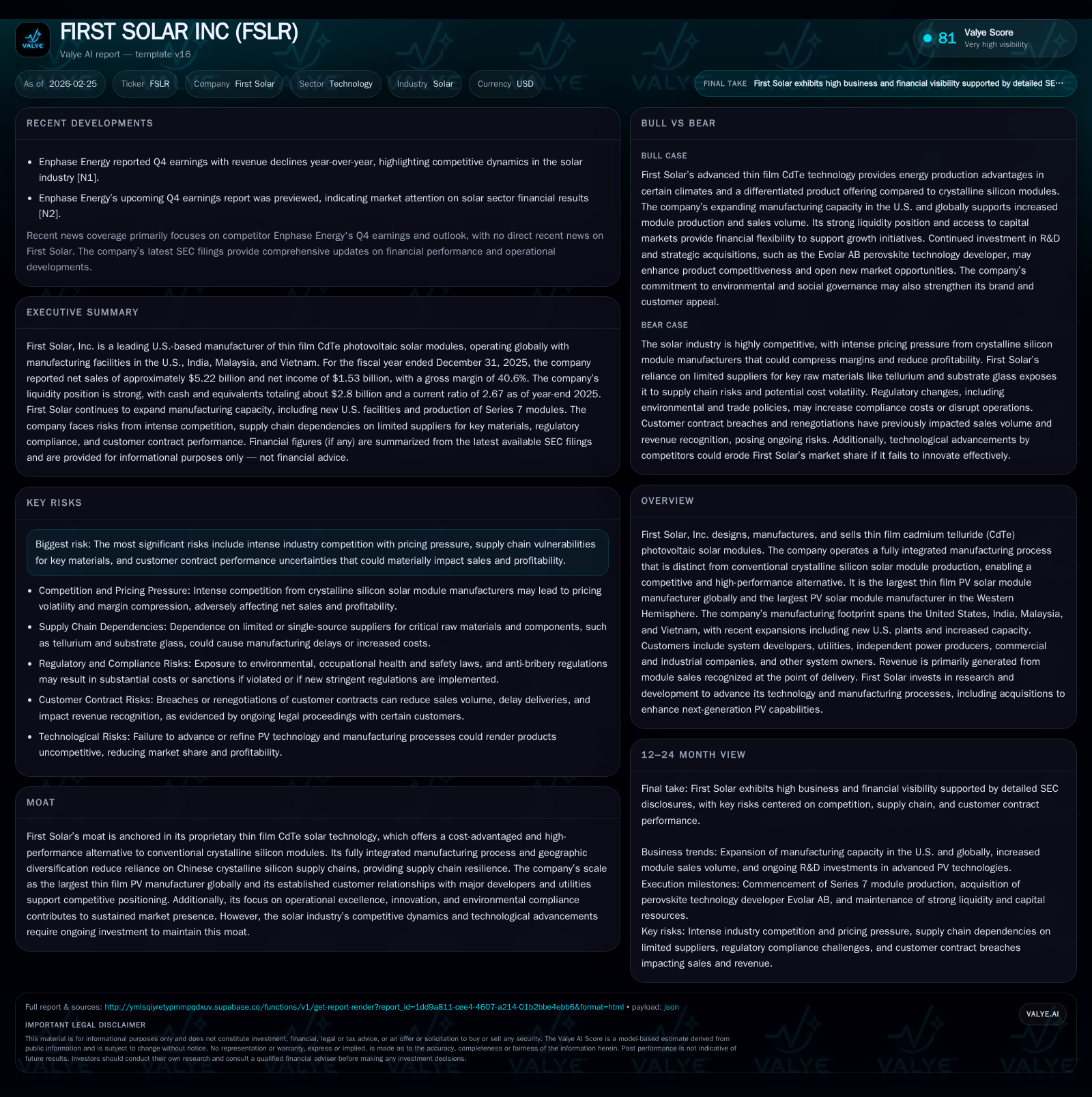

First Solar’s Expansion and Patent Litigation Shape Growth and Margins Pressure

First Solar maintains growth momentum driven by U.S. manufacturing scale-up amid intensified patent disputes and pricing competition.

First Solar Inc. posted robust revenue growth in 2025 on the back of expanding manufacturing capacity primarily in the U.S., leveraging its proprietary CdTe thin film technology, which differentiates it from crystalline silicon competitors. However, emerging risks include ongoing patent litigations concerning TOPCon technology and pricing pressures in global markets influenced by supply-demand imbalances and trade barriers. Capital expenditures are moderating after a heavy 2024 investment cycle, with solid cash flow generation supporting organic growth plans and R&D while no dividend or buyback data was disclosed. Monitoring contract dispute outcomes and cost management effectiveness will be critical going forward.

Historical Performance: Strong Growth Amid Capacity Expansion

First Solar's revenue increased sharply over the past four years, rising from approximately $2.62 billion in 2022 to $5.22 billion in 2025—a compound annual growth trend boosted by an aggressive expansion of its thin-film CdTe solar module production capacity particularly in the United States. Revenue grew by about 24.1% in 2025 compared to the prior year [F1]. The firm's operating income followed suit, moving from a modest loss of $27 million in 2022 to an operating profit of roughly $1.60 billion in 2025, reflecting successful scaling but some margin pressures as indicated by a fall in gross margin percentage from historical peak levels [F1][S6]. Net income similarly advanced from a negative base (-$44 million) in 2022 to over $1.53 billion in reported earnings for 2025—corresponding roughly to a trailing ROE near 16%, signaling effective capital utilization amid expansion investments.

The company also evidenced strong operational cash flows that nearly doubled between 2023 and 2025 ($603 million to $2.06 billion), supporting significant capital spending yet maintaining positive free cash flow estimated at around $1.19 billion for 2025 ([F1]; calculated as CFO minus Capex). Capital expenditures peaked in 2024 at approximately $1.53 billion but were scaled back substantially (down nearly 43%) to $870 million in the latest reported year as major new plants moved into production phases [F1][S17].

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($bn) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5.2 | 1528 | 2.1 | 1597 | +24.1% | +18.3% |

| 2024 | 4.2 | 1292 | 1.2 | 1394 | +26.7% | +55.5% |

| 2023 | 3.3 | 831 | 0.6 | 857 | +26.7% | +1981.0% |

| 2022 | 2.6 | -44 | 0.9 | -27 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div, Buybacks. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 1187 | 16.0 |

| 2024 | -308 | 16.2 |

| 2023 | -785 | 12.4 |

| 2022 | -30 | -0.8 |

Source: SEC companyfacts cache [F1].

- Approximate based on available data; **negative prior periods

Note: Dividend payout and share repurchase data are not available for the periods referenced.

Future Growth Drivers and Constraints

First Solar’s future growth prospects largely hinge on scaling its differentiated thin-film CdTe photovoltaic solar modules, where it enjoys competitive advantages over conventional crystalline silicon technology through lower material intensity and established manufacturing integration [S23]. The company is actively expanding domestic manufacturing footprints with multiple new U.S.-based plants completed recently, plus plans for a sixth facility expected online by late 2026, supported partly by incentives under the Inflation Reduction Act (IRA) and related tax credits such as Section 45X production credits [S17].

Backlog volume remains strong with module sales contracts covering around 50 GW valued at $15 billion extendable up to around mid-decade horizon including price adjustments reflecting anticipated technology improvements [S27]. This portfolio spans primarily utility-scale developers, independent power producers, utilities, and corporate buyers predominantly located in the U.S., which mitigates currency exposure since revenues are mostly USD-denominated.

Despite these tailwinds, growth is tempered by ongoing risks: intense global competition keeps module pricing volatile, notably as Asian manufacturers—with substantial crystalline silicon module capacity—operate near or below cost levels mainly targeting European markets [S28]. Indian market access limitations further reduce international deployment opportunities for First Solar’s Southeast Asian production units forcing strategic shifts toward more localized U.S operations.

Additionally, patent litigation surrounding TOPCon technology—a competing high-efficiency solar cell type—is actively contested by First Solar through multiple lawsuits against industry players including JinkoSolar, Canadian Solar, and others with claims filed at both district courts and the US International Trade Commission (USITC) seeking exclusion orders that could shape market access dynamics [S14][S25][S26]. These legal challenges pose cost risks as well as potential disruptions depending on rulings.

Supply chain resilience remains enhanced relative to peers given First Solar’s low dependence on polysilicon feedstock (avoiding regions like China’s Xinjiang) combined with geographically diversified assembly facilities across the U.S., India, Malaysia, and Vietnam [S1], but scarcity or pricing shifts in key materials like tellurium or substrate glass remain potential vulnerabilities.

Forecasts / Expectations & What To Watch

While explicit forward financial guidance was not detailed in recent disclosures or earnings calls available as of early ’26 [N2], key indicators for investors include:

- Progress updates on commissioning of new U.S manufacturing plants including the announced sixth facility slated for second half of ’26.

- Outcomes of ongoing patent infringement litigations—especially those before USITC—as they can materially impact competitive positioning and licensing exposure.

- Pricing trends across key export markets especially Europe where overcapacity issues persist.

- Contract renewals or disputes resolution involving major customers such as BP Solar Holding where breach suits have been filed seeking ~$384M payments with significant counterclaims under litigation until mid-2026 ruling expected [S9][S10].

- Impact assessments relating to potential supply chain disruptions or raw material price volatility.

- Execution effectiveness on module performance improvements tied to next-generation Series technologies influencing revenue adjustment opportunities within existing contracts [S27][S13].

Returns & Capital Allocation Summary

First Solar reported a strong net income of about $1.53 billion for FY25 with operating margins remaining robust at approximately 30%. The cash flow profile is healthy with operating cash flows exceeding two billion dollars facilitated by improved working capital management including advance customer payments and factoring trade receivables [F1][S21]. Capital expenditure spending moderated after a peak installation phase supporting rapid capacity growth; planned capex remains sizable ($0.8-$1 billion forecasted for ’26) focused on scaling domestic production capability alongside R&D investments centered around further cost reductions and efficiency gains of their CdTe modules [S17].

The company has accumulated cash reserves totaling nearly $2.8 billion alongside a healthy current ratio (~2.67x), providing liquidity adequacy for near-term operational needs without reliance on external debt financing given undrawn credit facilities recently upsized to $1.5 billion from previously unused $1 billion line [F1][S22][S8]. No dividend payouts or stock buyback programs are disclosed within recent filings suggesting retained earnings reinvested into growth initiatives rather than shareholder distributions.

Industry Context: Thin Film Versus Crystalline Silicon Dynamics

From a sector standpoint (analysis), First Solar's CdTe thin film modules offer several intrinsic advantages including lower semiconductor material consumption (only ~2-3% compared to crystalline silicon modules), allowing for costs less correlated with fluctuating polysilicon prices which have historically exhibited volatility due to geopolitical factors such as trade embargoes relating to Xinjiang region polysilicon supply restrictions imposed by legislation like the Uyghur Forced Labor Prevention Act [S1]. The shorter energy payback period and competitive temperature coefficient also provide real-world performance benefits that alleviate some efficiency perception drawbacks traditionally associated with thin-film technologies.

However, crystalline silicon remains dominant globally with rapid innovation trends like bifacial cells and TOPCon passivation layers driving efficiency gains potentially challenging First Solar’s market share if technological leadership falters or if pricing pressure intensifies beyond sustainable margins.

Conclusion

First Solar demonstrates a compelling growth trajectory fueled by its proprietary CdTe module technology and deliberate capacity expansion predominantly centered on reshoring production within the United States under current favorable policy frameworks like the IRA tax incentives program.

Nevertheless, key execution risks remain tied to managing competitive pricing pressures exacerbated by global oversupply conditions, navigating complex patent litigation battles which could reshape product offerings or licensing fees materially impacting profitability, continuing innovation pace against evolving crystalline silicon tech enhancements, resolving substantial customer contract disputes potentially affecting near-term revenue recognition visibility, alongside mitigating supply chain constraints particularly related to specialized raw materials.

Decision-makers should carefully monitor legal developments around intellectual property claims scheduled into mid-2026 court rulings alongside margin trends amid challenging industry-wide pricing environments while tracking capital expenditure discipline necessary to underpin sustainable long-run returns without over-leverage.

Disclaimer: This analysis is provided solely for informational purposes without offering investment advice or recommendations regarding First Solar Inc.’s securities.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments