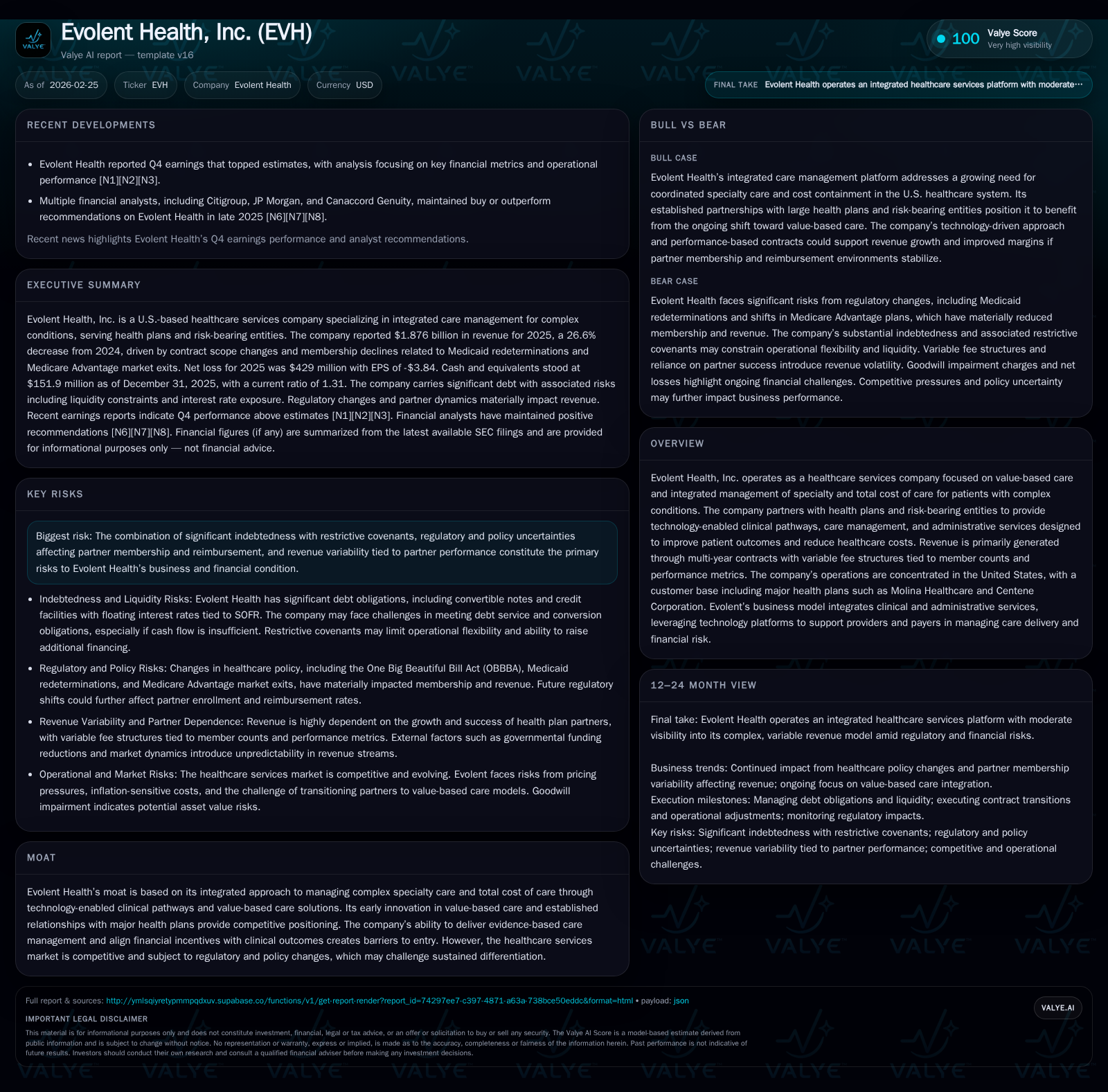

Evolent Health’s Debt Refinancing and Portfolio Shift Reinforce Cost Management Focus

Evolent Health demonstrates robust revenue growth amid heavy debt servicing and strategic divestitures in its value-based care business.

Evolent Health, a pioneer in technology-enabled value-based healthcare services, has delivered strong top-line expansion over recent years, driven by multi-year contracts with major health plans focused on specialty care management. However, earnings remain under pressure from escalating operating losses, largely attributable to impairments and increased interest expenses. The company has undertaken significant refinancing actions to extend debt maturities and manage liquidity, alongside portfolio reshaping through divestitures like Evolent Care Partners. Looking forward, maintaining revenue momentum depends on expanding partnerships and navigating regulatory uncertainties, while controlling capital allocation amidst heavy leverage remains critical.

Company Overview and Historical Performance

Founded in 2011 as an early innovator in value-based care (VBC), Evolent Health carved a niche supporting health plans and risk-bearing entities in managing specialty care for complex patient populations including cancer and cardiovascular diseases. Leveraging technology-enabled clinical pathways integrated with administrative services, Evolent aims to enhance evidence-based patient outcomes while curbing cost inflation.

Between 2021 and 2023, Evolent’s revenue escalated markedly from $248 million to $556 million (a ~45% compound annual growth rate), reflecting successful contract expansions with major partners such as Molina Healthcare and Centene Corporation. These contracts typically feature variable fee structures tied to member counts and performance metrics within multi-year agreements that stabilize recurring revenue streams [F1][S1].

However, profitability trends reveal intensifying operating losses: the company swung from an operating profit of ~$3.6 million in 2022 to a steep operating loss of $410 million by fiscal year-end 2025. This was predominantly driven by a non-cash goodwill impairment of nearly $398 million reflecting market capitalization declines relative to carrying asset values, alongside rising interest expenses on substantial indebtedness accrued from financing activities [F1][S25]. Net losses followed suit with a record negative $429 million in 2025.

Simultaneously, operating cash flow improved to nearly $39 million in 2025 compared to just under $19 million the prior year—highlighting positive underlying cash generation capabilities despite bottom-line pressures. Capital expenditures remained relatively moderate versus cash flow at around $35 million annually (data available up to 2019), aligning with the company’s asset-light software-enabled service model [F1].

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | -429 | 39 | -410 | -1782.0% | ||

| 2024 | -23 | 19 | -40 | +31.8% | ||

| 2023 | 556 | -33 | 143 | -71 | +45.4% | -74.3% |

| 2022 | 382 | -19 | -12 | 4 | +54.0% |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks, FCF. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | -103.4 |

| 2024 | -2.3 |

| 2023 | -3.1 |

| 2022 | -2.2 |

Source: SEC companyfacts cache [F1].

Note: Capex data limited; Buybacks noted only for latest year

Strategic Moves & Portfolio Changes

In late 2025, Evolent divested its total cost of care management arm, Evolent Care Partners (ECP), for approximately $100 million (net proceeds around $91 million post working capital adjustments). This move crystallized a gain (~$15 million) but narrowed Evolent's operational footprint towards its core specialty care management services emphasizing integrated clinical pathways [S1].

Alongside portfolio pruning, Evolent executed notable refinancing transactions: it issued roughly $167 million aggregate principal amount of new notes maturing in 2031 to repurchase equivalent principal of rapidly maturing 2025 notes expiring imminently. Additionally, it drew upon delayed draw term loan facilities totaling $200 million during early 2025 for general corporate purposes, including working capital needs and debt repayments [S4][S6][S7].

Such actions extended debt maturities while managing cash flow demands but have also entailed significant interest expense increases — interest attributable across various instruments rose materially in recent periods.

Capital Structure & Liquidity Profile

As of December 31, 2025, Evolent's balance sheet carried:

- First Lien Term Loan Facility: ~$117 million outstanding [S9]

- Second Lien Term Loan Facility: ~$175 million originated from Series A Preferred Stock exchange [S9][S7]

- Revolving Credit Facility utilization: ~$72.5 million drawn versus total commitments nearing $125 million under various increments [S9][S7]

- Convertible Senior Notes aggregating ~$569 million principal due mostly by the end of this decade; structured at coupons ranging from ~3.5%–4.5%, tied to share conversion rights and fair value discounts [S20]

Cash and equivalents stood at approximately $152 million at year-end accompanied by restricted cash close to $29 million designated mainly for pharmacy claims collateralization and risk-sharing deposits — reflective of operational complexities inherent in healthcare financial arrangements [S12][F1].

Liquidity is guarded through covenants requiring minimum liquidity tests and leverage thresholds embedded within credit agreements; these covenants also impose constraints on dividends (none paid currently) and stock repurchases which did occur modestly (~$40 million in FY25). Because servicing large amounts of debt requires significant cash outlays (interest expense topped $57 million recently), the company balances deleveraging efforts against required reinvestments into platform enhancements and sales initiatives.

Future Growth Drivers & Constraints

Growth going forward hinges on leveraging its integrated technology offerings that combine clinical decision support with administrative efficiency improvements — particularly attractive given shifting payer-provider incentives favoring value-based care models over fee-for-service. The company’s moat rests on these differentiated clinical pathway tools coupled with established relationships within leading Medicaid-focused health plans.

However upward trajectory faces notable headwinds:

- Regulatory risks impacting Medicare Advantage enrollment trends or reimbursement policy changes among managed care entities could dampen partner membership levels and associated revenues.

- Revenue contraction risks exist if key contractual partners underperform against agreed metrics tied directly to variable fees.

- The burden of considerable indebtedness limits free cash flow availability for aggressive M&A or organic expansion without additional capital raises.

- Integration complexities surrounding new technologies or joint ventures could also temper near-term margin expansion potential.

Absent explicit forward guidance disclosed recently, monitoring key contract renewals, partnership expansions (e.g., Molina or Centene updates), regulatory environment shifts affecting Medicaid managed care will be critical indicators for momentum sustainability [N1][N2][N3].

Returns & Capital Allocation Considerations

Return on equity is severely negative (-103% approximate FY25) driven largely by net losses from impairments and financing costs overshadowing operating profitability attempts [F1]. The structural leverage amplifies both returns potential in upside scenarios but equally risks magnifying losses under adverse conditions.

Cash flow generation supports ongoing operational needs yet leaves limited discretionary capacity for shareholder distributions; accordingly no dividends are declared presently. Buybacks conducted appear opportunistic amid liquidity events such as refinancings rather than sustained programs.

Capital allocation currently prioritizes:

- Debt refinancing/refund efforts aimed at optimizing maturity profiles and cost savings.

- Selective divestitures like ECP enabling focus on higher-margin specialty management verticals.

- Continued investments into technology platforms underpinning care integration capabilities.

Balancing these priorities against potential alternative uses including acquisition opportunities or expanded R&D will require ongoing review especially should credit markets tighten or partner demand fluctuate.

Closing Thoughts & Outlook Signals

Evolent Health occupies a specialized niche addressing complex healthcare cost challenges using a blend of clinical expertise aided by digital infrastructure. The firm’s strong historical revenue rise signifies market acceptance though earnings remain volatile due primarily to capital structure dynamics plus impairment risks inherent in intangible assets valuation.

Successful navigation entails sustaining contracted client base growth while prudently managing leverage-induced financial constraints amidst evolving healthcare policies impacting managed care economics. Observers should watch upcoming partner contract renewals/expansions plus regulatory shifts impacting Medicare Advantage carefully as signals of growth potential or stress points.

This analysis reflects publicly available information up through February 25th, 2026 without providing investing advice or price forecasts.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments