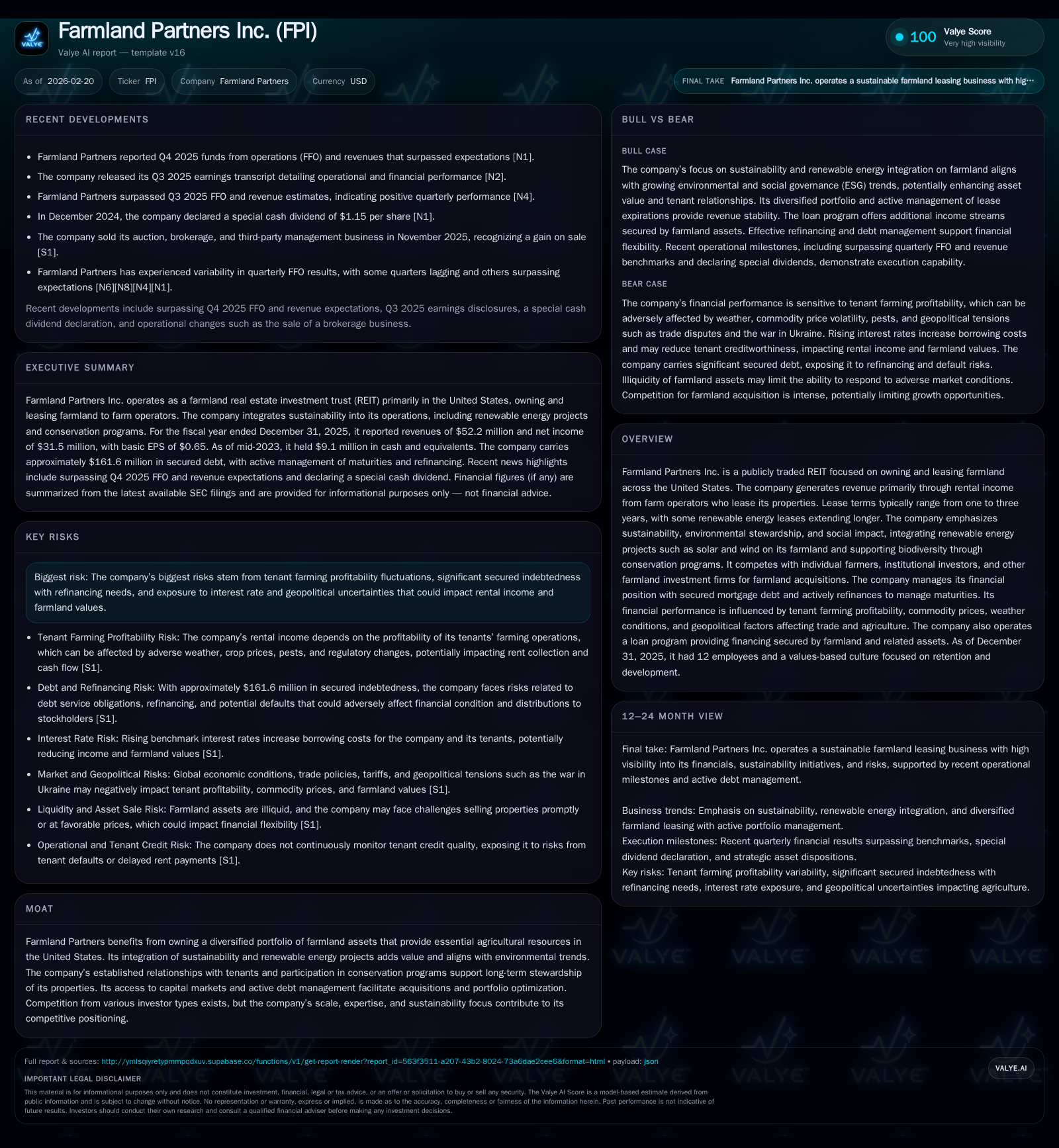

Farmland Partners Navigates Strong Revenue Growth Amid Refinancing and Tenant Profitability Challenges

FPI leverages a diversified U.S. farmland portfolio and sustainability initiatives to support revenue growth, while actively managing capital structure and tenant risks in a complex agricultural market environment.

Farmland Partners Inc. (FPI), a REIT focused on owning and leasing U.S. farmland, reported significant revenue growth in 2025 driven by farmland value appreciation and elevated rental rates linked to strong commodity prices. Despite this top-line expansion, net income declined due to lower gains on asset sales and impairment charges from portfolio optimization. Operating cash flow improved modestly, supporting increased dividend distributions and share repurchases, balanced against ongoing mortgage debt refinancing in a high interest rate environment. Sustainability efforts including renewable energy leases and conservation programs contribute to diversified revenue streams and ESG integration. Key drivers of future performance include tenant profitability under volatile commodity markets, competitive pressures in farmland acquisition, and refinancing execution. Risks encompass tenant defaults, farmland valuation fluctuations, and regulatory uncertainties impacting agricultural operations.

Company Overview and Historical Performance

Farmland Partners Inc. (NYSE: FPI) is a publicly traded real estate investment trust specializing in acquiring, owning, and leasing high-quality farmland across multiple U.S. regions. The company derives most of its revenue from rents paid by tenant farmers under leases typically spanning one to three years; some leases also support renewable energy installations.

The business benefits from secular trends such as rising global food demand driven by population growth and increasing GDP per capita—especially in developing economies—leading to persistent land value appreciation that supports tenant profitability and stable rent collections [S1].

From FY2022 through FY2025, FPI has demonstrated substantial revenue growth primarily fueled by acquisitions combined with upward pressure on lease rates linked to commodity price strength. However, net income has shown volatility due to non-operating factors including gains or losses on asset disposals as well as impairments related to portfolio optimization decisions.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | Capex ($) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 52 | 32 | 17 | 23000 | +143.0% | -47.3% |

| 2024 | 21 | 60 | 16 | 253000 | -0.5% | +93.8% |

| 2023 | 22 | 31 | 13 | 275000 | -1.1% | +164.8% |

| 2022 | 22 | 12 | 17 | 853000 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): OpInc, ROE%. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 64 | 38 | 17 |

| 2024 | 22 | 28 | 16 |

| 2023 | 12 | 72 | 13 |

| 2022 | 11 | 16 |

Source: SEC companyfacts cache [F1].

Note: Operating income data not available for the latest years; capex figures represent capital expenditures incurred but not yet paid.

Drivers of Historical Growth

The sharp increase in revenue during FY2025 reflects higher rental rates aligned with inflationary pressures on agricultural inputs coupled with strong commodity prices improving tenant profitability [S1]. Strategic property dispositions generated realized gains of approximately $10.5 million primarily from Corn Belt assets sold during the year [S16]. These transactions facilitated portfolio optimization while providing liquidity.

Operating cash flow grew moderately year-over-year due to stable rent collections despite lower gains on dispositions relative to prior years; net income contraction was influenced by impairments on select assets no longer meeting investment criteria [F1][S26].

Future Growth Prospects

Looking forward, Farmland Partners expects sustained global food demand growth driven by population increases and rising income levels that shift dietary patterns towards higher consumption of animal-based proteins—thereby increasing feed crop demand such as corn and soybeans [S1]. Renewable energy leasing presents an expanding diversification avenue; existing solar projects across ten farms generate roughly 207 megawatts of clean energy capacity with options on additional properties for future installations [S1].

However, growth could be constrained by several factors:

- Elevated interest rates increase borrowing costs for both FPI refinancing activities and tenant farmers reliant on debt financing for operational cycles, potentially pressuring rent payments [S6][S23].

- Intensifying competition for farmland includes individual farmers alongside large institutional investors such as Nuveen Natural Capital and Gladstone Land; scale advantages are critical but may compress acquisition yields over time [S1][S9].

- Weather-related risks like droughts or floods can disrupt crop production impacting tenant solvency; federal program uncertainties arising from USDA funding lapses add operational challenges [S2].

Capital Structure and Refinancing Activity

As of December 31, 2025, Farmland Partners held approximately $161.6 million in mortgage indebtedness secured by its farmland portfolio excluding issuance costs [S15]. The company faced $68.3 million in debt maturities within the next twelve months but proactively refinanced or redeemed about $68 million during late 2025/early 2026; approximately $67 million remains under active refinancing negotiations demonstrating ongoing capital market access despite a challenging interest rate environment [S4][S16].

Debt agreements contain covenants restricting additional indebtedness beyond agreed thresholds as well as limiting certain corporate actions including asset sales or distributions that could impact financial flexibility [S6]. Interest rate swaps are employed selectively to mitigate exposure from floating-rate debt components.

Capital Allocation Priorities

REIT distribution requirements mandate paying out at least 90% of taxable income annually; accordingly, dividends surged nearly threefold from $21.6 million in FY2024 to $63.7 million in FY2025 despite earnings volatility [F1][S26]. Share repurchases totaled $37.8 million during FY2025 reflecting management confidence in intrinsic value when shares trade attractively.

Acquisition activity slowed markedly with only about $7.3 million spent during FY2025 compared with prior periods indicating disciplined capital deployment amid elevated market prices for farmland assets [F1][S10].

Sustainability Integration & ESG Initiatives

Environmental stewardship is embedded within FPI’s business model through biodiversity initiatives such as enrollment in USDA Conservation Reserve Program (CRP) acres which remove marginal lands from production temporarily while improving soil health and wildlife habitat [S1]. This supports social impact objectives by fostering rural economic activity.

Renewable energy leases represent a growing segment contributing non-agricultural rental income estimated above $1 million annually while aligning with investor ESG preferences through green energy generation from solar arrays deployed across leased farms [S26].

Risks & Uncertainties

Material risks include:

- Tenant credit risk heightened by cyclical agricultural economics; defaults or bankruptcies could impair rental income requiring legal remedies or foreclosures that may affect property values negatively [S14][S27].

- Interest rate volatility poses ongoing challenges increasing borrowing costs which could constrain refinancing options given sensitivity of farmland valuations to discount rates indirectly influenced by macroeconomic conditions.

- Geopolitical events such as the war in Ukraine affect fertilizer supply chains but FPI tenants largely source inputs domestically mitigating direct exposure somewhat [S1][S23].

- Litigation related to alleged stock manipulation has been a distraction though no material liabilities have been recorded currently associated with these matters [S9][S21].

Milestones & Monitoring Points

Key areas for investor attention include:

- Completion of refinancing efforts addressing remaining near-term debt maturities.

- Tenant rent renewal trends relative to commodity price movements.

- Acquisition or disposition activity signaling strategic portfolio adjustments.

- Progression of renewable energy project pipeline expansions enhancing revenue diversification.

- Regulatory changes impacting USDA programs or sustainable farming practices influencing operational fundamentals.

Conclusion

Farmland Partners maintains a geographically diversified core portfolio generating steady rental income complemented by sustainability-driven supplementary revenues from conservation programs and renewable energy projects adding optionality. While near-term prospects face headwinds from monetary tightening affecting borrower affordability alongside intensifying competition compressing acquisition yields, long-term fundamentals rooted in global food demand growth underpin structural scarcity supporting land values. Management’s balanced approach toward distributing cash flows through dividends and buybacks alongside cautious acquisition spending reflects alignment with shareholder interests amid evolving market dynamics. Vigilance regarding tenant credit quality remains essential given the yield-sensitive nature of the business model within an uncertain macroeconomic environment.

This analysis relies exclusively on publicly available SEC filings and news sources without any speculative forecasting or proprietary information.Farmland Partners’ actual future results may be affected by unforeseen developments beyond those discussed herein.This report does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments