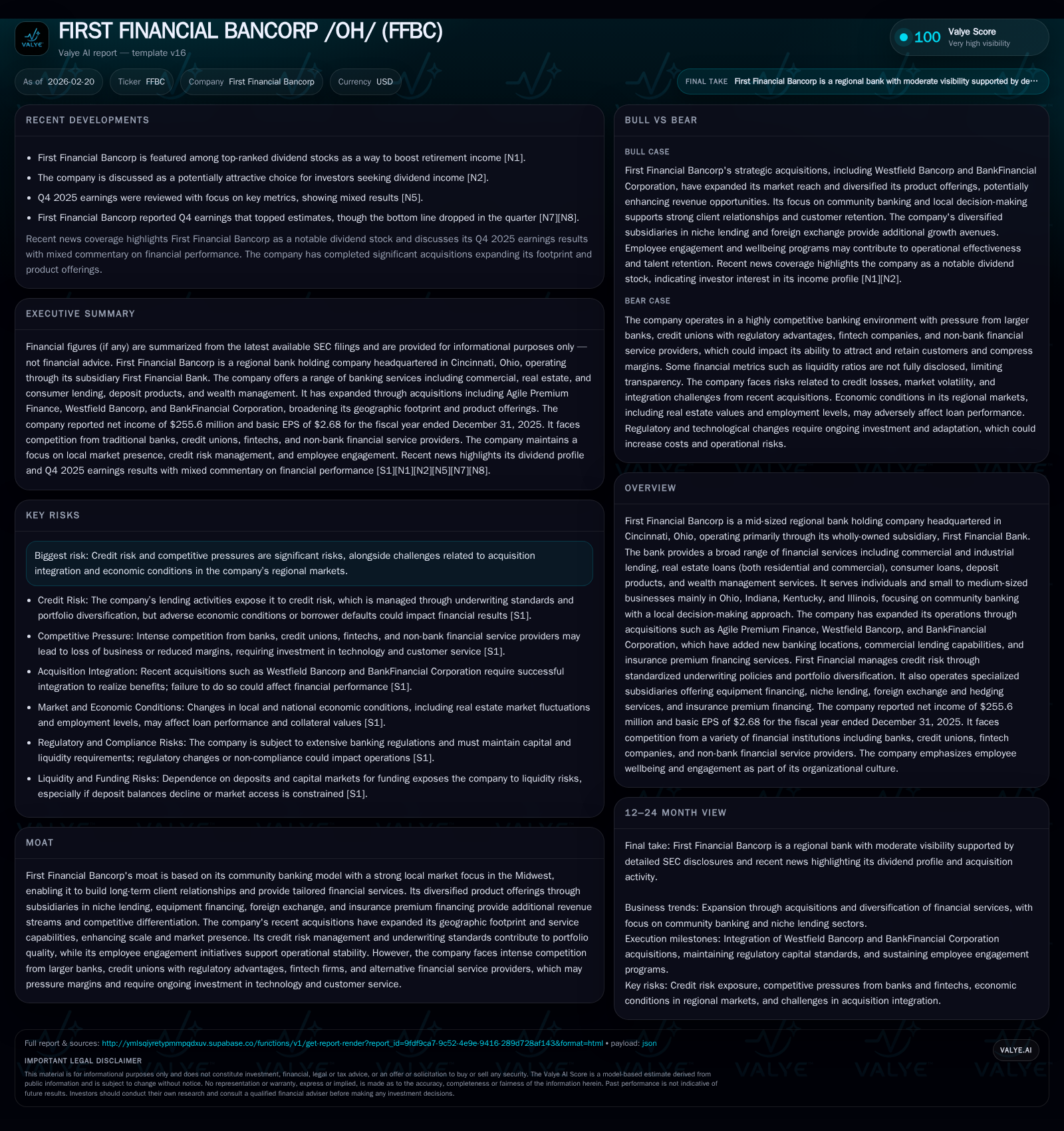

First Financial Bancorp’s Regional Focus and Acquisition Strategy Drive Moderate Profit Growth Amid Competitive Pressures

FFBC leverages community banking and diversification through acquisitions to maintain steady earnings and manage credit risk in the Midwest.

First Financial Bancorp (FFBC), a Cincinnati-based regional bank with a footprint centered in Ohio, Indiana, Kentucky, and Illinois, has grown primarily through community banking complemented by strategic acquisitions such as Westfield Bancorp and Agile Premium Finance. Its core strengths include diversified lending, tailored client relationships, and disciplined credit risk management. Over the last four years, FFBC delivered moderate earnings growth supported by acquisition-driven scale, with net income rising 11.7% year-over-year to $256 million in FY2025 [F1]. Going forward, revenue growth will depend on further integration of recent acquisitions, managing competitive pressures from larger banks and fintechs, and navigating evolving regulatory landscapes [S10][S25]. Capital discipline has been steady with consistent dividend payouts but no recent buybacks [F1]. Monitoring deposit trends and credit quality amid macroeconomic shifts will be critical for upcoming performance milestones.

Overview of First Financial Bancorp

First Financial Bancorp (FFBC) is a mid-sized regional bank holding company headquartered in Cincinnati, Ohio. Operating primarily through its wholly owned subsidiary First Financial Bank—themselves founded in 1863—FFBC focuses on community banking in four Midwest states: Ohio, Indiana, Kentucky, and Illinois [S1][S6]. The company pursues a business model anchored on close local customer relationships facilitated by local decision-making authority. It offers an extensive range of financial services that span commercial & industrial lending, residential and commercial real estate loans, consumer credit products, deposit accounts, equipment leasing through Summit Funding Group, wealth management services, as well as foreign exchange transactions via Bannockburn Global Forex division [S1][S20].

Historical Performance & Key Financials

Over the past four years (FY2022–FY2025), FFBC showed moderate but consistent profitability improvement underpinned by both organic business growth and selective acquisition activity. Net income rose from $217.6 million in FY2022 to $255.6 million in FY2025 representing roughly an 11.7% year-over-year increase from FY2024 to FY2025 alone [F1]. Operating cash flow increased more sharply by almost 29% YoY during this period while capital expenditures remained relatively stable near $20-24 million annually indicating controlled investment spending congruent with steady branch operations or technology upgrades [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 256 | 338 | 21 | +11.7% |

| 2024 | 229 | 262 | 21 | -10.6% |

| 2023 | 256 | 487 | 24 | +17.6% |

| 2022 | 218 | 201 | 14 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Rev, OpInc. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks | FCF ($mm) |

|---|---|---|---|

| 2025 | 95 | 317 | |

| 2024 | 90 | 241 | |

| 2023 | 87 | 0 | 463 |

| 2022 | 87 | 0 | 187 |

Source: SEC companyfacts cache [F1].

Note: Revenue and operating income are not available from provided data.

The approximate return on equity for FY2025 stands at around 9.2%, which reflects a reasonable risk-adjusted profitability metric for a regional bank balancing local focus with growth investments [F1]. Dividend payments have shown modest increases annually with no common stock repurchases recorded since FY2022 after notable buybacks in earlier years suggesting a cautious capital allocation posture amid expansions [F1].

Growth Drivers & Business Segments

Growth at FFBC has been propelled by several factors:

Geographic Expansion Through Acquisitions: Recent acquisitions including Westfield Bancorp added new banking centers predominantly in Ohio/Kentucky markets while purchases like Agile Premium Finance enhanced specialty lending tied to insurance premium financings nationwide [S6]. These transactions increased scale breadth geographically while diversifying loan product mix.

Diverse Loan Portfolio: FFBC manages its asset base across commercial & industrial debt used for working capital or equipment financing; real estate loans segmented into residential single-to-four family homes as well as investor-owned commercial properties; consumer loans like vehicle financing; alongside lease/equipment financing via Summit Funding Group catering especially to franchisees primarily in quick service/casual dining sectors where underwriting blends conventional credit assessment with franchise-specific knowledge frameworks [S1][S17][S20].

Specialized Units: Bannockburn’s foreign exchange operations serve middle-market clients nationwide providing structured hedging solutions exposing FFBC to markets beyond its core regional geography albeit concentrated among a few key counterparties posing some revenue volatility risk [S22][S23]. Additionally, Agile Premium Finance extends coverage to all U.S states enhancing fee-based income resilience.

Community Banking Model: The emphasis on local market expertise paired with relationship banking allows FFBC to compete effectively against larger institutions within its footprint despite increasing consolidation pressures (analysis).

Credit Risk Management

FFBC employs rigorous underwriting standards centralized through dedicated credit committees that assess borrower creditworthiness comprehensively including cash flows, guarantor strength, collateral valuations while enforcing authorized exposure limits per client or sector segments [S1][S17][S23]. Their allowance for credit losses incorporates the current expected credit loss (CECL) methodology reflecting lifetime loss expectations based on historical data coupled with forecasts incorporating macroeconomic variables.

In fiscal year 2025 alone they recorded $36.5 million in provision expenses attributable to net charge-offs alongside growing balances indicating proactive recognition of potential impairments amidst economic cycles affecting consumer incomes or business performance within their markets [S23]. This conservative approach is typical among regionals seeking to maintain portfolio quality amid sectoral uncertainties such as manufacturing slowdowns or shifts in retail franchise health.

Competitive Environment & Industry Risks

FFBC operates within a crowded field of competitors ranging from large national banks—benefitting from scale advantages—to credit unions advantaged by preferential regulations allowing them price leadership on multiple products without corresponding tax burdens [S10][S24][S27]. Fintech entrants intensify pressure particularly on the mortgage and consumer loan segments offering digital end-to-end lending platforms eliminating branch overheads thereby enabling competitive pricing or faster turnaround times threatening traditional community banks’ foothold.

Additionally emerging innovations like stablecoins under the GENIUS Act regulatory umbrella introduce alternative payment systems potentially eroding deposit bases forcing banks like FFBC to evolve technologically while managing traditional deposit flight risks given heightened liquidity sensitivity amidst rapid digital asset migration trends [S24][S27]

Regulatory risks remain material encompassing anti-money laundering compliance under the Patriot Act regime; evolving CFPB enforcement patterns particularly following funding adjustments; cybersecurity mandates exponentially expanding due diligence costs; as well as detailed Basel III capital adequacy standards imposing buffer requirements potentially constraining capital distributions or acquisitions unless capital positions remain robust [S4][S7][S11][S21].

Capital Allocation & Liquidity Positioning

Capitalization appears sound with equity growing consistently alongside net income gains reflecting retained earnings reinvested to support asset expansions including accumulation of loan portfolios post-acquisitions [F1][S21]. No repurchases recently signals prioritization of balance sheet strength over returning capital via buybacks possibly reflecting integration costs or regulatory conservatism amid uncertain economic conditions.

Dividends have been steadily maintained in line with earnings growth paying approximately $94.6 million in FY2025 up roughly 5% from prior year signaling shareholder returns are balanced against liquidity needs [F1]. Liquidity management remains crucial given accelerated deposit volatility catalyzed by digitization accelerating mobility out of traditional deposits into alternative assets such as money market funds or cryptocurrencies requiring optimal stress test procedures instilled routinely within treasury functions [S14][S7].

Outlook & Key Milestones To Monitor

Forward growth depends largely upon:

- Successful assimilation of recent acquisitions driving incremental cross-sell opportunities without excessive cost overruns or customer attrition noted typically post-merger integration phases;

- Sustaining asset quality especially commercial loan concentrations sensitive to regional economic cycles including manufacturing headwinds prevalent across Midwestern markets;

- Navigating competitive threats posed by FinTechs embedding financial services digitally reducing reliance on physical branch footprints;

- Proactive regulatory adherence aligned with evolving capital policies influencing capacity for dividends or share repurchases;

- Maintaining diversified non-interest revenue streams via specialized subsidiaries Bannockburn and Agile Premium Finance despite inherent concentration risks highlighted;

- Managing cybersecurity risks increasingly critical as customer data volumes grow alongside digital channel adoption.

Specific guidance remains limited absent explicit forecast details from management disclosures but investor attention should focus on quarterly filings analyzing net interest margin trends given funding cost fluctuations; loan loss provisioning trajectory reflecting economic assumptions; balance sheet mix shifts between loans versus securities holdings; and efficiency ratio movements indicative of technology or branch network investments balancing cost controls versus growth imperatives.

Conclusion

First Financial Bancorp represents a quintessential regional bank balancing tradition and scale expansion through acquisitions targeting the Midwest's robust community markets supplemented by niche specialty finance units enhancing revenue diversity. While growing prudently evidenced by solid profit increases and stable returns on equity over recent years coupled with consistent dividend policies it confronts mounting challenges from larger competitors wielding scale advantages alongside nimble fintech disruptors reshaping client expectations around speed & pricing.

Ongoing regulatory complexity demands continuous adaptation reflected in substantial compliance efforts spanning AML programs through cybersecurity readiness underscoring operational resilience importance alongside credit risk vigilance fundamental amid potential economic volatility across core market geographies.

Investors should observe integration outcomes of new acquisitions particularly whether these achieve planned synergies without diluting asset quality or inflating operating costs materially while also monitoring macroeconomic signals impacting loan demand or repayment capabilities across various borrower classes served.

This analysis provides an overview based on publicly available SEC filings up to February 19, 2026 ([F1],[S1]-[S29]) and supplementary news reports without offering investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments