Energy Transfer LP’s 2025 Growth Balance Between Capex Surge and Regulatory Risks

Energy Transfer LP reported moderate revenue growth in 2025 supported by expansive infrastructure investments while navigating legal and environmental challenges.

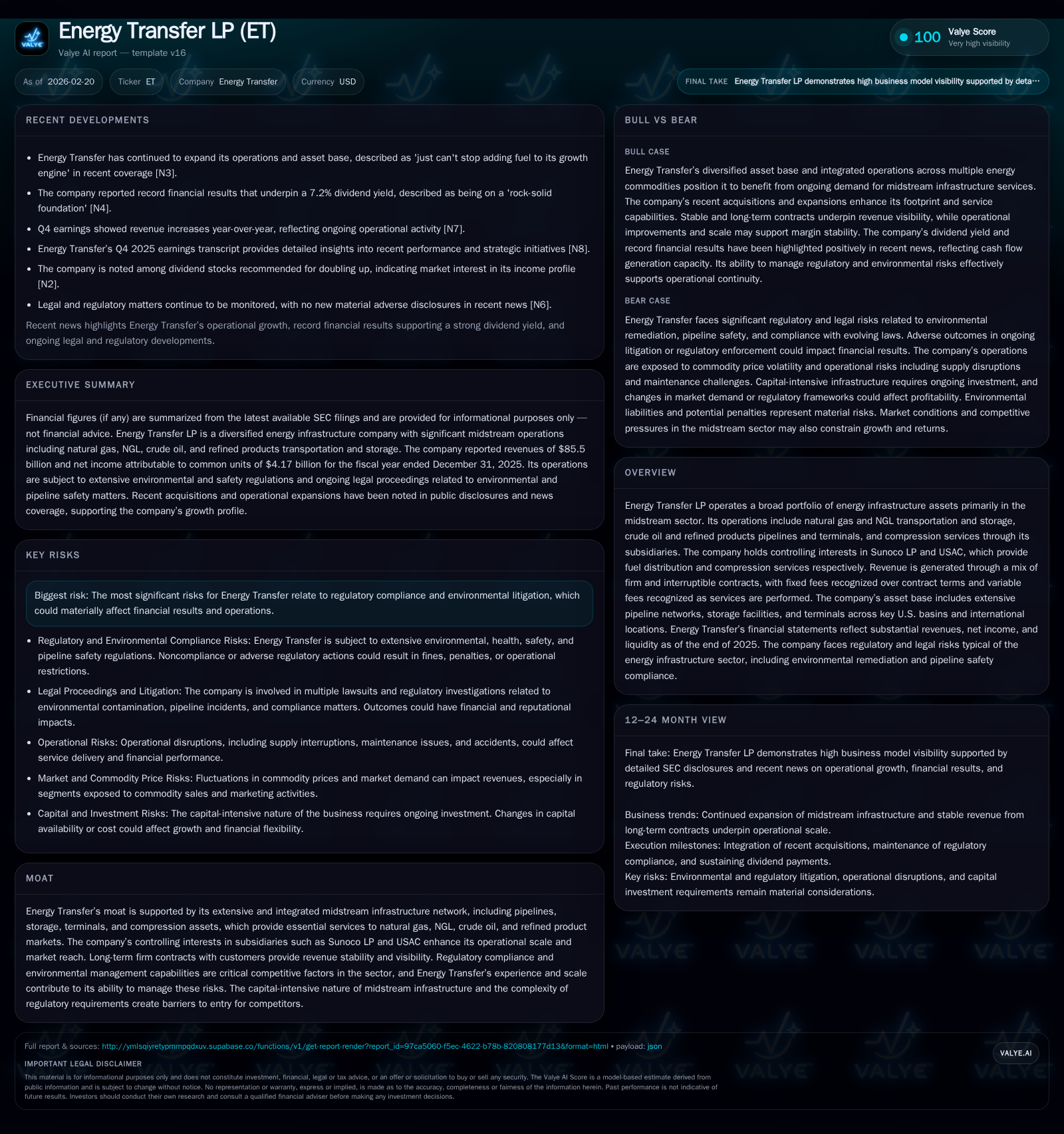

Energy Transfer LP’s 2025 financial performance saw revenues rise 3.5% year-over-year to $85.5 billion, driven by its diversified midstream infrastructure portfolio including controlling interests in Sunoco LP and USAC. However, net income declined 7.9%, reflecting higher operating costs and legal provisions amid environmental litigation risks. Capital expenditures surged over 50% to $6.3 billion as the company aggressively expanded pipeline, storage, and compression assets across prolific U.S. basins. Liquidity remains strong with a current ratio of 1.22 and well-managed debt covenants, but regulatory exposure and associated legal proceedings remain material factors to monitor going forward.

Overview

Energy Transfer LP operated in 2025 as a dominant energy infrastructure player primarily focused on the midstream sector encompassing natural gas, natural gas liquids (NGLs), crude oil, and refined products transportation and storage. The Partnership’s comprehensive assets include pipelines, terminals, storage facilities, and compression services distributed across key U.S. basins like the Permian, Anadarko, Williston, Haynesville, Marcellus, and Utica shales. Energy Transfer holds controlling stakes in subsidiaries Sunoco LP—which operates an extensive fuel distribution network—and USAC, which provides critical compression services for gas gathering and processing.

Historical Performance

From 2022 through 2025, Energy Transfer’s revenue trends reveal a rebound after a dip in 2023 linked to macroeconomic headwinds affecting commodity pricing and volumes:

Historical performance (annual)

| FY | Rev ($bn) | Net ($bn) | CFO ($bn) | OpInc ($bn) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 85.5 | 4.4 | 10.1 | 9.0 | +3.5% | -7.9% |

| 2024 | 82.7 | 4.8 | 11.5 | 9.1 | +5.2% | +22.3% |

| 2023 | 78.6 | 3.9 | 9.6 | 8.3 | -12.6% | -17.3% |

| 2022 | 89.9 | 4.8 | 9.1 | 7.7 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks | FCF ($bn) | ROE% |

|---|---|---|---|

| 2025 | 3.8 | 9.0 | |

| 2024 | 7.3 | 10.5 | |

| 2023 | 0 | 6.4 | 9.0 |

| 2022 | 0 | 5.7 | 11.7 |

Source: SEC companyfacts cache [F1].

Note: Operating cash flow (CFO) calculated as net cash provided by operating activities; Capex represents payments for acquisition of productive assets.

Revenue rose moderately by 3.5% in FY25 following a sharp contraction in FY23 related partly to supply/demand imbalances during global disruptions in energy markets, with operating income almost flat (-1.2%) due largely to inflationary costs in operations and administrative areas combined with less favorable contract dynamics.

Net income declined by nearly 8%, influenced by increased litigation expenses tied to environmental cases as well as impairments and higher interest expense from expanded debt issued in recent years.

Operating cash flow showed an 11.8% contraction reflecting tighter working capital management but still producing approximately $10 billion annually—a robust figure that underpinned significant capital spending initiatives that surged +51% year-over-year to $6.3 billion.

Business Model Drivers

Energy Transfer generates revenues predominantly through firm transportation/storage contracts for pipelines and storage facilities across multiple basins characterized by long durations and fixed fee structures providing consistent stand-ready services irrespective of fluctuations in throughput volumes from producers.

Interruptible contracts form a smaller portion of revenues but expose results to volume variability.

The controlling interests in Sunoco LP – with an integrated fuel distribution network spanning North America, Europe, Caribbean sectors – provide diversification away from purely midstream operations toward downstream logistics ensuring diversified cash flows.

USAC strengthens the company's midstream segment through compression assets essential for gas collection and transportation.

Cost management is challenged by rising maintenance/operational expenses especially given rigorous regulatory safety compliance requirements imposed on pipeline systems including integrity management programs targeting high consequence areas.

Growth Prospects & Constraints

Growth Catalysts

- Continued build-out of high-demand natural gas gathering and processing capacity in prolific shale plays like Permian Basin supporting growing gas production.

- Expansion of terminals, fractionation facilities, and pipeline lateral fill-ins enabling capture of NGL market growth driven by petrochemical demand.

- Strategic acquisitions such as the Crestwood deal broaden footprint notably in the Williston Basin giving scale advantages.

- Inflation adjustments embedded within many firm contracts offering partial revenue protection.

- Renewable natural gas (RNG) integration potential leveraging existing pipeline infrastructure could emerge as complementary growth area given industry energy transition trends.[S19]

Constraints & Risks

- Ongoing environmental lawsuits (e.g., MTBE groundwater contamination cases brought by states like Maryland and Pennsylvania) pose financial penalties risk and reputational issues.[S9],[S20]

- Climate change litigation alleging deceptive marketing practices extend potential adverse verdicts.[S9]

- Regulatory risks including FERC enforcement investigations (e.g., allegations over historical non-compliance involving Rover pipeline operations).[S9]

- Market volatility affecting interruptible volumes can compress margins temporarily though mitigated by predominance of firm contracts.[N2],[N14]

- Dependence on commodity price-linked margin spread impacts downstream refining operations owned via Sunoco LP's Burnaby Refinery complex with supply chain vulnerabilities.[S2]

Financial Position & Capital Allocation

Energy Transfer maintains a significant debt load exceeding $68 billion held under various senior notes maturing through the mid-2050s and credit facilities including revolving lines at subsidiary levels (Sunoco LP’s $2.5 billion facility unused at year-end). The company’s leverage ratio stood at a moderate 3.21x consolidated EBITDA at fiscal year-end demonstrating compliance with restrictive covenants limiting liens, asset sales, affiliate transactions, or dividend payments during defaults.[S4],[S23]

Recent debt activity includes issuance of multiple senior notes totaling approximately $4 billion during early-to-late 2025 aimed at refinancing near-term maturities while redeeming roughly $3 billion principal amount of older notes—these moves have extended maturity profiles while optimizing coupon structures.[S18]

Liquidity is supported by over $1.27 billion cash plus substantial unutilized revolvers offering flexibility for capital spending or opportunistic acquisitions as evidenced by active deployment into pipeline expansions with capex accelerating sharply.[F1]

ROE hovers around approximately 9%, based on latest net income versus equity base nearing $49 billion reflecting stable profitability despite transient earnings pressures.[F1]

Free cash flow (CFO minus capex) remains positive (~$3.85 billion), sufficient to cover distributions although dividend payout data is not explicitly available from tagging but recent commentary points to a sustained above-7% yield reflecting the confidence from record earnings stabilization.[N1],[N7]

No recent share repurchases were noted since FY21 bolstering focus on reinvestment into core growth assets rather than capital returns via buybacks.[F1]

Operational Highlights & Segment Nuances

- Intrastate & interstate natural gas pipelines represent significant revenue drivers supported by multi-year firm contracts aggregating reservation fees plus variable incremental charges tied to throughput volumes.[S19]

- Midstream segment focuses heavily on gathering/processing/compression activities anchored in basins such as Permian and Haynesville benefiting from contiguous infrastructure ownership enabling operational efficiencies.[S26]

- Crude oil logistics & refined product transportation via pipeline networks combined with terminals services add incremental stability given commodity mix diversification.[S19]

- Sunoco LP’s retail fuel distribution system—with over thousands of sites branded under Sunoco—is a major contributor providing volume diversity outside pureplay midstream exposure.[S19]

- USAC’s compression service portfolio offers specialized services essential for boosting gas throughput integrity compliance aligning with increasing regulatory focus on methane emissions reductions.[S19],[S24]

Legal Proceedings & Regulatory Environment Risks

Energy Transfer faces several notable environmental litigations including arrayed MTBE groundwater contamination claims filed by multiple states seeking damages potentially materializing beyond accruals currently reserved though judged unlikely to imperil consolidated balance sheet materially.[S9],[S20],[S25]

Sunoco's ownership of refinery operations introduces operational risk factors including crude supply interruptions primarily tied to dependencies on pipelines such as Trans Mountain Pipeline impacting Burnaby Refinery continuous operation amid local community opposition or regulatory stringency.[S2]

FERC investigations into historic conduct during construction phases of notable pipelines like Rover add legal uncertainties with potential penalties though no current quantifications available.[S9]

Newer climate change related lawsuits target alleged deceptive marketing practices across multiple jurisdictions presenting evolving liabilities beyond traditional environmental exposures requiring vigilant risk management strategies moving ahead.[S9],[S20]

High consequence area rules under pipeline integrity management programs require continuous inspection via inline tools or pressure testing constraining OPEX but assuring system safety standard adherence--a notable cost driver unique to this sector’s compliance landscape.

What To Watch Going Forward (Analysis)

- Close monitoring of environmental litigation outcomes will be critical given potential implications for contingent liabilities or settlement reputational impacts affecting cost of capital.

- Contract renewals particularly interruptible segments activity where volume elasticity may lead to margin erosion if production slows or shifts geographically.

- Capex execution efficiency amid rapidly escalating investment program targeting system expansion balanced against return profile sustainability.

- Refining margin environment connected indirectly through Sunoco LP’s asset exposure—commodity price volatility remains a key sensitivity factor impacting earnings contribution.

- Debt maturity schedules aligned with ongoing refinancing efforts maintaining covenant compliance essential to preserve liquidity buffers.

- Potential further consolidation/acquisition targets leveraging Energy Transfer’s large-scale platform offering synergies especially around low-cost basin access or complementary downstream capabilities.

Conclusion

Energy Transfer LP remains a heavyweight midstream energy infrastructure operator demonstrating resilient revenue growth driven by diversified assets spanning natural gas transmission/storage, crude/refined products logistics, and retail fuel distribution through subsidiaries like Sunoco LP and USAC compression service provider.

Despite challenges posed by regulatory compliance costs alongside ongoing environmental lawsuits leading to modest margin compression impacting net income growth trajectory, the Partnership has buttressed its growth profile through aggressive capital investments with capex surging over half since prior year supported by stable liquidity position underscored by institutional-grade credit covenant adherence.

Its long-dated debt maturities paired with controlled leverage ratios provide financial flexibility conducive for funding expansive project pipelines targeting burgeoning U.S shale basin volumes fundamentals whilst navigating complex regulatory headwinds endemic to midstream operators today.

Investors interested should keep abreast of legal developments alongside operational execution efficacy given these remain critical inflection points influencing future profitability persistence across an energy transition shaped macro backdrop.

This analysis is based solely on publicly available information as of February 20, 2026, including SEC filings , latest quarterly releases , XBRL data [F1], and related industry context; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments