Fifth District Bancorp’s Conservative Mortgage Focus Limits Growth Amid Stiff Local Competition

Established community bank leverages fixed-rate residential lending with cautious expansion into commercial loans while managing modest capital returns.

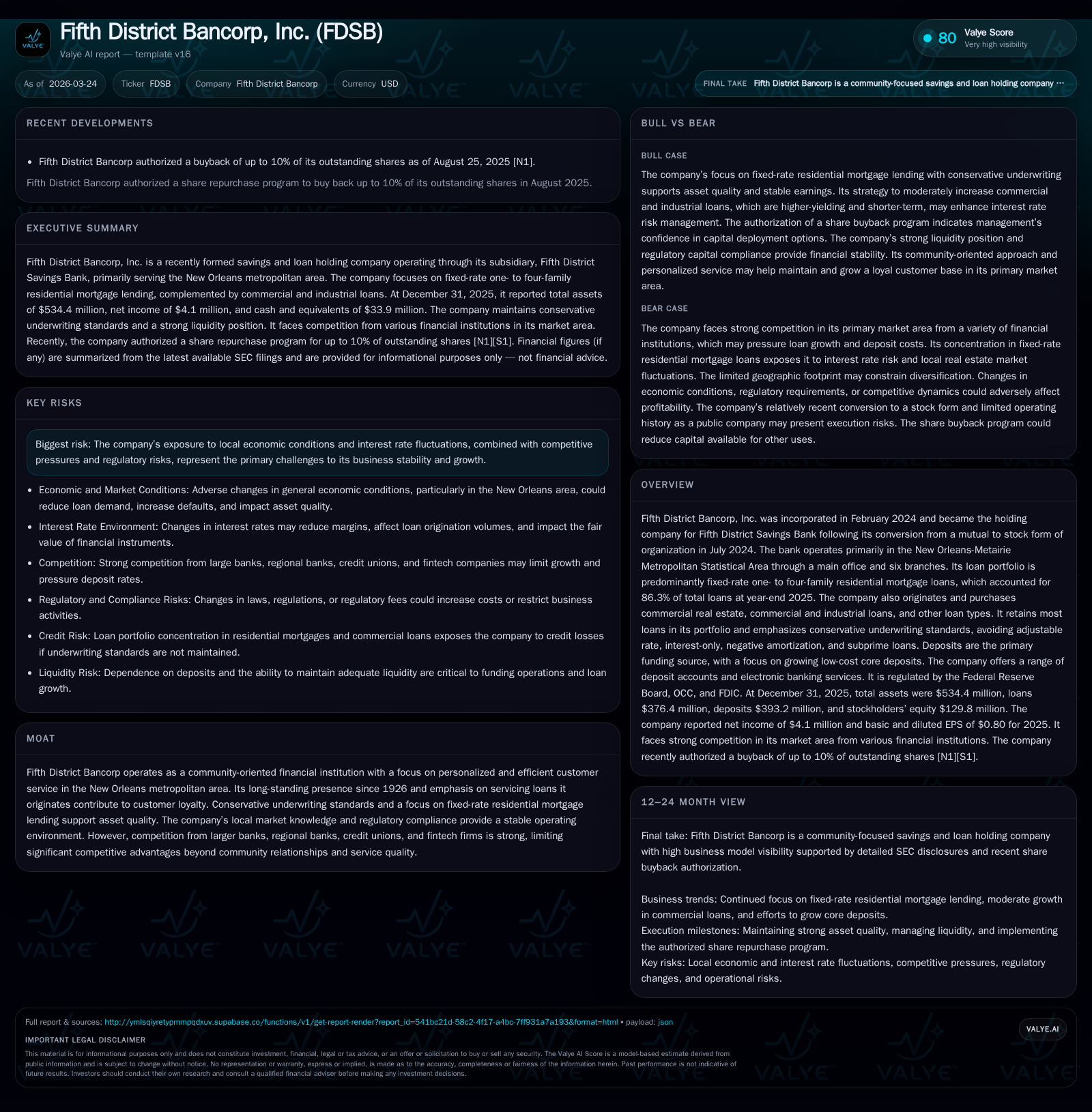

Incorporated in early 2024 after converting from a mutual savings bank, Fifth District Bancorp operates as a local lender concentrated in fixed-rate one- to four-family residential mortgages in the New Orleans area. Its conservative underwriting and retention of originated loans support strong asset quality, though growth remains moderate due to localized market constraints and competitive pressures. The bank’s recent financials show a rebound to profitability and positive cash flow, backed by stable deposits and disciplined capital management including a substantial stock repurchase program but no dividends yet.

Company Background and Historical Growth

Fifth District Bancorp, Inc., formed in February 2024 following its conversion from a mutual savings bank to a stock holding company in July that year, serves primarily the New Orleans-Metairie MSA through a main office and six branches [S1]. Its roots trace back nearly a century as a community-oriented financial institution focusing heavily on fixed-rate one- to four-family residential mortgage loans, which accounted for approximately 86.3% of total loans at December 31, 2025 [S5]. The bank also originates commercial real estate and commercial & industrial loans comprising around 6.6% of the loan book [S5].

The company's loan portfolio growth has been gradual post-conversion. Loans receivable (net) expanded by $9.1 million or roughly 2.5% during fiscal year 2025 compared to the prior year; this net increase reflects gross originations of $58.5 million offset by repayments totaling $49.4 million [S26]. Commercial loans contributed an increase of $10.4 million driven mainly by commercial real estate and industrial originations, while one- to four-family mortgages declined by $6.9 million [S26]. This demonstrates management's intention to moderately diversify the loan book beyond its dominant residential base without compromising credit standards.

Deposits—the primary funding source—also showed tempered growth rising marginally by $1.7 million or about 0.4% during the same period [S26]. Certificates of deposit rose slightly ($925K), accompanied by shifts within deposit category compositions: NOW accounts increased but money market accounts decreased [S28]. Core deposits (non-time deposits) represented approximately 39% of total deposits as of year-end [S5], reflecting efforts to improve stable funding leverage.

Financial performance rebounded substantially between the fledgling entity’s first full fiscal year (2024) and fiscal year ended December 31, 2025. Net income swung from a loss of $1.08 million in FY24 to positive earnings of approximately $4.09 million in FY25—a nearly fivefold improvement [F1]. Operating cash flow followed suit moving from negative $1.05 million to positive $1.33 million, yielding free cash flow (operating cash flow minus capex) near $942,000 after accounting for reduced capital expenditures ($384K vs $510K prior year) [F1]. Equity grew modestly from roughly $125.8 million to about $129.8 million reflecting retained earnings accumulation less share repurchases [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($) | Capex ($) | Net YoY |

|---|---|---|---|---|

| 2025 | 4 | 1326000 | 384000 | +479.2% |

| 2024 | -1 | -1054000 | 510000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($) | ROE% |

|---|---|---|

| 2025 | 942000 | 3.2 |

| 2024 | -1564000 | -0.9 |

Source: SEC companyfacts cache [F1].

Business Model and Strategic Positioning

Central to Fifth District Bancorp's operations is its niche as a community-focused lender committed to serving local customers with personalized banking services [N/A Overview]. The bank maintains its entire loan servicing internally rather than selling servicing rights—a practice that fosters closer borrower relationships and improves collection insight [N/A Moat]. Conservative underwriting policies exclude adjustable-rate mortgages or riskier product structures such as interest-only or subprime loans; this prudence stabilizes asset quality though limits yield enhancement opportunities [S11].

Its product suite is anchored by fixed-rate residential mortgages predominantly for owner-occupied properties that rely heavily on borrower employment income verification coupled with external appraisals for collateral valuation . This complements its smaller footprint commercial lending activities where repayment ability is assessed via borrower cash flows alongside pledged collateral that tends to be less liquid or harder to value precisely compared to residential assets .

Funding emphasis lies mainly on attracting low-cost "core" deposits—consisting primarily of transactional accounts and retail savings—which enhances net interest margin stability versus reliance on certificates of deposit or wholesale borrowings . While certificates account for over half of total deposits ($239.7 million out of $393.2 million total), management continues efforts to build core balances organically plus capitalize on existing relationships for deposit gathering from commercial borrowers [S28]. Importantly, as a member of the Federal Home Loan Bank system with stocks held but no advances drawn at end-2025 ($0 outstanding against capacity ~$188M collateralized limit), the bank retains contingent liquidity options without current reliance .

Industry Context and Competitive Environment (Analysis)

As a community lender operating exclusively within Southeast Louisiana's New Orleans metro vicinity, Fifth District Bancorp faces notable pressures common across localized banking franchises: modest market sizes limiting organic balance sheet expansion; intense competition from larger regional banks wielding superior scale economies; credit unions offering attractive rates fueled by non-profit status; and emerging fintech platforms targeting mortgage origination efficiency or deposit innovation.

Despite these headwinds, long-term presence since 1926 underpins customer goodwill alongside regulatory compliance bolstering operational stability—valued traits among conservative borrowers especially post-financial crisis periods [N/A Moat]. Regulatory frameworks impose capital conservation buffers constraining liberal dividend or repurchase programs until earnings consistency improves beyond nascent stockholder bases such as post-mutual conversions . The firm's deliberate avoidance of volatile loan products coupled with internal servicing reduces credit risk exposure relative to industry trends toward more aggressive lending.

However, localized economic dependencies—e.g., oil sector fluctuations influencing employment—and sensitivity to house price movements necessitate vigilance around condition shifts which may impair collateral realizations or borrower repayment ability impacting asset quality metrics despite currently low nonperforming asset ratios (~0.1%) [S5,S16,S20].

Future Growth Prospects and Risks

Management articulates intent to sustain focus on fixed-rate one- to four-family home mortgage lending while incrementally growing commercial & industrial portfolios which offer shorter terms and higher yields beneficial for interest rate risk mitigation [S5]. Growth avenues also include opportunistic branching or acquisitions within the community banking sphere though no immediate network expansions are planned indicating measured resource deployment strategies calibrated against market realities [N/A Overview,S26].

Areas potentially limiting growth include:

- Geographic concentration risks heightening exposure to local economic downturns.

- Competition restricts pricing power for both lending yields and deposit costs.

- Regulatory constraints affecting dividend distributions and permissible activities while requiring robust capital cushions.

- Interest rate fluctuations impacting loan demand elasticity and net interest margins.

- Potential prepayment volatility inherent with fixed-rate mortgage portfolios complicating duration matching.

Conversely, opportunities exist through expanding commercial loan generation tied to improving regional economic momentum plus enhancing digital service capabilities might augment customer acquisition though competing fintech entrants remain agile threats.

Capital Allocation and Returns Profile

The company has adopted active capital return policies post-conversion including authorization of a publicly disclosed stock repurchase plan permitting buyback up to approximately 10% of shares outstanding (555,947 shares authorized) initiated August 25, 2025; cumulative repurchases totaled roughly 173,711 shares through December quarter end at an average price near $13.72 per share reflecting management’s preference for share count reduction over dividends currently [S24,F1].

No dividends had been declared or paid through end-2025 due largely to regulatory considerations mandating earnings stability plus preservation of capital during early public company stages [S22]. With an approximate trailing twelve-month return on equity near 3.2%, Fifth District shows nascent but positive profitability given its recent turnaround after operating losses during conversion transition periods [F1]. Operating cash flows turning positive combined with modest capex needs illustrate internal funding capacity consistent with conservative balance sheet management.

Regulatory capital ratios classify the institution as well-capitalized under OCC guidelines as of December 31, 2025 supporting continued dividend/distribution flexibility when earnings permit albeit cautious prudence prevails consistent with community institution norms .

Milestones and What To Watch (Analysis)

Without explicit public forward guidance beyond strategic objectives in filings there remains key monitors going forward:

- Quarterly EPS trajectory confirming sustained profitability improvements beyond inaugural public fiscal years.

- Loan portfolio mix shifts indicating acceleration in higher-yielding commercial loans relative share gains without compromising credit standards.

- Deposit composition dynamics evidencing growth in low-cost core deposits supporting net interest margin expansion.

- Capital adequacy metrics maintaining well-capitalized classification supporting future shareholder return initiatives including potential dividends.

- Asset quality metrics amid any regional economic headwinds especially monitoring delinquencies/nonperformers given concentration profiles.

- Competitive pressures evidenced through local market share changes particularly versus regional super-community banks or innovative new entrants.

Conclusion

Fifth District Bancorp’s transformation into a publicly held entity represents an archetype community bank balancing heritage localized customer service with prudent risk controls focused overwhelmingly on steady fixed-rate residential mortgages supplemented by measured commercial lending growth initiatives within its New Orleans franchise base. The firm’s conservative underwriting discipline paired with repeat servicing relationships underpin robust asset quality presently reflected through minimal problem loans metrics despite modest volume growth constraining top-line expansion.

Financial performance has returned solidly into black following conversion-related challenges highlighted by substantial net income recovery accompanied by positive operating cash flows facilitating governance through disciplined capital allocation—especially via meaningful share buybacks though dividends await future earnings sustainability signaling maturity progression.

Investors tracking Fifth District should weigh its relatively limited geographic diversification against strong community ties alongside the cautious yet sound approach taken amid competitive landscapes increasingly dominated by scale players armed with technology advantages intersecting traditional banking franchises trying to maintain relevance via service differentiation.

This analysis is based solely on publicly available information including recent SEC filings for Fifth District Bancorp as of March 24, 2026 ([S1]-[S29]) and summarized financial data ([F1]). It does not constitute investment advice nor an endorsement regarding securities purchase decisions.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments