proprietary chassis platform, integrated fleet software, and charging infrastructure tailored for last-mile and back-to-base commercial routes. The commercial EV industry presents both regulatory tailwinds and operational headwinds, including supply chain vulnerabilities and customer concentration risk. While Xos’s integrated approach offers potential differentiation, capital constraints remain a significant hurdle for scaling operations. Near-term milestones will focus on capital raising efforts, execution on vehicle deployments, and expansion of infrastructure services.

Latest Operating Developments and Significance

Xos’s latest quarterly filing dated November 13, 2025 [S2] delivers a sobering update on its financial condition during operational scaling challenges. Management explicitly reiterates a "substantial doubt" regarding the company’s ability to maintain sufficient liquidity over the subsequent twelve months without securing additional capital or refinancing. A critical near-term development involves the August 2025 conversion of accrued interest (~$6 million) on its $20 million convertible promissory note into approximately 1.8 million shares of common stock [S1,S16]. This conversion reduces immediate interest expenses but defers principal repayments spread over ten quarterly installments through early 2028 with ascending payments ranging from $1.5 million to $3 million per quarter [S16].

The company’s cash balance stood at about $14 million at year-end 2025 [F1,S7], supported by liquidity access from its March 2024 acquisition of ElectraMeccanica Vehicles Corp., which brought approximately $50 million in cash at closing [S10,S14]. However, this buffer appears insufficient to fully alleviate funding concerns as Xos faces ongoing operating losses alongside commitments to scale production capacity.

Complementing these filings is an 8-K event notice dated March 26, 2026 [S3] wherein Xos updated the market on year-end results and reiterated the pressing need for additional financing options while pursuing operational stability. The tone across these disclosures strongly emphasizes cautious optimism but underscores execution risks tied to financial endurance.

These operating updates establish a backdrop where liquidity limitations directly constrain growth initiatives even as technological progress continues.

Xos Business Model and Product Integration

Xos operates within a single reportable segment focused on electric commercial vehicles designed specifically for Classes 5 through 8 — targeting medium- and heavy-duty usage scenarios typical of last-mile delivery and back-to-base logistics routes [S1,S11]. The company’s revenue stems primarily from vehicle sales (including direct leases) supplemented by ancillary products such as charging infrastructure sold via its Xos Energy Solutions™ division.

Central to Xos’s strategic proposition is the proprietary X-Platform chassis platform engineered for rugged urban delivery cycles with range capabilities up to approximately 200 miles per day [S1]. This foundation enables modular integration with battery systems and powertrains optimized for operational efficiency in commercial fleets.

Complementing hardware offerings is the Xosphere™ software platform that manages vehicle telemetry, diagnostics, route planning, and energy management [S1]. This telematics component seeks to reduce total cost of ownership by delivering data-driven insights enabling fleet operators to optimize charging schedules aligned with available infrastructure.

The company's acquisition of ElectraMeccanica in early 2024 strengthened its product portfolio by adding complementary EV designs and bolstered liquidity reserves [S14], thereby supporting broader market coverage beyond solely step vans and stripped chassis vehicles.

Despite the integrative appeal combining chassis engineering, telematics software, and scalable charging solutions—which collectively form an ecosystem moat—Xos contends with supply chain dependency risks. Several critical components come from single-source suppliers accounting for sizable portions of accounts payable (e.g., two vendors made up ~23% as of year-end 2025) [S4]. This concentration potentially impairs flexibility to ramp output rapidly or negotiate cost terms amid volatile material markets.

Industry Environment and Competitive Dynamics

The broader commercial electric vehicle (EV) sector is characterized by rapid growth prospects propelled by increasingly stringent environmental regulations incentivizing fleet electrification globally . However, deployment faces acute supply chain disruptions affecting battery components, power electronics, harnesses, and structural materials—many impacted by tariff fluctuations that introduce cost volatility [S26,S12].

Xos’s niche focus on last-mile delivery limits total addressable market size compared with full truckload or long-haul freight segments but provides specialization advantages by tailoring EV designs optimized for high-density urban environments where range requirements are moderate yet reliability demands are elevated . Such specialization aligns with demand drivers emphasizing operational savings via zero-emission vehicles mandated under public policy regimes.

Competitive pressures stem from incumbents like Ford Pro Electric Trucks offering expanded medium-duty EV lines alongside dedicated EV startups that deliver vertically integrated platforms similar to Xos’s suite . Legacy OEMs generally benefit from established supply chains but often lack dedicated software ecosystems tailored narrowly to commercial fleet management as found in Xosphere™.

Margin compression poses a structural challenge due to component scarcity driving procurement costs higher while production volumes remain modest relative to automotive scale economics. Switching costs currently appear limited; many customers are experimental or pilot users given technology adoption phases, though integrated software/hardware bundles aim eventually to increase lock-in through incremental service offerings.

Significantly, customer concentration risk features heavily in credit exposure metrics: one customer accounted for approximately 54% of revenue during fiscal year 2025 while four customers collectively represented nearly half the accounts receivable balance at year-end [S19,S11].

Growth Catalysts and Obstacles

Tailwinds bolstering growth include accelerating mandates for decarbonization of commercial fleets particularly in urban centers seeking emission reductions under state-level Clean Fleet Rules or zero-emission vehicle (ZEV) mandates . These policies increasingly compel logistics providers to upgrade aging internal combustion engine fleets toward electric alternatives offering lower total cost of ownership over lifecycle.

Expansion of Xos Energy Solutions™ charging products constitutes another growth vector by addressing a notable bottleneck in widespread EV adoption: reliable fast-charging infrastructure compatible with diverse fleet schedules. Software upgrades enhancing predictive fleet energy management further support efficiency gains attractive to cost-sensitive customers.

However, execution is impeded by macro-financial constraints including continuing net losses that limit reinvestment capacity [F1], reliance on external funding sources amid volatile credit markets described in risk disclosures [S12,S26], plus persistent supply chain uncertainties complicating timely vehicle deliveries.

Elevated warranty liability provisions rising year-over-year signal potential residual quality or reliability challenges impacting post-sale operating expenses [S13]. Delays or underperformance relative to product specification targets could undermine customer confidence during critical early adoption phases.

Additionally, rising competition paired with tariff-induced component cost inflation erode pricing flexibility necessary for margin improvements in nascent production scales.

Key Near-Term Milestones and Monitoring Points

Investor focus should monitor upcoming quarterly guidance updates that may shed light on capital raise initiatives or refinancing terms addressing imminent debt maturities within the next two years given convertible note amortization schedules outlined [S3,S16].

Tracking volume ramp rates concerning vehicle production shipments alongside ElectraMeccanica product integration timelines will be instrumental in assessing whether incremental scale mitigates unit costs effectively.

Developments related to roll-out or expansion of charging hubs under the Xos Energy Solutions™ brand represent growth milestones with cross-selling potential into existing vehicle customer bases enhancing ecosystem stickiness.

Diversification efforts reducing revenue dependency on a handful of large customers should also be closely observed via updated periodic disclosures highlighting new contracts or partnerships mitigating concentration risks underscored at fiscal year-end [S19,S11,N1,N2].

Lastly, management commentary tone in earnings calls remains an essential sentiment barometer reflecting confidence or caution concerning operational forecasts given the delicate balance between funding challenges and the underlying market opportunity [N1,N2].

Financial Overview: Liquidity, Profitability, and Cash Flow

Xos’s most recent annual figures ending December 31, 2025 depict revenues declining roughly 18% year-over-year to approximately $46 million while operating loss narrowed about 28% but remained significant at -$33 million; net loss improved similarly though still considerable at -$25 million [F1]. These trends suggest measured progress controlling expense run rates amid softer top-line results.

Operating cash flow swung positive reaching $5.4 million versus negative nearly $49 million a year prior signaling meaningful working capital improvements possibly including better receivables collection or inventory management [F1]. Capital expenditures were minimal at zero dollars in full year ’25 reflective of tight cost controls following earlier investments [F1,S6,S29].

Balance sheet liquidity at year-end comprises cash & equivalents near $14 million with current assets exceeding current liabilities yielding a current ratio above 2x—an indication of short-term solvency though not fully alleviating going concern warnings documented extensively throughout filings [F1,S7,S12,S19].

Equity stands diminished around $23 million representing significant erosion from accumulated losses producing negative return on equity approaching -109%, reinforcing concerns over sustainable profitability absent structural turnaround actions [F1].

Convertible note restructurings provide temporary respite but require successful execution on fundraising plans long term crucially dependent on capital markets receptivity amidst economic uncertainty factors outlined including geopolitical tensions impacting supply chains highlighted throughout notes sections [S16,S26,S28].

| FY | Revenue ($M) | OpInc ($M) | NetIncome ($M) |

|---|---|---|---|

| 2023 | 44.5 | -65.0 | -75.8 |

| 2024 | 55.9 | -45.9 | -50.2 |

| 2025 | 46.0 | -33.1 | -25.3 |

| FY | CFO ($M) | Capex ($M) |

|---|---|---|

| 2023 | -39.3 | 1.4 |

| 2024 | -48.8 | 0.3 |

| 2025 | 5.4 | 0 |

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 46 | -25 | 5 | -33 | -17.8% | +49.5% |

| 2024 | 56 | -50 | -49 | -46 | +25.7% | +33.9% |

| 2023 | 45 | -76 | -39 | -65 | +22.4% | -3.4% |

| 2022 | 36 | -73 | -128 | -111 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 5 | -108.7 |

| 2024 | -49 | -149.2 |

| 2023 | -41 | -167.8 |

| 2022 | -142 | -65.4 |

Source: SEC companyfacts cache [F1].

In summary, while corrective financial trends appear plausible through working capital management gains offsetting continued investment de-escalation, material reliance on external capital injections remains unavoidable given recurring losses and industry investment intensity inherent in scaling complex electric vehicle manufacturing.

This analysis aims solely to detail operating developments, business positioning, industry context, growth dynamics, key monitoring points, and summarized financial health based strictly upon reviewed SEC filings and corroborating reports as of April 21, 2026.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments