First Choice Healthcare’s Shift to Nurse Practitioner-Led Clinics Sets the Stage for Growth

FCHS pivots from orthopedic services toward a national network of personalized wellness clinics emphasizing Nurse Practitioner-led care and compounding pharmacy integration.

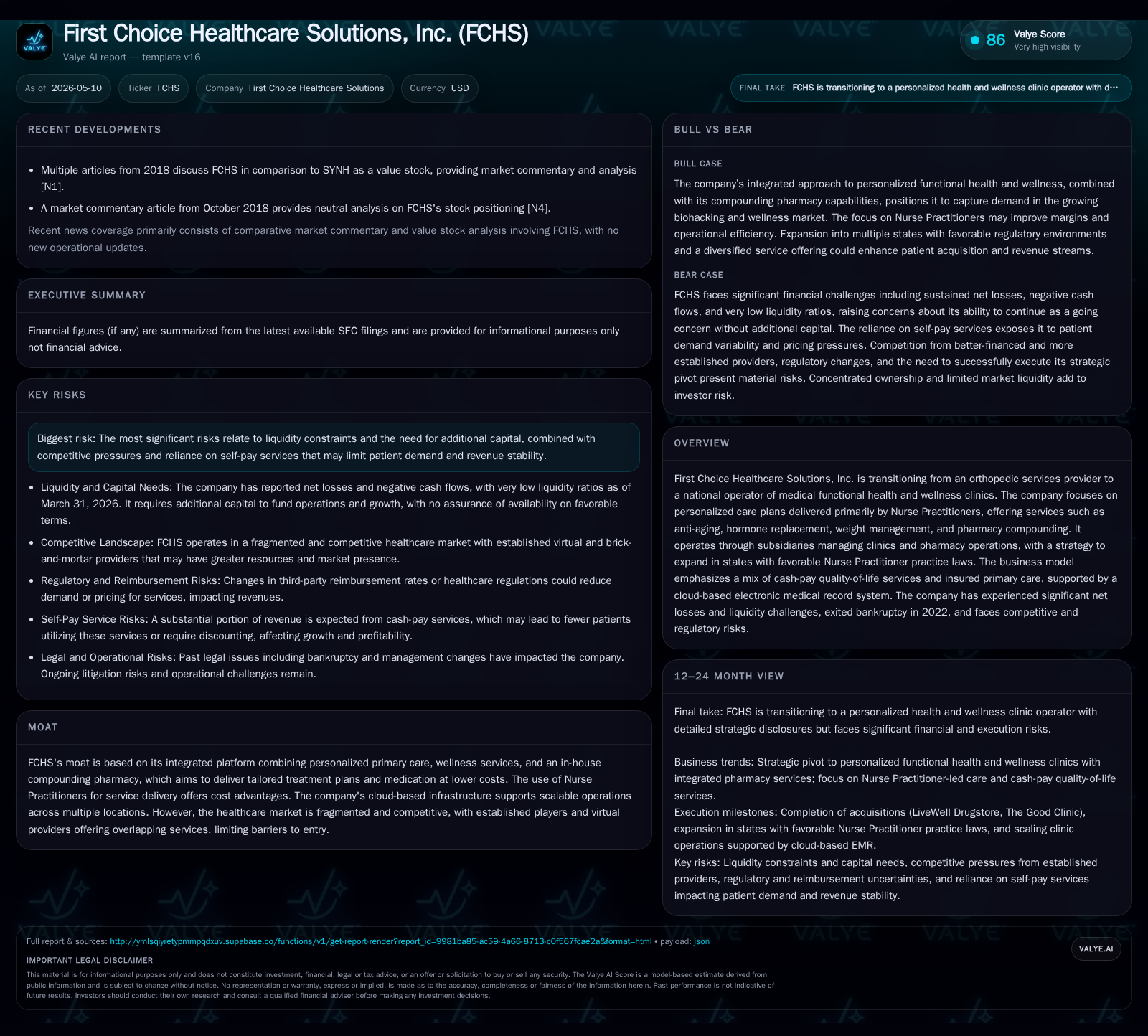

First Choice Healthcare Solutions, Inc. (FCHS) is executing a strategic transformation away from traditional orthopedic services toward operating a national medical functional health and wellness clinic network. The latest quarterly filing highlights ongoing divestiture of legacy lines and integration of acquisitions like Pointe Medical Services and The Good Clinic to scale Nurse Practitioner-driven personalized care and pharmacy offerings. Despite significant liquidity constraints and operating losses, FCHS’s business model focuses on scalable lower-cost provider staffing, a diversified cash-pay service mix, and cloud-based infrastructure benefits. However, this growth path faces market fragmentation, regulatory complexity, and substantial financial risk based on current balance sheet metrics.

Latest Operating Update Reflects Strategic Refocus

First Choice Healthcare Solutions’ Q1 2026 Form 10-Q filed May 8th reveals continued operational realignment away from its historically dominant orthopedic services toward building a national chain of medical functional health and wellness clinics. The company has effectively curtailed its legacy orthopedic treatment offerings, including physical therapy, pivoting resources to support Nurse Practitioner (NP)-led primary care and quality-of-life service lines [S2].

Highlights include ongoing integration efforts of recent acquisitions — notably Pointe Medical Services and The Good Clinic — which broaden the personalized primary care footprint and pharmacy operations under the company’s growing Live Well MD brand [S6]. These moves reflect an explicit strategy to build a scalable platform leveraging NPs as primary providers while embedding pharmacy compounding to deliver customized medication solutions.

However, the filing underscores pressing liquidity challenges with cash & equivalents measured at just $3,859 as of March 31, 2026 against $42.2 million of current liabilities — yielding an effectively zero current ratio [F1]. This working capital mismatch evidences substantial financial strain that could constrain further growth absent capital infusions.

Additionally, restructuring-related headcount reductions have been implemented previously to reduce operating expenses while redirecting focus on revenue growth in high-potential segments [S1].

Business Model Evolution: From Orthopedics to Wellness and Personalized Care

FCHS monetizes through a hybrid model combining direct-to-consumer cash-pay quality-of-life medical therapies alongside insured primary care visits largely delivered by Nurse Practitioners [S1][S22]. Cash-pay segments encompass services such as anti-aging treatments, hormone replacement therapy (HRT), metabolic weight management programs, and precision laboratory/gene testing to personalize care plans [S25].

The insurance-billable primary care offered via NPs serves both as a patient acquisition funnel and as a baseline stable revenue source supporting overall clinic economics. The cost advantage stems notably from employing NPs whose labor costs are materially lower compared to physicians but who can independently manage a broad scope of primary care services especially in states granting full-practice authority [S6].

Complementing this is an in-house compounding pharmacy operation producing sterile and non-sterile customized drug formulations including hormone optimizations tailored to individual biologies—a modular capability designed to enhance patient outcomes while improving margin profiles [S21].

Cloud-based electronic medical records (EMR) systems centralize data flows across multi-site operations facilitating standardized protocols which are critical for quality control in the compounding process and continuity in personalized medicine delivery [S1]. Collectively these elements position FCHS’s platform as integrated but still early-stage within a fragmented industry.

Competitive Positioning in a Fragmented Primary Care and Pharmacy Market

The company’s moat primarily derives from vertical integration across clinical care plus compounding pharmacy—allowing coordinated personalized treatment plans delivered cost-effectively through Nurse Practitioners [S1][S15]. This dual offering aims to differentiate FCHS from typical primary care chains that lack specialized pharmacy capabilities.

Nonetheless, the U.S. primary care market is deeply fragmented with numerous traditional physician practices alongside emerging virtual health providers offering overlapping wellness services. While the NP labor model promises lower unit costs (a sector-native insight), regulatory heterogeneity across states imposes operational complexity affecting geographic expansion pace and scale economics [S15][S18]. For example, only about half of the U.S. states grant full-practice authority to NPs thereby constraining where FCHS can deploy its core clinic model without physician oversight.

Furthermore, compounding pharmacies face stringent FDA and state-level regulations requiring meticulous compliance with Good Manufacturing Practices (GMP) especially for sterile admixtures which carries legal risk if standards lapse [S21]. This heightens barriers related not only to regulatory scrutiny but also capital intensity for scaled sterile production.

Market evaluations for Denver and Phoenix suggest intent to further extend nationwide presence.

Acquisitions such as Pointe Medical Services ($17.3 million deal signed July 2023) supplying internal medicine/wellness infrastructure along with The Good Clinic's established primary care concept offer immediate operational scale and help seed brand awareness initiatives [S6][S11].

A critical lever is scaling patient volume per clinic coupled with increased adoption of higher-margin self-pay treatments including compounded pharmaceuticals delivered by their proprietary pharmacy ecosystem. Marketing strategies employ digital channels plus employer outreach programs aiming to attract lifestyle-oriented clients seeking longevity interventions—a faster-growing segment within biohacking-related health trends identified at the industry level [S22].

Operational efficiencies are anticipated from standardized cloud-based EMRs enabling rapid onboarding of providers across clinics while maintaining compliance standards essential for compounding pharmacy operations.[F1] Margin improvement metrics will hinge on volume uplift in both clinic visits and prescription fill rates plus enhanced mix towards cash-pay therapies.

Risks and Constraints: Liquidity Pressure, Market Competition, and Regulatory Challenges

Liquidity remains the most pressing risk; Q1 2026 filings reveal severe working capital imbalances (current liabilities exceed current assets by magnitudes) with negligible cash reserves casting doubt on sustainability absent new funding events [F1][S2][S4]. Persistently negative operating income (~$2.67 million loss recorded in FY2025) coupled with accumulated deficit exceeding $74 million reflect significant historical losses tied partly to restructuring costs post-bankruptcy exit in 2022 [F1][S1].

Competitive dynamics intensify pressure as established hospital systems, health networks, telehealth platforms, along with emerging boutique wellness providers compete for similar patient cohorts. Margins could be pressured further should competitive factors force service discounting or increased marketing spend required to build brand recognition beyond initial acquisition footprints [S15].

Regulatory risks are multifaceted: compounding pharmacies carry inherent liability—both from product safety perspectives requiring strict adherence to USP <795>/<797> standards—and exposure to evolving federal/state anti-kickback statutes that complicate referral relationships [S21][S20]. Billing errors or documentation failures across multi-state operations could result in fines or exclusion from government payor programs impacting insured revenue lines [S15].

The company acknowledges that access to additional capital through equity or debt markets is imperative for growth execution; failure here risks forced curtailment of expansion plans or deeper cost-cutting that may impair competitive positioning [S7][S13]. Additionally, integrative execution risks exist related to assimilating acquired entities fully into uniform operating protocols.

Upcoming Milestones and Performance Indicators to Watch

Critical near-term milestones include completing acquisition integrations particularly around harmonizing clinical protocols between Pointe Medical Services and The Good Clinic subsidiaries into the Live Well MD umbrella [S2][S6]. Observing patient volume metrics per location will provide early insights into customer adoption velocity under the NP-delivered model.

Capital raises disclosed or announced post-quarter would be pivotal signals for growth runway extension. Regulatory approvals enhancing pharmacy compounding licenses or reimbursement policies could materially affect service mix economics.

Operational execution markers such as provider hiring rates consistent with planned geographic rollouts plus improvements in billing accuracy/compliance adherence are also key leading performance indicators [S1]. Monitoring shifts in revenue composition between self-pay versus insured segments will inform risk profile evolution given variability linked to consumer discretionary spending versus insurance reimbursement predictability.

Financial Snapshot: Operating Losses and Balance Sheet Status

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $3,859 | |

| 2026-03-31 | ||

| Current assets | $44,434 | |

| 2026-03-31 | ||

| Current liabilities | $42,234,469 | |

| 2026-03-31 | ||

| Current ratio | 0x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

| Metric | Value (USD) | Period Ended |

|---|---|---|

| Cash & Equivalents | 3,859 | |

| 2026-03-31 | ||

| Current Assets | 44,434 | |

| 2026-03-31 | ||

| Current Liabilities | 42,234,469 | |

| 2026-03-31 | ||

| Operating Income | -2,671,033 | |

| 2025-12-31 |

The stark imbalance between current assets ($44K) versus current liabilities ($42M) yields a near-zero current ratio demonstrating acute short-term liquidity risk absent immediate capital infusions [F1]. Operating losses remain substantial driven by ongoing restructurings plus acquisition-related amortizations or integration costs indicated in annual disclosure [$2.67 million negative operating income reported for fiscal year ended Dec 2025] [F1][S1].

No long-term debt is currently reported indicating leverage is concentrated primarily on working capital obligations or trade payables; however large accumulated deficits (> $74 million) weigh on equity cushions limiting financial flexibility [F1][S7]. These financial stress signals necessitate close monitoring of liquidity management effectiveness especially given expansive strategic ambitions.

This analysis synthesizes verified SEC disclosures up through the Q1 2026 filing alongside authoritative company documents without forward-looking investment opinions. Given FCHS’s transitional stage facing structural market opportunities paired with acute financial constraints this profile should serve as an informed business examination rather than directive advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments