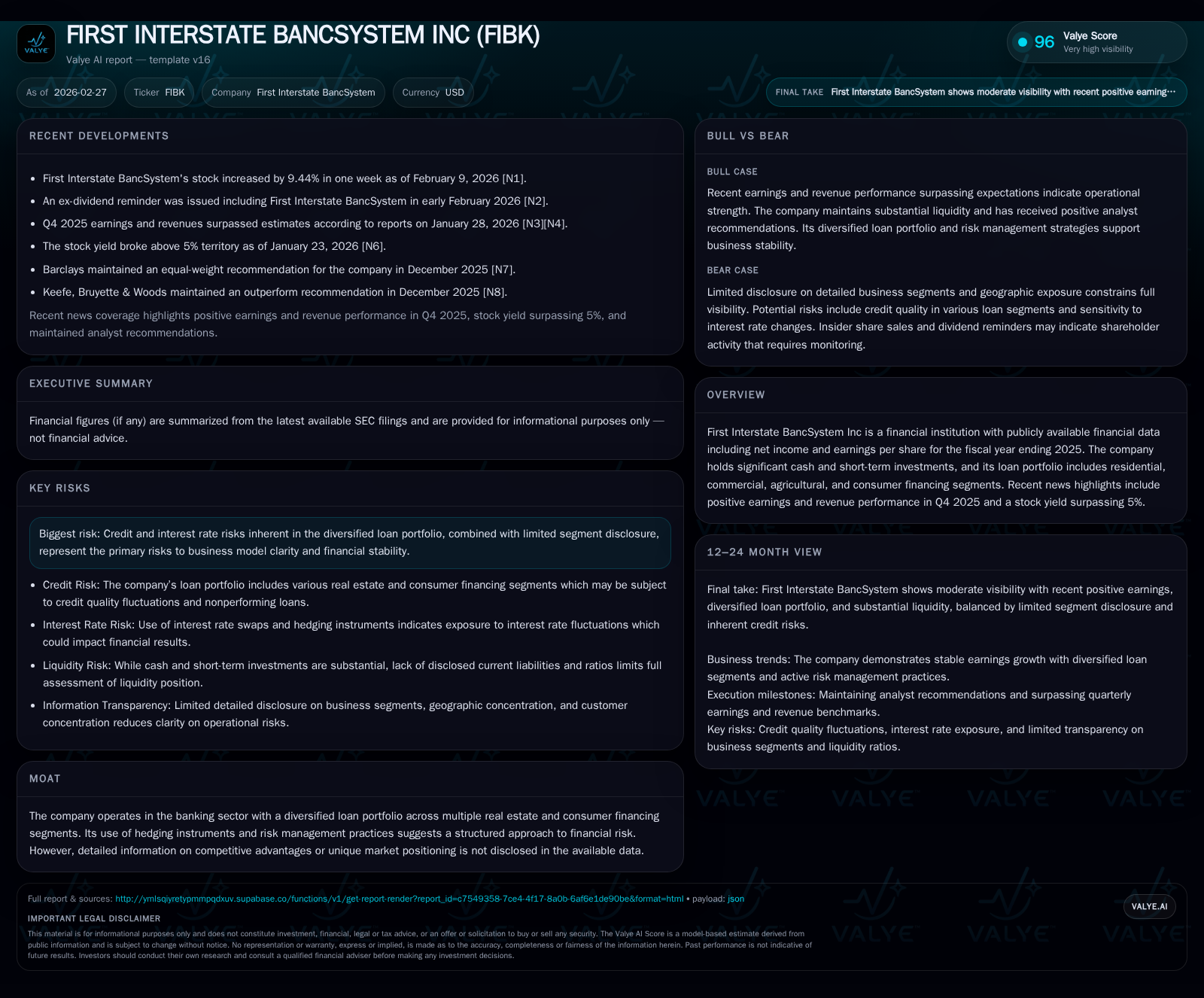

First Interstate BancSystem's Earnings Upswing and Portfolio Risks in 2025

A detailed examination of FIBK’s financial surge alongside emerging credit concentrations and regulatory headwinds.

First Interstate BancSystem Inc (FIBK) experienced a significant net income increase of 33.7% in FY2025, largely propelled by its diversified loan portfolio and robust quarter-end earnings, which lifted its stock yield above 5%. Yet, the firm’s heavy exposure to commercial real estate lending—representing approximately 69.1% of loans—and recent commercial loan charge-offs underscore underlying credit risk sensitivities amid an evolving regulatory environment. Capital allocation reflects a balance between steady dividends and meaningful share buybacks, signaling management confidence despite moderate returns on equity near 8.8%. Going forward, stakeholders should monitor credit quality trends, FDIC assessment rates, and regulatory developments impacting fee structures.

Strong Earnings Momentum and Historical Growth Trends

First Interstate BancSystem demonstrated notable financial momentum through fiscal year ending December 31, 2025. Net income grew impressively by approximately 33.7%, from $226 million in FY2024 to $302.1 million in FY2025 [F1]. This surge was underpinned by solid revenue performance driven by its diversified lending activities and effective banking operations highlighted in positive Q4 earnings results that exceeded market expectations [N1][N2]. However, this expansion was somewhat offset by a decline in operating cash flow, which fell by about 13.9% to $305.6 million in FY2025 compared to the prior year’s $355 million [F1]. The drop suggests changing liquidity patterns within operational segments potentially related to loan portfolio shifts or working capital adjustments.

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Net YoY |

|---|---|---|---|

| 2025 | 302 | 306 | +33.7% |

| 2024 | 226 | 355 | -12.2% |

| 2023 | 258 | 428 | +27.3% |

| 2022 | 202 | 534 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | ROE% |

|---|---|---|---|

| 2025 | 194 | 122 | 8.8 |

| 2024 | 196 | 1 | 6.8 |

| 2023 | 195 | 34 | 8.0 |

| 2022 | 182 | 199 | 6.6 |

Source: SEC companyfacts cache [F1].

Note: ROE for FY2025 derived as net income divided by equity per available data.

Loan Portfolio Composition and Credit Risk Drivers

At the core of First Interstate BancSystem’s business is a heavily weighted commercial lending segment where commercial real estate loans alone represent approximately 69.1% of the loans held for investment as of December 31, 2025 [S1]. Such concentration exposes FIBK to cyclical risks inherent in the real estate market and broader economy since repayments depend largely on the operational success of the associated properties or ventures rather than solely collateral liquidation values.

The bank recognized a significant impairment charge-off amounting to about $15.8 million in Q4 2025 related to a troubled commercial real estate loan facing adverse borrower-specific conditions [S1]. This event underscores vulnerabilities that can materialize swiftly within large-sized commercial loans that lack fungible collateral.

Moreover, First Interstate BancSystem’s exposure extends into agricultural sectors indirectly affected by volatile commodity prices influencing crop producers, livestock businesses, transporters, and equipment manufacturers [S1]. Shifts in supply-demand fundamentals globally or regionally can impact borrowers’ cash flows and creditworthiness.

These factors collectively signal that credit risk management remains paramount amid an economic backdrop with uneven sectoral recoveries and inflationary pressures affecting input costs.

Regulatory Landscape and Its Influence on Operations

Regulatory compliance remains a complex element shaping First Interstate BancSystem’s operational costs and strategic response frameworks.

Post-pandemic surges in insured deposits caused a thinning of the Deposit Insurance Fund ratio below statutory minimums, prompting the FDIC to raise insurance assessment fees substantially—first via higher baseline rates then through additional special assessments directly impacting FIBK’s expense base [S1]. Future increases are possible if economic conditions weaken or deposit volumes rise further.

Additionally, heightened scrutiny from the Consumer Financial Protection Bureau (CFPB), particularly focused on fee-based revenue streams including overdraft and late fees common in consumer finance businesses, introduces compliance uncertainties and potential remediation obligations [S1]. The evolving "open banking" rules under Dodd-Frank Section 1033 may also compel adjustments to data accessibility practices with further regulatory revisions anticipated amid ongoing litigation.

These regulatory dynamics necessitate vigilant monitoring as they can influence profitability, customer engagement strategies, and technology investments.

Capital Allocation: Dividends, Buybacks, and Liquidity

Management’s capital deployment strategy reveals a cautious yet assertive stance noteworthy for buy-side analysts.

Dividends remained broadly stable near $194 million for FY2025 versus $195.9 million in FY2024 [F1], reflecting commitment to maintaining shareholder income streams despite rising regulatory costs discussed above.

Conversely, share repurchase activity accelerated markedly: buybacks rose from roughly $1.2 million in FY2024 to nearly $121.9 million in FY2025 [F1], signaling confidence in valuation levels and future cash flow prospects.

Even with these outflows, equity grew moderately to around $3.45 billion at year-end FY2025 compared to $3.30 billion previously; however, reported return on equity stands at a measured level of approximately 8.8%, implying capital efficiency merits continued attention [F1].

Liquidity positioning benefits from substantial balances of cash and short-term investments as per SEC filings while hedging instruments help stabilize interest rate exposures within lending books [S4][S5].

Forward-Looking Views: What Investors Should Monitor

While explicit multi-year guidance is absent from reported materials, several key indicators warrant focus going forward:

- Credit quality evolution within heavily concentrated commercial real estate loans given macroeconomic uncertainty; watch for signs of increased delinquencies or further charge-offs as early distress signals.

- Changes in FDIC insurance assessment rates remain an external cost variable capable of compressing net margins depending on federal deposit fund health.

- Regulatory developments around CFPB enforcement policies on fees and open banking data access may require operational shifts or increased compliance spending.

- Interest rate trajectory influences loan yields versus funding costs; keen observation of Fed policy impacts will be crucial amid possible volatile rate cycles.

- Market reaction post-Q4 earnings highlights momentum but also places emphasis on sustaining underlying fundamentals amid sector risk exposures [N4][N6].

Collectively these areas form the core analytic framework for evaluating FIBK’s near-to-mid-term prospects under current economic conditions.

Conclusion: Balancing Yield, Growth, and Risk

First Interstate BancSystem presents an intriguing profile characterized by strong recent earnings growth juxtaposed against concentrated commercial lending risks and intensifying regulatory expense pressures.

The firm’s disciplined capital allocation—with consistent dividends complemented by escalated buybacks—signals shareholder alignment albeit tempered by mid-single-digit returns on equity that suggest room for improved capital efficiency.

Fundamentally, the concentration in commercial real estate loans drives both upside via revenue generation during stable cycles and downside vulnerability amid sector stress as exhibited by recent impairment recognition.

Navigating this dynamic requires continuous vigilance over credit trends alongside keen sensitivity to regulatory shifts particularly those emanating from enhanced FDIC deposit insurance cost structures and unfolding CFPB oversight enhancements.

For stakeholders analyzing FIBK’s positioning within the regional banking landscape, appreciating this tripartite balancing act between yield attraction, growth sustainability, and inherent portfolio risks is essential for informed due diligence.

Disclaimer: This analysis is provided solely for informational purposes based on publicly available data as of February 27, 2026,[F1][N#][S#] without any recommendation regarding securities or investment strategies.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments