Five Point Holdings Accelerates Share Repurchase and Expands Asset Management Amid California Development Growth

Five Point Holdings reports robust early 2026 operational moves, leveraging portfolio diversification and capital structure improvements to sustain growth in California’s mixed-use communities.

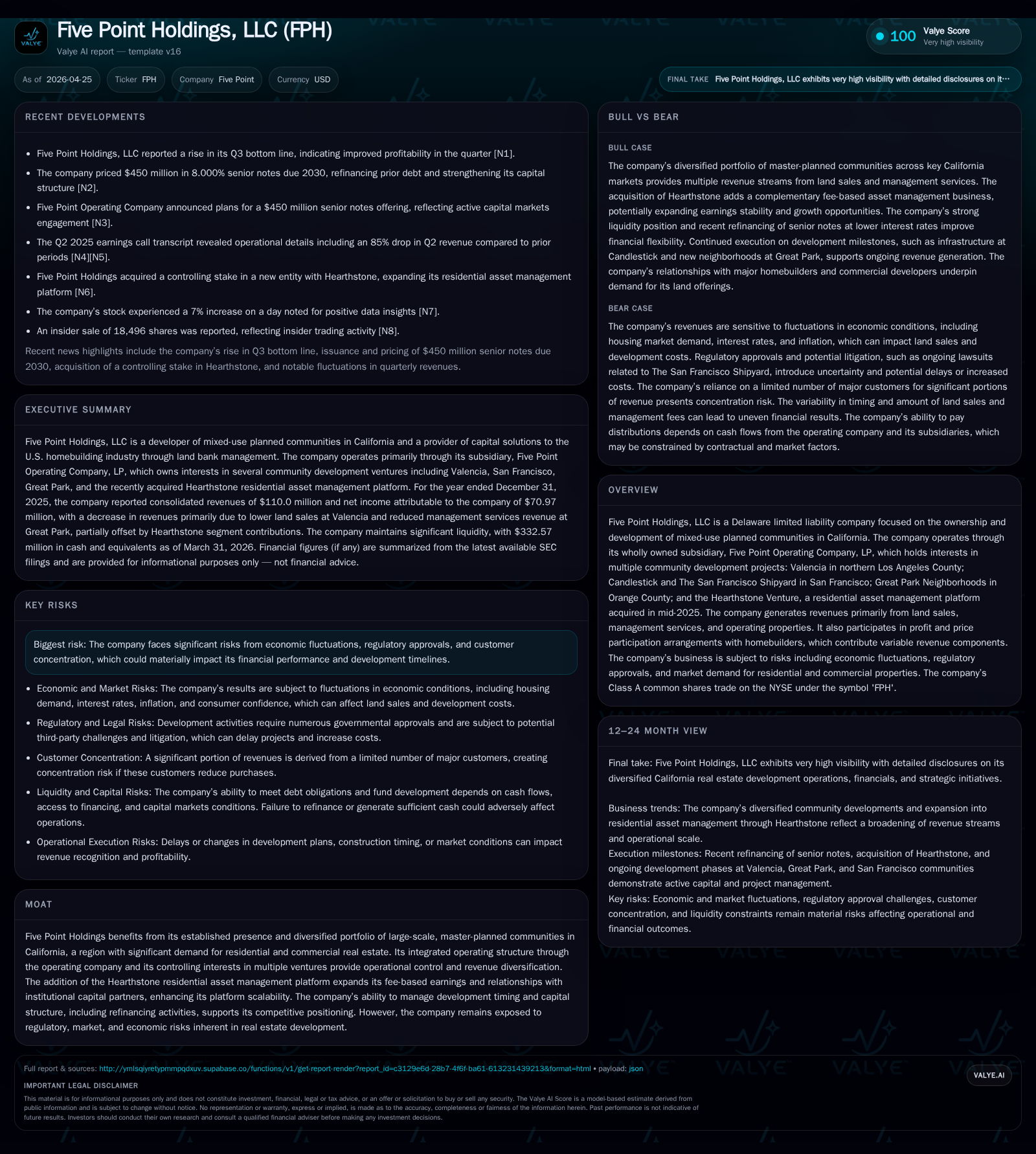

In its latest quarterly filing, Five Point Holdings, LLC has announced a $40 million share repurchase authorization complementing ongoing portfolio expansion. The company continues to advance its master-planned communities across key Californian markets, supported by the Hearthstone asset management platform acquired in mid-2025. While revenues declined year-over-year due to sales timing decisions, stable net income and solid operating cash flows underline resilience amid sector cyclicality. Strategic alignment with homebuilders and institutional partners solidifies its competitive position, though regulatory and economic sensitivities remain key risks.

Recent Operating Update

The latest quarterly filing dated April 24, 2026 (10-Q) surfaces critical near-term developments framing Five Point Holdings' operational trajectory. Notably, the Board sanctioned a share repurchase program capped at $40 million targeting Class A common shares, an active capital redeployment strategy signaling confidence in underlying asset value and future earnings potential [S3]. This initiative marks a shift towards enhanced shareholder return mechanisms after a period devoid of buybacks since the last annual report.

Operationally, Five Point continues methodical progress within its California master-planned developments. The company achieved a landmark industrial land sale within the Valencia community—a key northern Los Angeles County asset—realizing $42.5 million from a prime 13.8-acre parcel transaction, first significant since over 15 years prior [S1]. Conversely, residential land sales were selectively delayed to optimize pricing during market conditions, evidencing strategic inventory management rather than volume maximization.

The Hearthstone acquisition in July 2025 broadens Five Point's revenue base through its residential asset management platform managing land banking funds primarily focused on residential lot options. By extending into fee-based earnings alongside traditional land sales and management services, Five Point bolsters recurring revenue streams and institutional partner relationships—a move enhancing business durability through diversification [S1].

While FY 2025 revenues declined by about 54% year-over-year to roughly $110 million due principally to timing choices around land dispositions, net income grew moderately by nearly 4%, reaching approximately $71 million [F1]. Operating cash flow remains solid at over $105 million annually supporting liquidity needs for continued development work [F1]. The company's balance sheet reflects prudent refinancing actions including a new issuance of senior notes at an attractive fixed coupon rate coupled with an expanded revolving credit facility to underpin capital flexibility going forward; as of March 31, 2026 holdings include cash and equivalents of $332.6 million against total debt nearing $443.7 million indicating manageable leverage levels with a net debt around $111 million [F1].

Business Model and Strategic Positioning

Five Point's operating model pivots on owning and developing large-scale mixed-use communities predominantly situated across high-demand Californian regions where housing supply deficits remain acute. Through its wholly owned subsidiary Five Point Operating Company LP, it manages pivotal projects such as Valencia (LA County), Candlestick and The San Francisco Shipyard (San Francisco), Great Park Neighborhoods (Orange County), along with the Hearthstone platform that enhances its capital solutions offerings for homebuilders.

Revenue generation is multifaceted: primary contributors include upfront land sales — both commercial and residential — augmented by participation agreements that entitle Five Point to variable profit or price participation payments linked to homebuilder performance post-sale; further supplemented by development management services fees especially associated with the Great Park Venture [S1][F1]. This structure allows partial decoupling from raw transaction volume swings by layering incentive-aligned compensation mechanisms.

In recent years, Five Point has calibrated its residential parcel release strategy judiciously to align supply availability with evolving market absorption trends rather than maximizing immediate turnover—an approach reflecting matured discipline given the cyclical sensitivities in real estate demand dynamics. Moreover, adding Hearthstone expands capability into lot option fund asset management—tying Five Point closer to institutional capital inflows servicing homebuilding activity and providing more recurring revenue features.

Homebuilding partnerships are integral to revenue realization and operational success; guest builders operate on developed sites selling finished homes while Five Point captures upstream value through lot sales plus variable participation arrangements that increase proportionally with housing prices or builder profitability gains [S1][S19]. This symbiotic setup anchors solid customer retention prospects but also introduces concentration risk due to material reliance on select builders as major customers.

Industry Structure and Competitive Position

The single-family housing development sector in California operates in an environment shaped by constrained land supply due to zoning restrictions, environmental regulations, infrastructure costs, and growing demand driven by population growth and affordability gaps. Five Point's focus on large-scale master-planned communities affords operational scale advantages allowing phased development over multi-year horizons thereby smoothing capacity utilization and amortizing fixed overheads.

Competition comes from both regional homebuilders with vertically integrated development arms as well as standalone land developers who may lack comparable portfolio scales or diversified geographical exposure within California’s diverse submarkets. Five Point’s established foothold across multiple major metro areas offers relative insulation from localized downturns or regulatory delays.

Additionally, integrating residential asset management via Hearthstone places Five Point at an intersection between development and finance — bridging capital providers seeking exposure to California housing markets with homebuilders requiring sophisticated lot banking solutions. This convergence creates differentiation potential compared to peers reliant solely on asset flipping or pure fee models.

Nevertheless, regulatory complexities including permitting timelines, environmental litigation risks (e.g., ongoing legal proceedings related to contaminated parcels at San Francisco Shipyard), water usage agreements (notably under long-term contracts highly relevant given California’s variable hydrological conditions), and rising construction costs impose persistent developmental headwinds [S1][S12]. These factors collectively form structural growth constraints despite strong demand fundamentals.

Growth Drivers and Constraints

Drivers:

- Continued scarcity of developed land parcels suitable for residential/commercial projects in urban/suburban California drives sustained long-term pricing power.

- Enhanced fee-based revenue streams from Hearthstone strengthen revenue predictability even amid cyclical slowdowns.

- Strategic coordination with homebuilders increases velocity of developed land monetization via profit/price participation enhancements.

- Strong liquidity position enables timely investments into horizontal development accelerating staged community build-out progressively capturing market demand.

- Repurchase program signals confidence leveraging firm’s intrinsic value potentially reinforcing equity market perception enhancing access to capital if needed.

Constraints:

- Protracted regulatory approval processes remain uncertain impacting project timelines especially environmentally sensitive sites such as those formerly military controlled near San Francisco Shipyard.

- Homebuilder customer concentration risk exposes earnings variability tied to their business cycles and capital availability.

- Macroeconomic variables including interest rate fluctuations affect mortgage affordability which underlies buyer demand impacting downstream lot absorption rates.

- Highly competitive California real estate market imposes continual innovation requirement on community design/features influencing attractiveness versus alternatives.

- Capital intensity inherent in horizontal infrastructure investments necessitates balanced capital planning amid fluctuating funding cost environments limiting aggressive expansion without sufficient returns visibility.

What To Watch Next

Key forthcoming milestones that will elucidate Five Point’s path forward include:

- Execution pace for new neighborhood launches within Great Park and continued phases upsell signaling momentum in product absorption.

- Further progress on commercial/institutional leasing or disposition activities inside Valencia's industrial/commercial parcels beyond recent notable sale.

- Performance metrics from Hearthstone’s lot option funds including co-investment outcomes revealing stability/duration of fee income contribution.

- Updates on resolution or progress regarding legacy environmental litigation affecting property delivery schedules at San Francisco Shipyard which influence asset monetization timing.

- Quarterly updates pertaining to share repurchase activity pace serving as indicative gauge of management’s risk tolerance and balance sheet prioritization strategy going into late 2026.

- Guidance revisions explicitly addressing anticipated sales cadence changes aligned with broader housing market condition forecasts if provided in upcoming filings/press releases.

Financial Profile Summary

Historical performance (annual)

|

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 110 | 71 | 105 | 217000 | -53.8% | +3.9% |

| 2024 | 238 | 68 | 116 | 808000 | +12.4% | +23.3% |

| 2023 | 212 | 55 | 154 | 23000 | +395.9% | +459.6% |

| 2022 | 43 | -15 | -188 | 75000 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

|

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 105 | 3.1 |

| 2024 | 115 | 3.2 |

| 2023 | 154 | 2.8 |

| 2022 | -188 | -0.8 |

Source: SEC companyfacts cache [F1].

Financial data underpinning Five Point’s operating narrative reflect selective sales timing producing sharp headline revenue contraction offset by margin stability and improved operational cash generation:

|

| FY | Revenue ($mil) | Net Income ($mil) | CFO ($mil) | Capex ($thous) | Equity ($bil) | Rev YoY % | Net Income YoY % | CFO YoY % | Capex YoY % |

|---|---|---|---|---|---|---|---|---|---|

| 2025 | 110 | 70 | 105 | 217 | 2.32 | -53.8% | +3.9% | -9.3% | -73.1% |

Liquidity remains robust with approximately $333 million cash reserves against total debt near $444 million as March quarter closed highlighting manageable leverage levels exemplified by net debt standing close to $111 million—a metric supportive of planned share repurchases without constraint [F1]. Interest coverage stability anchored by refinanced senior notes yielding lower coupon rates reduces stress from interest cost volatility risks amidst fluctuating macro conditions [S4–S11].

Broadly speaking, the financial profile underscores a transitional phase balancing prudent cash deployment across expanding project phases while maintaining disciplined capital stewardship manifested through refinancing gains and cautious buyback activism post-lull in distributable share purchases during prior years.

Disclaimer

This analysis is provided solely for informational purposes reflecting publicly available data up through April 25, 2026. It does not constitute investment advice or recommendations regarding securities mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments