Lakeland Industries Solidifies Government Contracts While Struggling with Profitability

The latest quarterly disclosures underscore Lakeland’s revenue momentum from government contracts against persistent operational and cash flow deficits.

Lakeland Industries reported a 15% year-over-year revenue increase in its latest quarter driven by new contracts with UK fire and rescue services, reflecting growing government demand for certified protective equipment. Despite this topline expansion, the company continues to face significant challenges with profitability, posting widening net losses and negative operating cash flow. The firm’s strategic positioning benefits from NFPA safety certifications and government relationships that create competitive moats, but cost pressures and revenue volatility weigh on margin recovery. Investor focus will remain on execution against contract backlog, cost control initiatives, and sustaining liquidity amid ongoing financial strain.

Quarterly Results Spotlight: Topline Growth Amid Profit Headwinds

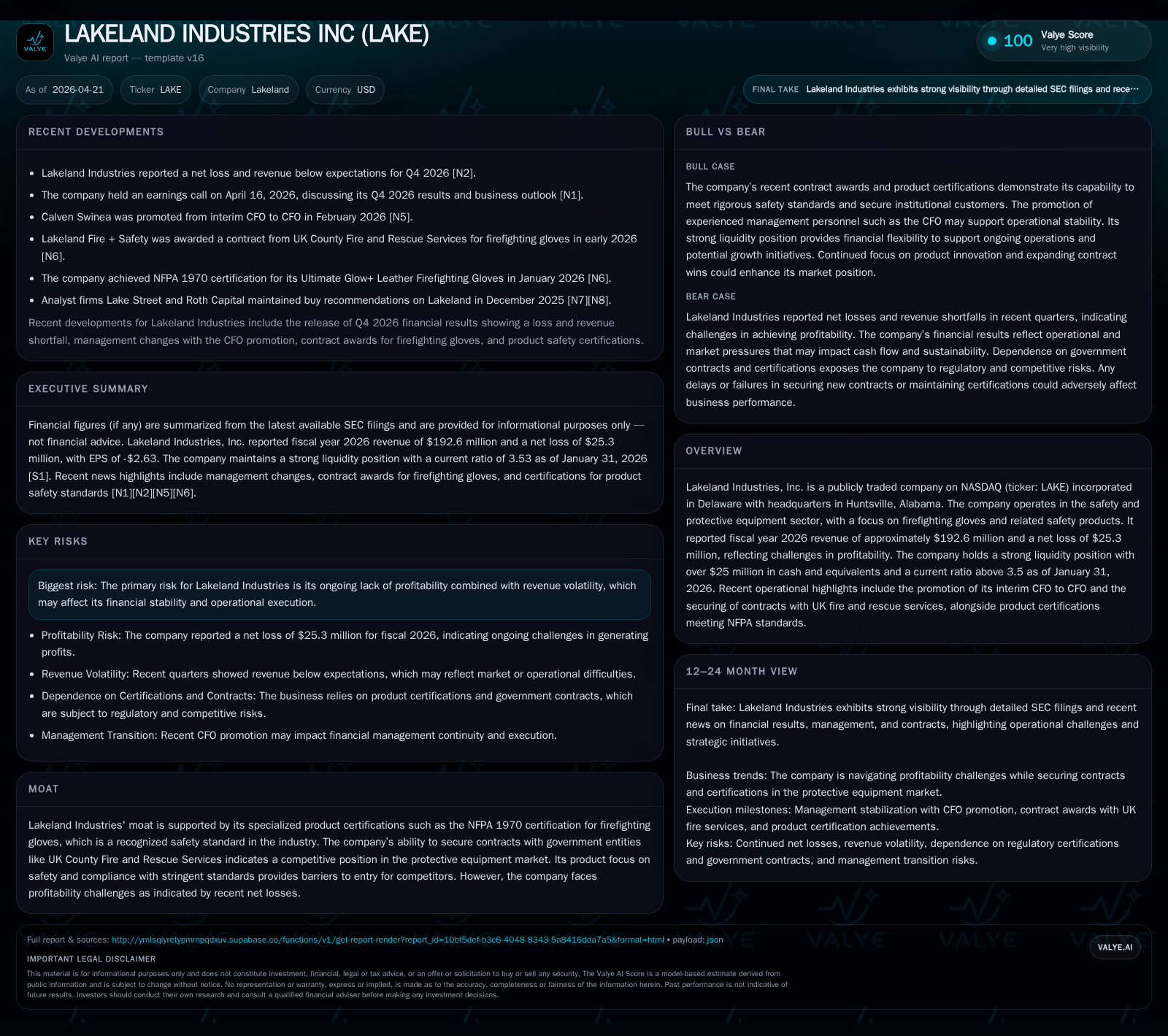

Lakeland Industries’ latest 10-Q filing dated December 9, 2025 [S2] reveals a notable uptick in revenue growth — exceeding 15% year-over-year — largely stemming from newly secured contracts with UK fire and rescue services announced earlier this year [S3]. This top-line traction underscores the company's ability to expand its footprint within the government contracting segment for essential safety products.

However, this revenue momentum has not translated into profitability gains. Operating income deteriorated further to an operating loss of $15.5 million in FY2026, compared with a $9.3 million loss in the prior year [F1]. Net losses deepened correspondingly to $25.3 million [F1], indicating that expense growth outpaced sales gains. Moreover, operating cash flow remained negative at approximately -$15.75 million for the full fiscal year [F1], signaling continued cash burn despite liquidity buffers. These results inject caution into investor sentiment as Lakeland balances growth initiatives against ongoing financial headwinds.

Business Model Examination: Specialized Protective Gear with Certified Safety Standards

Lakeland operates primarily in a specialized niche of the safety and protective equipment sector, focusing on manufacturing comprehensive firefighting gloves and related personal protective gear. Central to its business model is strict adherence to industry-standard certifications such as NFPA 1970 — the National Fire Protection Association's benchmark for firefighter protective clothing — which serves as a critical gatekeeper for market access [S1].

This regulatory compliance not only fulfills safety requirements imposed by public sector agencies but also differentiates Lakeland’s offerings amid a fragmented competitive landscape where many vendors operate without such certifications. Consequently, customers reliant on certified gear exhibit high switching costs due to stringent regulatory oversight and product validation protocols.

The firm’s revenue accrual relies on government procurement cycles where contract tenders are rigorous but once won tend to generate recurring revenues due to mandated replacement schedules and compliance upkeep [S1]. This model predicates steadier customer retention but introduces exposure to procurement timing risks.

Market Position: Competitive Moats Fueled by Government Contracts and NFPA Certification

The company's moat is anchored in its product certification pedigree and established relationships with government entities. Lakeland's recent success securing contracts with UK County Fire & Rescue Services evidences an ability to compete effectively on quality and compliance dimensions internationally [S3]. Such contracts also reflect increasing global recognition of NFPA standards or equivalent safety benchmarks beyond U.S borders.

Given the criticality of protective gear in emergency response scenarios, buyers prioritize certified products that meet rigorous testing protocols. Lakeland's compliance establishes pricing power resistant to commoditization pressures seen elsewhere in PPE markets populated by lower-cost uncertified alternatives.

Nonetheless, while certifications protect market entry barriers, competition remains from firms focusing on adjacent product lines or offering bundled solutions across other protective equipment categories — necessitating continued innovation and contract competitiveness.

Headwinds to Margin Improvement: Cost Pressures and Profitability Risks

Despite growth in contractual wins and revenues, Lakeland confronts pronounced structural hurdles restraining earnings recovery. The Management Discussion section of the latest quarterly report details elevated costs linked to raw materials inflation, labor expenses associated with quality assurance processes required by certification standards, plus overheads from servicing global government accounts [S2].

Revenue volatility inherent in bid-driven public sector procurement introduces lumpy demand patterns complicating fixed cost absorption. These factors culminate in negative operating leverage whereby incremental revenues do not adequately cover expanding costs.

Moreover, reported risk factors cite potential disruptions from supply chain uncertainties that may further exacerbate input price escalation or delay fulfilment timelines impacting margins [S4]. Investors must weigh these persistent profitability drags against the backdrop of Lakeland's strategic product positioning.

Growth Outlook: Expansion in Public Sector Demand vs. Revenue Volatility

Structurally, demand for firefighting gloves and similar protective equipment tied to public safety budgets appears intact and underpinned by increasing regulatory emphasis on first responder safety worldwide [S1]. International expansion through entities like UK fire services signifies tangible growth avenues beyond domestic markets [S3].

However, cyclical elements intrinsic to government spending cycles create episodic peaks and troughs that induce revenue fluctuations. Additionally, procurement lead times combined with evolving certification requirements can delay order intake or require capital expenditures ahead of revenue recognition cycles.

While NFPA certification sustains competitive advantage facilitating contract eligibility, sustaining incremental market share hinges on continuous certification renewals and product innovation responding to evolving standards and end-user ergonomics.

Critical Investor Watchlists: Upcoming Milestones and Execution Traps

Investor attention should focus sharply on near-term operational milestones highlighted during the April 16 earnings call [N1], including:

- Renewal or expansion of existing government contracts internationally,

- Progress on internal cost management programs aimed at reversing margin erosion,

- Timely recertification of products to maintain NFPA compliance,

- Potential updates or changes in procurement regulations affecting contract bidding dynamics,

- Monitoring management’s commentary on achieving sustainable profitability targets given past losses [N2].

Execution risks remain non-trivial as conversion of new contracts into stable cash flows coupled with disciplined spending control will dictate whether recent topline wins yield durable financial improvements.

Financial Summary: Liquidity Strength Versus Negative Earnings and Cash Flow

The fiscal year ending January 31, 2026 paints a mixed financial profile for Lakeland (see table below). The company retains a strong liquidity position — demonstrated by a current ratio above 3.5x supported by $25.2 million in cash equivalents — which provides operational runway amid losses [F1][S14].

Nonetheless, profitability metrics remain challenged with an operating loss widening by approximately 67% YoY to $15.5 million alongside a net loss magnitude expansion creating negative return on equity near -20% annualized [F1]. Operating cash flow stayed deeply negative at -$15.7 million leading to estimated free cash flow deficit around -$16.4 million after modest capital expenditures.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2026 | 193 | -25 | -16 | -16 | +15.2% | -40.0% |

| 2025 | 167 | -18 | -16 | -9 | +34.1% | -433.2% |

| 2024 | 125 | 5 | 11 | 6 | +1879.2% | +189.6% |

| 2023 | 6 | 2 | -5 | 6 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2026 | 1152000 | -16 | -19.6 |

| 2025 | 887000 | -17 | -12.3 |

| 2024 | 9 | 4.4 | |

| 2023 | -7 | 1.6 |

Source: SEC companyfacts cache [F1].

This juxtaposition confirms that while capital structure and liquidity management have been prudent so far ([S5],[S14],[S18]), sustained operational losses necessitate cautious monitoring of future capital allocation options.

In conclusion, Lakeland Industries stands at an inflection point where validated product leadership through stringent certifications combined with expanded governmental contracts offer promising growth pathways against a backdrop of significant profitability challenges worsened by inherent cost structures and demand volatility. Execution discipline around cost containment and converting backlog into positive cash flow will shape whether the company can leverage its moat into sustainable financial performance.

This analysis is based solely on publicly available SEC filings through April 21, 2026 ([S1]-[S22]) and relevant press sources ([N1]-[N5]). It is intended for informational purposes without providing investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments