Fiverr Expands Value-Added Services as Marketplace Growth Faces Macroeconomic Challenges

Fiverr International Ltd. reported modest revenue growth in 2025 driven by service offerings despite declining marketplace volume and active buyers.

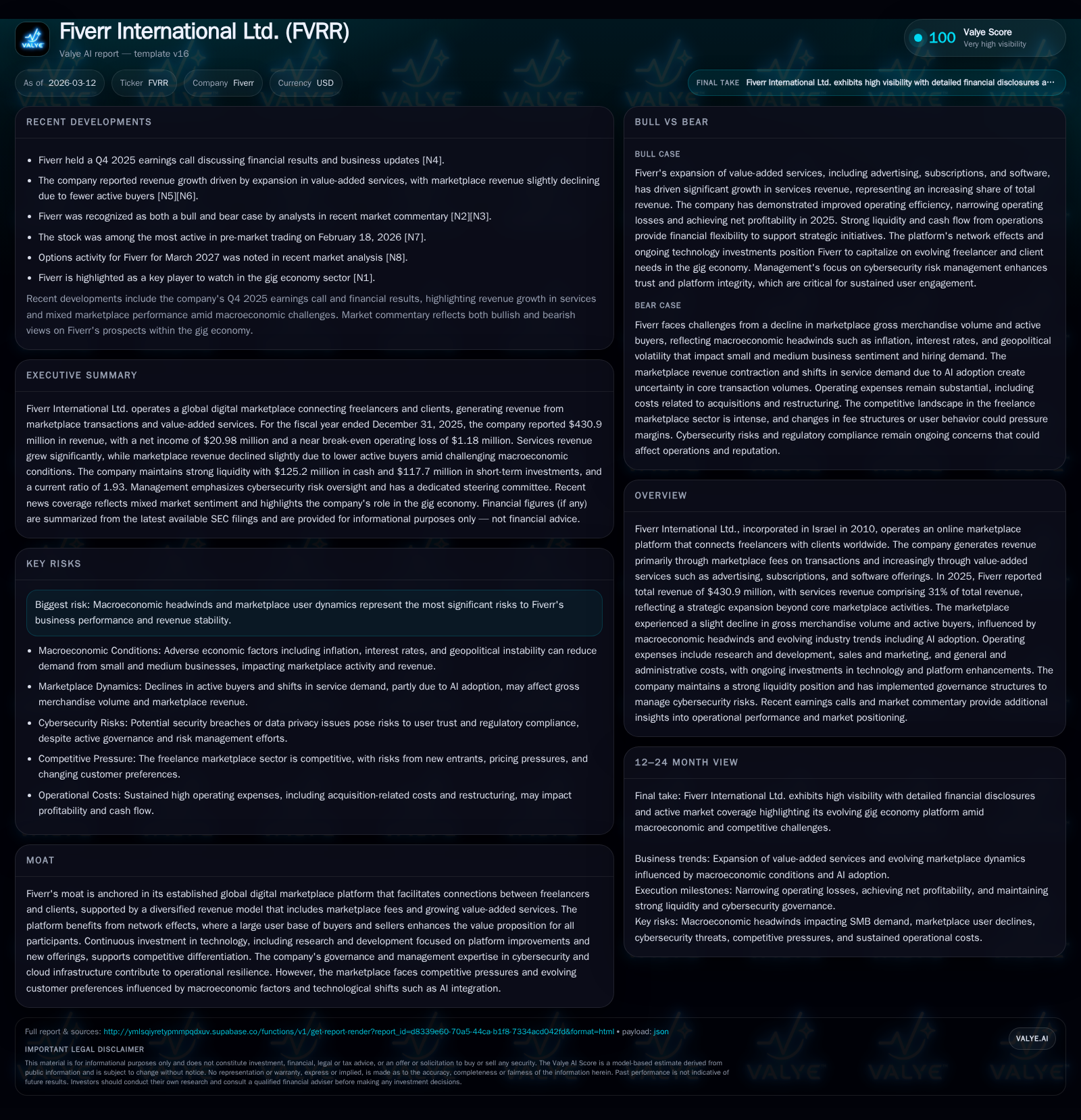

Fiverr International Ltd., a global online freelance marketplace, increased revenue by 10.1% in 2025 to $430.9 million, fueled by a 50.9% surge in services revenue representing value-added offerings. However, its core marketplace revenue dropped 1.8%, reflecting a 2.2% decline in gross merchandise volume (GMV) and a 13.6% fall in active buyers, offset partially by increased spend per buyer. Operating loss narrowed substantially, supported by disciplined expense management and strong cash flow generation, enabling continued share repurchases albeit at a reduced pace compared to the prior year. The firm is leveraging technology investments, including AI integration and enhanced cybersecurity governance, to augment platform competitiveness amid evolving macroeconomic and industry dynamics.

Business Overview

Fiverr International Ltd., an Israel-incorporated company founded in 2010, operates a digital marketplace that connects freelancers globally with clients seeking diverse services across categories.

Historically centered on facilitating gig transactions through marketplace fees, Fiverr has expanded its business model to emphasize value-added services including advertising platforms, subscription-based offerings, and proprietary software solutions aimed at increasing user engagement and monetization avenues [S1]. This strategic shift has been motivated by the need to diversify revenue streams amidst competitive pressures and changing market dynamics.

Historical Financial Performance

Over the past four years (2022–2025), Fiverr has delivered consistent top-line growth but faced margin pressures impacted by investments and macro factors:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 431 | 21 | 105 | -1 | +10.1% | +15.0% |

| 2024 | 391 | 18 | 83 | -16 | +8.3% | +395.7% |

| 2023 | 361 | 4 | 83 | -15 | +7.1% | +105.1% |

| 2022 | 337 | -71 | 30 | -75 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 33 | 104 | 5.1 |

| 2024 | 100 | 82 | 5.0 |

| 2023 | 82 | 1.0 | |

| 2022 | 29 | -26.9 |

Source: SEC companyfacts cache [F1].

Source: [F1]

Key observations include:

- Revenue grew steadily at a CAGR above industry gig economy averages, reflecting both organic growth and portfolio diversification.

- Operating losses narrowed markedly from large losses in early years to near break-even in the latest fiscal year.

- Net income swung positive since the fiscal year ended December 31, 2023.

- Strong operating cash flows sustained despite sustained capex investment focused on technology infrastructure.

- Share repurchase programs have been sizable but more cautious recently, indicating balanced capital deployment strategies.

Revenue Composition and Business Drivers

Revenue for FY2025 totaled approximately $430.9 million, a rise of around $39 million (+10%) versus FY2024 led primarily by value-added services increased revenues that rose ~50.9% to $133 million or about one-third of total sales [S1].

In contrast, marketplace revenue declined modestly by about -1.8% to roughly $297 million reflecting downward pressure on Gross Merchandise Volume (GMV), which dipped approximately -2.2% year-over-year to $1,073 million [S1]. The GMV decline correlates with decreased annual active buyers (-13.6%) despite a compensating increase in average annual spend per buyer (+13.3%).

This shift may be interpreted as customer base contraction but heightened engagement or purchase intensity among remaining buyers — a phenomenon likely influenced by macroeconomic stress on SMBs coupled with evolving demand for higher skill-level offerings versus commoditized tasks potentially displaced or augmented by AI technologies [S16].

Cost Structure and Operating Expenses

Cost of revenue increased ~12%, principally owing to intangible amortization related to acquisitions/internal software capitalization (+$4M), contractors’ services (+$3.6M), hosting costs (+$1.6M) plus processing fees (+$0.6M) [S16]. These were partially offset by reduced employee-related expenses.

Operating expenses remained substantial though relatively stable with:

- Research & Development costs rising marginally (~0.5%) reaching about $91 million or ~21% of revenue as Fiverr intensifies investment in new product capabilities [S16].

- Sales & Marketing spending increased about +3%, largely driven by marketing campaigns plus impairment charges for certain discontinued activities totaling around ~$14M net adjustments offsetting lower personnel costs [S16].

- General & Administrative expenses grew

14%, notably due to acquisition-related costs including changes in contingent consideration fair values impacting the period accounting ($12M increase), alongside heightened fraud prevention and legal expenses [S16].

Despite these outlays, total operating loss narrowed dramatically from nearly -$16M in FY2024 to under -$1.2M in FY2025 reflecting operational leverage gains [S1].

Profitability Metrics & Capital Returns

Net income improved ~15% year-over-year hitting nearly $21M with an approximate return on equity of about 5% based on year-end equity balances exceeding $410 million [F1]. This profitability recovery signals effective cost containment alongside elevating revenues from new service lines.

Operating cash flow accelerated 26% compared to prior year reaching over $104M underpinning robust liquidity management [F1]. After moderate capital expenditures ($0.65M), Fiverr achieved substantial free cash flow near $104 million supporting balance sheet strength.

Share repurchases totaled around $32 million in FY2025 versus over $100 million the prior year suggesting more selective capital deployment possibly balancing returning capital to shareholders against funding innovation efforts amid uncertain external conditions [F1][S24]. No dividends have been reported.

Liquidity and Capital Structure

The company remains well-capitalized with cash equivalents of about $125 million as of December end-2025 backed by working capital around $232 million yielding a current ratio near two times [F1][S3–S4]. Contingent obligations related to acquisitions are managed prudently through regular fair value reassessments.

Notably, repayment of convertible notes matured November 2025 eliminated significant debt liabilities enhancing financial flexibility [S6][S7]. Ongoing access to investment-grade marketable securities aids cash management.

Strategic Positioning & Moat Analysis

Fiverr's competitive advantage lies chiefly in its established global digital marketplace encompassing millions of freelancers and client segments worldwide enabled by network effects amplifying value as participation scales . Diversification into value-added services including advertising sales, subscription models for premium features, and proprietary SaaS products broadens monetization vectors beyond pure transaction fees.

Investment focus remains on enhancing the platform experience via continuous R&D spending supporting AI-enhanced matching algorithms, workflow automation tools, and security architectures powered by seasoned cybersecurity leadership embedded within senior management oversight committees ensuring resilience against rising cyber threats [S20][S19]. Meaningful delineation between simple low-skill gigs replaced or optimized through AI vs complex high-skilled engagements informs product design cycles anticipated to reshape supply-side dynamics.

Market Risks & Industry Context

The company cites macroeconomic headwinds—persistent inflationary pressures, sharply higher interest rates disrupting SMB confidence—and geopolitical market uncertainties as primary constraints affecting buyer behaviors on the platform suppressing recruitment needs causing buyer attrition creating near-term headwinds [S16][S17].

Simultaneously, rapid adoption of AI creates bifurcated trends necessitating agile adaptation: commoditized tasks may decline while demand surges for creative or specialized professional services resistant to automation requiring differentiated platform handling.

Future Growth Prospects & Investor Considerations (Analysis)

At present no explicit public financial guidance exists beyond FY2025 results; however, key areas warrant monitoring:

- Expansion pace of high-margin services lines that currently constitute almost a third of total revenue yet significantly outgrow core marketplace volumes remains critical for sustained topline momentum.

- Stabilization or reversal of active buyer attrition would suggest improved market traction especially if general economic conditions stabilize.

- Productivity gains from ongoing AI integrations could reshape unit economics favorably if realized effectively within the next several quarters.

- Continued discipline balancing marketing spend efficiency without sacrificing brand visibility during volatile demand environments.

- Execution against strategic cost controls while investing sufficiently in technology innovation including cybersecurity safeguards critical for trust retention amid increasing regulatory scrutiny [S20].[N1],[N3]

With ample cash reserves and scalable infrastructure investments underway complemented by prudent capital allocation practices Fiverr appears positioned cautiously yet favorably relative to peers within the growing gig economy ecosystem [N8],[N10].

Conclusion

Fiverr International Ltd.’s fiscal trajectory through year-end December 31, 2025 paints a company transitioning from pure marketplace dependency toward enriched service-driven growing revenue streams amidst macroeconomic turbulence constraining transactional volumes.[F1][N1] Realignment efforts through measured cost control helped trim operating losses nearly entirely while delivering positive bottom-line earnings supported by strong operating cash conversion.[F1]

Navigating evolving skill demand dichotomies driven by intensified AI usage among freelancers will require continuous product innovation underpinned by solid cybersecurity governance frameworks ensuring platform integrity.[S20] How efficiently Fiverr scales its complementary services balanced against marketplace shrinkage will determine medium-term growth sustainability going forward.

Disclaimer: This analysis is based solely on publicly available information as of March 12, 2026, including SEC filings and recent news transcripts; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments