BingEx’s Dedicated Courier Model Drives Resilient Growth Amid Regulatory Shifts

Recent quarterly results highlight BingEx’s operational resilience driven by its distinctive on-demand dedicated courier approach despite regulatory headwinds.

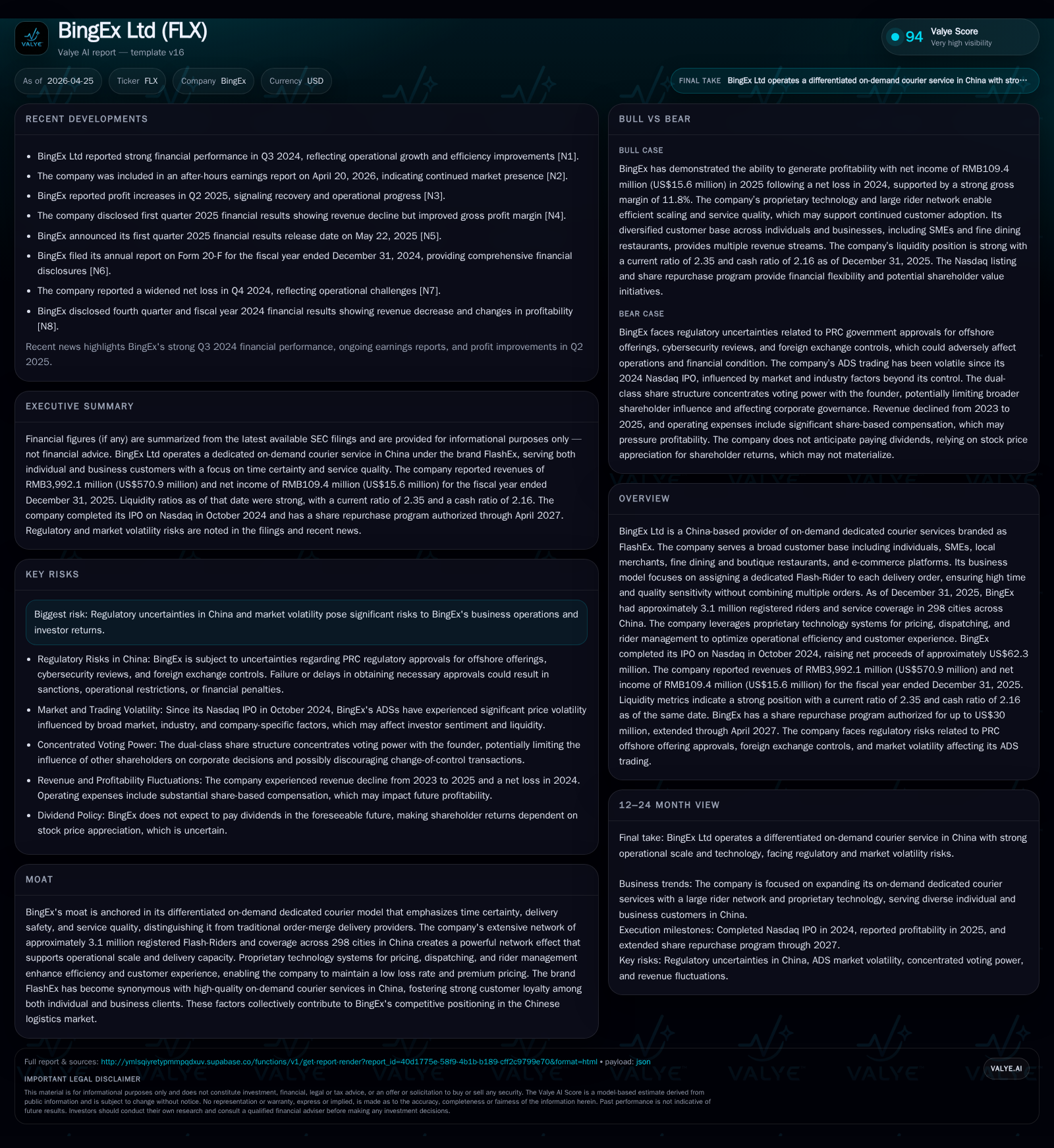

In its latest 6-K filing for Q4 and FY2025, BingEx Ltd demonstrated a rebound in net income and operational improvements, affirming the strength of its specialized dedicated courier business model. The firm’s FlashEx brand leverages a vast network of 3.1 million registered flash-riders across nearly 300 Chinese cities, supported by proprietary dispatch and pricing technology that optimizes delivery speed and efficiency. Although revenues dipped slightly in 2025 amid macroeconomic and regulatory pressures, BingEx managed to improve margins and return to profitability, underscoring the durability of its unit economics. Regulatory uncertainty in China remains a significant risk factor impacting strategic execution and capital flows.

Latest Quarterly Performance Validates Operational Resilience

BingEx Ltd's latest quarterly update reported on March 17, 2026 ([S2]) reveals encouraging signs of operational stability entering FY2026 despite ongoing macroeconomic pressures. The company announced financial results demonstrating a net income rebound from the prior year loss to RMB109.4 million (~US$15.6 million) in 2025 supported by improved operational efficiency. Average local delivery times shortened consistently over recent years—down from 29 minutes in 2023 to 26 minutes in 2025—highlighting continuous service enhancements critical for customer satisfaction.

Order volumes completed fell slightly to 249.2 million in 2025 from 277.2 million in 2024 but remained sizable given external conditions. Flash-Rider remuneration costs decreased both nominally and as a percentage of revenue (to ~84.5%) reflecting productivity gains and disciplined cost controls ([S1], [S4]). These factors underpin BingEx's ability to maintain premium-priced services without compromising quality.

Distinctive Business Model Centered on Dedicated, Time-Sensitive Delivery

BingEx’s core value proposition centers around the FlashEx on-demand dedicated courier model that distinguishes it from typical order-merge services prevalent among competitors ([S5], [S6]). Each delivery is assigned a dedicated flash-rider who handles the order exclusively from pick-up to drop-off without combining parcels or multi-order batching. This approach delivers precise time certainty, enhanced safety for high-value items such as gourmet food or legal documents, and superior service consistency.

Its diversified customer portfolio includes individuals seeking reliable personal deliveries alongside SMEs, fine dining establishments, boutique restaurants, e-commerce merchants, real estate agencies, law firms, and electronics manufacturers requiring customized logistics solutions ([S6], [S12]). This breadth of client segments reduces concentration risk while reinforcing BingEx’s strategic role within their operations.

The crowd-sourcing paradigm enables flexible participation by millions of riders who set their own schedules and use various transport modes—from motorcycles to public transit—effectively scaling coverage with controlled fixed costs ([S23]). Payment algorithms dynamically price deliveries based on multiple factors including distance and parcel attributes while optimizing rider incentives to ensure robust supply responsiveness.

Integrated Technology Enhances Flash-Rider Dispatch Efficiency

A backbone of BingEx’s competitive strength lies in its proprietary technology stack facilitating real-time intelligent pricing and automated dispatching ([S4], [S13]). The system allocates orders to nearby flash-riders swiftly while optimizing delivery routes using data analytics aimed at minimizing delays and fuel consumption.

This technological infrastructure not only enhances rider utilization rates but also enforces quality control via digital performance monitoring and rating to retain top-performing riders ([S23]). Such integration drives solid unit economics by balancing supply-demand dynamically amidst fluctuating urban densities.

Competitive Dynamics in China's On-Demand Courier Market

With an extensive network of approximately 3.1 million registered flash-riders spread throughout 298 Chinese cities as of end-2025 ([S1]), BingEx commands a substantial presence difficult for new entrants to replicate quickly due to logistical complexity and capital intensity.

Its focused dedication model cultivates 'order certainty'—a key differentiator recognized by customers valuing timeliness over lowest cost—enhancing pricing power amid intense competition from conventional aggregators that merge deliveries ([S14]).

Nonetheless, the evolving regulatory landscape introduces complexities; recent amendments to China's Anti-Monopoly Law impose stricter scrutiny over dominant market behaviors potentially affecting pricing strategies ([S8], [S14]). Furthermore, ongoing oversight from PRC authorities pertaining to overseas listing compliance underlines operational regulatory risk appetite.

Growth Catalysts: Urban Coverage Expansion and Customer Loyalty

Long-term growth hinges on continued urbanization driving demand for rapid local delivery services aligned with rising disposable incomes ([S1]). BingEx leverages social media campaigns, celebrity endorsements, rider branding uniforms, and referral programs targeting tech-savvy younger demographics to boost retention and acquire new users cost-effectively ([S20]).

The company tailors marketing efforts respecting differing city purchasing power profiles while incentivizing premium service usage through brand mind-share building around FlashEx's reputation for reliability ([S20]). Strategic expansion into underserved mid-tier cities can unlock incremental volume although saturation risk looms as competitive providers intensify their footprint.

Regulatory Risks and Their Impact on Strategic Execution

The company faces material risks linked to Chinese government regulation encompassing CSRC approvals for offshore offerings along with complex SAFE foreign exchange governance restricting overseas capital repatriation flows ([S8], [S18]).

The adoption of the Holding Foreign Companies Accountable Act (HFCAA) adds uncertainty with potential U.S. delisting if auditors are deemed inaccessible by PCAOB inspections—a risk seemingly mitigated currently but monitored closely ([S8]).

These regulatory constraints may curtail capital deployment agility or delay technology investments pivotal for maintaining competitive advantage. Cybersecurity review regulations further increase compliance burden potentially impacting data-driven innovations.

Key Milestones to Monitor for Execution and Demand Trends

Investors should track forthcoming Q2 order volume reports for evidence of market demand recovery or softness post-COVID normalization ([S2], [N1]).

Observation of marketing spend efficiency improvements will indicate if recent cost discipline translates into sustained customer acquisition gains. Additionally, rollout timing for next-generation dispatch algorithms or user experience enhancements will reflect R&D focus effectiveness.

Regulatory updates from CSRC or SAFE clarifying rules on capital movements or offshore fundraising remain crucial as these will influence BingEx’s financial flexibility and strategic maneuverability.

Financial Overview Underlining Improving Profitability and Liquidity

Historical performance (annual)

|

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 16 | 14 | 7 | 19000 | +178.0% |

| 2024 | -20 | 0 | -4 | 156000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 14 | 13.1 |

| 2024 | 0 | -19.6 |

Source: SEC companyfacts cache [F1].

BingEx returned to positive operating income territory with US$6.6 million in FY2025 after absorbing losses the previous year ([F1], [S2]). Net income likewise rebounded impressively from negative RMB146.5 million in 2024 to RMB109.4 million (US$15.6 million), translating into approximately 13% ROE based on year-end equity.[F1]

Revenue softened modestly by about 10%, reflecting deflationary industry factors but gross margin improved steadily nearing 11.8%, driven primarily by more efficient flash-rider remuneration ratios (down slightly from prior years' high eighties percentage range) ([S4], [F1]).

Selling & marketing expenses fell as management emphasized efficiency gains via digital channels versus broad-based discounts; R&D spending was curtailed following IPO phase stock comp accruals subsiding ([S15]).

Liquidity remains strong with US$80 million cash plus a current ratio surpassing two-fold providing a solid buffer against short-term volatility.[F1],[S2] Modest capex requirements underline the asset-light model enabling freed cash flow generation (approximate free cash flow over US$14 million).

|

| FY | Revenue (RMB m) | Operating Income (USD m) | Net Income (USD m) | Operating Cash Flow (USD m) | Capex (USD k) | Current Ratio |

|---|---|---|---|---|---|---|

| 2025 | 3,992 | 6.62 | 15.65 | 14.16 | 19 | 2.35 |

| 2024 | 4,468 | -3.53 | -20.07 | 0.30 | 156 | |

| 2023 | 4,529 | 10.65 | 19.70 | 44.66 | NA |

In summary, the latest filings underscore BingEx’s commitment to sustaining its differentiated courier model through technological innovation and strong network effects while cautiously navigating regulatory headwinds characteristic of China’s internet logistics sector.

Disclaimer: This analysis is for informational purposes only intended to provide industry context and company insights based on publicly available filings up to April 25, 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments