Femto Technologies Shifts Focus as New CRM Platform Drives Revenue Amid Cannabis Project Pause

Femto Technologies advances CRM software revenue amidst suspended cannabis facility plans and persistent customer concentration risks.

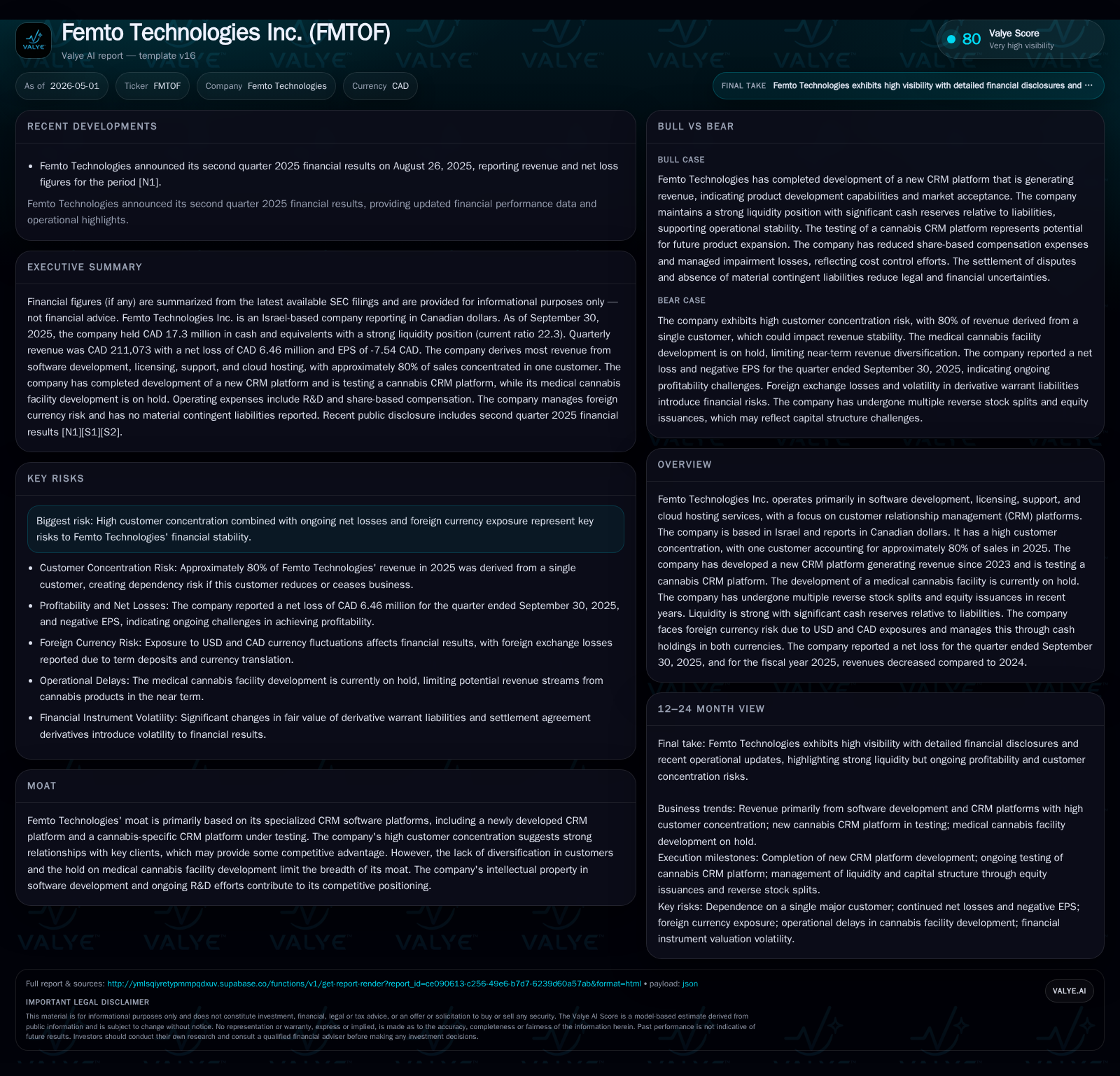

In its latest quarterly disclosure, Femto Technologies reported a revenue decline driven by lower software development sales and foreign exchange headwinds, while highlighting the commencement of revenues from its new core CRM platform launched in 2023. The cannabis-specific CRM platform is undergoing testing with no immediate revenue expectancy, and the medical cannabis facility project remains on hold. The company’s business model centers on specialized CRM software for SMEs with high reliance on a single major customer accounting for roughly 80% of sales. Although liquidity strength remains notable, customer concentration coupled with foreign currency exposure and net losses present ongoing challenges. Key near-term milestones include validation of the cannabis CRM solution and expansion of the Sensera device pipeline.

Latest Quarterly Operating Update: Revenue and Project Highlights

In its latest Form 6-K filed March 27, 2026 [S2], Femto Technologies disclosed fiscal-year revenues of CAD 846,531 for the year ended December 31, 2025—a noticeable decline from CAD 998,839 in the prior year [S1][S4]. The decrease is chiefly attributed to a drop of approximately CAD 161,146 in software development revenues alongside adverse foreign exchange movements between the Israeli Shekel (NIS) and Canadian dollar (CAD). Despite this contraction in top-line figures, gross margin remained positive but compressed at 12%, down from 15% a year earlier [S1].

The operating update spotlights a strategic pivot: completion and initial monetization of Femto’s new CRM platform initiated revenue streams beginning in 2023 [S1][S4]. Contrastingly, the company’s development effort on a cannabis-focused CRM solution has concluded but remains confined to testing phases at the Weizmann Institute of Science with no near-term revenue forecast [S1]. Additionally, funding constraints or strategic recalibrations have placed plans for a medical cannabis production facility on indefinite hold—a project that would have expanded Femto's direct participation in cannabis product sales [S1][S5]. These developments illustrate an operational focus shift towards SaaS-based software offerings over capital-intensive physical assets.

Importantly, Femto maintains a highly concentrated revenue base with approximately 80% of all sales attributable to one key customer during 2025 compared to about 67% in 2024 [S1][S4]. This dependency presents a critical variable impacting near-term stability and underscores risks tied to client retention.

Business Model Overview: Specialized CRM Software and Customer Dependency

Femto Technologies operates through its wholly owned subsidiary BYND Israel which develops proprietary Customer Relationship Management (CRM) software platforms geared predominantly towards small and medium-sized enterprises (SMEs) within Israel [S1][S13]. The flagship 'Benefit CRM' solution facilitates optimization across sales management, workforce coordination, contact center operations, and asset management—key operational domains where scalable cloud-based solutions increasingly anchor SME digital transformation efforts.

Revenue formula incorporates multiple streams: software development contracts for bespoke customization or upgrades; licensing fees for access rights; recurring support contracts providing continual maintenance; and cloud hosting fees enabling SaaS delivery models. This mix imbues predictable recurring income elements but remains susceptible to project timing variability mainly stemming from the bespoke development piece [S1].

Recently accomplished projects include launching a feature-enriched new generation Benefit CRM platform credited with initiating new revenue flows since mid-2023 [S1][S4]. Parallel efforts yielded a cannabis sector-specific CRM platform which targets regulatory compliance nuances and operational complexities unique to medical cannabis providers—a niche yet nascent market segment with uncertain adoption timelines [S1][S13].

The pronounced concentration of revenues towards a single dominant client reflects deep engagement but constrains diversification benefits. The company's approach includes close collaboration with its primary customer financing much of its ongoing R&D effort but simultaneously elevates operating leverage risks should this relationship falter [S1][F1].

Competitive Positioning within the CRM Software Sector

Within Israel's vibrant tech ecosystem focused on SME digital solutions, Femto positions itself as a specialized player offering integrated CRM suites enriched by proprietary intellectual property keenly tuned to operational workflows relevant to salesforce effectiveness and client interaction intelligence [S1][S13]. Its additional focus on emerging SaaS use-cases like medical cannabis adds an early-mover tilt into verticalized solutions that could develop durable positioning once regulatory clarity emerges.

Barriers within this niche arise from long product R&D cycles paired with established switching costs inherent in enterprise-grade CRM implementations—where data migration complexities and user retraining inhibit rapid churn once adopted. However, scale advantages enjoyed by global incumbents such as Salesforce or Microsoft Dynamics create stiff competitive headwinds that require Femto to emphasize domain-specific functionalities tailored for local compliance requirements or sector idiosyncrasies.

The successful rollout of their next-generation Benefit CRM platform signals incremental enhancement of product relevance though commercialization remains primarily domestic with limited geographic diversification currently [S1][S13]. Meanwhile, the immature state of the therapeutic cannabis market tempers imminent commercial upside from their segment-specific offering despite technological readiness.

Drivers of Growth: Product Innovation and Market Penetration

Key growth themes center first around expanding uptake of Femto’s new cloud-based Benefit CRM solution among Israeli SMEs seeking streamlined digitization pathways amidst intensifying competition. Product improvements such as enhanced analytics modules, mobile access facilitation, or AI-driven workflow optimization embedded within their offering serve as levers for differentiation [S13].

Secondly, successful completion of the cannabis CRM testing by the Weizmann Institute—expected timeline undisclosed—could unlock access to regulated medical marijuana operators who face challenging compliance monitoring demands. While currently non-revenue generating, this platform represents latent upside contingent upon regulatory trajectories within Israel’s evolving cannabis landscape [S5][S13].

Thirdly, continued research & development expenditures—rising notably due to initiatives like the Sensera Device—reflect strategic intent to diversify technological assets beyond software alone into IoT or smart devices which could integrate vertically with their existing platforms enhancing ecosystem value propositions [S6].

Finally, Femto has augmented its portfolio through acquisitions such as securing equity stakes in Gilad Planning & Implementation Technologies aiming to bolster AI capabilities embedded within its software services—aligning with wider industry shifts towards machine learning-enabled business tools [S7][S8].

Risks and Constraints: Customer Concentration and Currency Exposure

The overriding risk vector emanates from extreme customer concentration where reliance on one client drives approximately four-fifths of revenues raising acute counterparty risk exposure should contract renewal prospects dim or payment delays arise. This single-client dependency limits operational flexibility restricting strategic pivots or scaling impacts until broader customer adoption materializes [S1][F1].

Foreign currency risks compound complexity since operating denominated expenses span Israeli Shekels (NIS), Canadian dollars (CAD), and exposure linked to USD fundraising proceeds. Reported foreign exchange losses nearing CAD 910k during fiscal 2025 evidence material volatility implications affecting profitability metrics. Although cash holdings are managed across USD and CAD accounts partially offsetting translation risks, fluctuations remain an earnings sensitivity factor [S1][S20].

Ongoing net losses observed historically—a loss exceeding CAD 47 million in FY2024 transitioning towards net income in FY2025—reflect intensive investment cycles typical for tech innovators but nonetheless emphasize high cash burn rates requiring careful liquidity stewardship despite sizeable cash buffers showcased as CAD ~17.3 million end-September 2025 balance sheet reserves alongside an exceptionally strong current ratio above twenty-two points indicating solid solvency fundamentals [F1][S9][S12].

Moreover, suspension of physical medical cannabis facility development strangles prospective downstream revenue avenues while potentially locking capital resources into deferred use cases [S1][S14]. Regulatory uncertainty around emergent sectors like medical cannabis introduces execution timing ambiguities complicating growth trajectory assumptions.

Upcoming Catalysts: Testing Milestones and Market Expansion Signals

Market participants should closely monitor outcomes from ongoing clinical-grade testing activities at Israel’s Weizmann Institute regarding Femto’s Cannabis CRM Platform which will validate technical robustness and potential calibration needs necessary before meaningful commercial rollout can proceed [S5][S13]. Successful validation could materially shift investor sentiment about user traction pathways within this emerging segment.

Complementarily, tracking registered user growth metrics or contract announcements related to their new Benefit CRM platform offers tangible insights into commercial-scale adoption versus early-stage trials. Any signs indicating improved retention rates or cross-selling opportunities would mark positive demand traction.

Development progress concerning the Sensera Device alongside patents prosecution status will illuminate R&D cycle velocity and integration potential between hardware-device data streams feeding FEMTO’s analytics stack—this could forge competitive differentiation through tech convergence effects [S6][S7].

Additional strategic alliances or acquisition endeavors targeting AI-enhanced service capabilities reflect management’s adaptation strategy amid rapid technological evolution reshaping enterprise SaaS landscapes; disclosures around these initiatives will be relevant execution touchpoints going forward [S7][S8].

Finally, given high concentration risk profiles investors should heed any shifts in client composition or diversification efforts disclosed in interim reports.

Supporting Financial Snapshot: Liquidity and Profitability Trends

Femto’s financial footing is reinforced by substantial cash balances totaling approximately CAD 17.3 million as of September 30, 2025 supplemented by total current assets near CAD 17.9 million while maintaining minimal current liabilities just over CAD 0.8 million yielding an extraordinary current ratio exceeding 22—indicative of excellent short-term liquidity coverage ratios although magnifying working capital tied-up relative to operations scale [F1].

The company reported a turnaround shifting from an operating net loss exceeding CAD -47 million in FY2024 into net income amounting to approximately CAD +12.9 million in FY2025—a significant margin improvement fueled by cost containment measures including reduced impairment charges along with increased professional fees supporting M&A activities reflecting accelerated portfolio refinement efforts [S1][S4].

Nonetheless operating cash flow remains negative at approximately -CAD9.5 million in FY2025 consistent with heavy reinvestment nature characteristic of pre-scale technology firms aiming at product pipeline expansion rather than dividend generation or capital returns currently [S15]. Capital raises through equity offerings totaling US$17 million earlier underscored funding adequacy sustaining near-term growth initiatives inclusive of developing the Sensera Device alongside core software enhancements [S3][S15]. Foreign exchange losses partially offset financial income generated predominantly through USD-denominated term deposit yields demonstrating active treasury management facing multi-currency challenges [S6][S20].

Overall balance-sheet robustness complements strategic priority realignment emphasizing scalable SaaS revenue streams; however sustaining positive profitability depends heavily on growing recurring revenues amidst concentrated client dynamics.

This analysis synthesizes Femto Technologies Inc.'s recent quarterly disclosures and annual filings up to April–May 2026 without conjecture beyond reported facts. It focuses on elucidating operational pivots toward specialized CRM solutions amid suspended ancillary projects while contextualizing financial health parameters relative to prevailing corporate strategy execution risks.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments