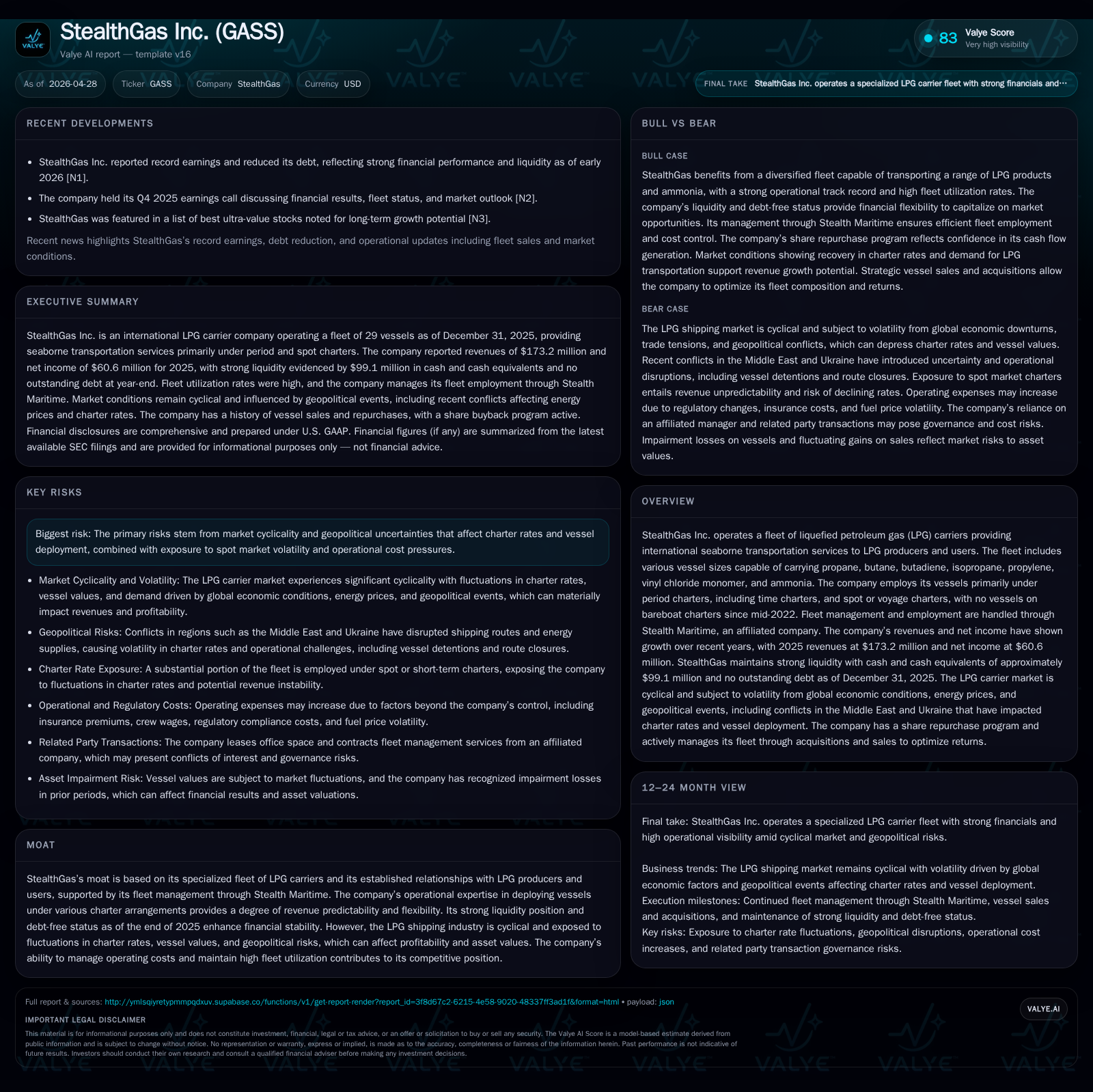

StealthGas Inc. Posts Record Earnings and Debt-Free Fleet Amid Market Volatility

StealthGas’s March 2026 quarterly update highlights record net income, full debt repayment, and strategic fleet moves supporting resilience in LPG shipping.

In its latest quarterly filing, StealthGas Inc. reported record net income of $60.6 million for 2025 alongside the elimination of all outstanding fleet debt as of year-end, underscoring robust financial discipline amid a volatile LPG shipping market. The company operates a specialized fleet of LPG carriers employing flexible charter structures to balance revenue stability with market upside capture. Despite operational setbacks including a key vessel’s prolonged off-hire from a port incident, StealthGas maintains strong liquidity and is actively optimizing its fleet through asset sales and joint venture realignments. Near-term growth hinges on resolving utilization constraints and executing planned drydockings while monitoring charter rate trends in critical Asian markets.

Latest Quarterly Operating Update: Navigating Challenges with Record Earnings

StealthGas Inc.'s most recent quarterly disclosure covering the twelve months ended December 31, 2025, reports a robust net income of $60.6 million, setting a new earnings milestone for the company despite headwinds stemming from reduced joint venture distributions and a significant loss of operating capacity due to an incident affecting its flagship vessel Eco Wizard at a Russian port since July 2025 [S2][F1]. The incident has effectively sidelined one large carrier (~40,551 cbm), reducing available operating capacity by roughly 12%, leaving the company with 25 active vessels out of its 28-strong roster including one joint venture unit as of early April 2026 [S1].

Financial discipline is reflected in aggressive deleveraging; StealthGas made $85.9 million in debt repayments during 2025 resulting in a completely debt-free core fleet as of December 31, 2025—a rare position within the shipping sector amidst rising interest rates and supply chain disruptions [S3][F1]. Importantly, this debt elimination enhances financial flexibility and risk resilience against the cyclical fluctuations typical of LPG shipping markets.

The company also engaged in strategic asset portfolio reshaping via the sale of two vessels in 2025 generating proceeds exceeding $25 million, alongside acquiring remaining equity interests in two joint venture-owned vessels—moves designed to improve control over cash flow streams and reinforce operational integration [S4]. Concurrently, management has continued an active share repurchase program, buying back over four million shares at an average price near $4.99 per share totaling approximately $21.2 million since mid-2023, signaling confidence in earnings sustainability despite spot market uncertainties [S3][N1].

Core Business Model: Specialized LPG Fleet and Flexible Charter Structures

StealthGas operates within a niche segment of maritime shipping focused on liquefied petroleum gases including propane, butane, butadiene, propylene, vinyl chloride monomer (VCM), isopropane, ammonia, among others. This specialized product mix demands dedicated carrier designs equipped to handle pressurized cargo safely—an established barrier limiting supply side competition relative to general dry bulk or crude oil tankers [S1].

The commercial strategy employs a blend of period charters—primarily multi-year time charters granting predictable cash flows—and spot/voyage charters that offer upside potential when market rates strengthen but introduce revenue variability [S1][S9]. Since mid-2022 the company exited bareboat charters entirely favoring operational models that retain responsibility for vessel operation costs but enable better pricing leverage.

This contracted charter structure balances steady earnings visibility with opportunistic positioning during favorable market cycles. For example, time charter equivalent (TCE) daily rates averaged around $12,334 in 2025 versus higher rates prior years reflecting modest market softening but above long-term averages given tight supply fundamentals [S24].

Fleet Management Excellence through Stealth Maritime Inc.

Stealth Maritime S.A., an affiliated entity under common control with StealthGas's management, handles all operational deployment decisions including crewing, maintenance scheduling, charter negotiations, and voyage planning [S1]. This arrangement provides centralized expertise maximizing fleet utilization (which averaged near 98.8% in 2025) while controlling operating expenses per day at roughly $4,965—slightly higher than previous years due to increased crew wages and maintenance but managed effectively against income pressures [S23][S24].

The synergy permits responsive charter mix adjustments amid fluctuating demand cycles while maintaining regulatory compliance and high safety standards essential for hazardous cargo transport. This control infrastructure constitutes a competitive moat shielding StealthGas from third-party operating disruptions or inefficient asset deployment.

Competitive Dynamics: Market Cyclicality, Charter Rate Volatility and Geopolitical Risks

The LPG carrier market is inherently cyclical influenced by macroeconomic trade shifts predominantly spanning Asia (notably China and India), Africa, Europe, and America [S1]. Seasonal heating demand concentrates volume into colder months boosting spot rates temporarily while unplanned geopolitical incidents—like closure risks around the Strait of Hormuz or sanctions affecting Russian ports—can constrain vessel availability or disrupt traditional trade routes [N1][S14].

Eco Wizard’s extended off-hire following a Russian port incident highlights vulnerability to such shocks causing a meaningful shortfall (~40k cbm) in owned capacity that may limit revenue generation until resolved or offset through fleet redeployment strategies [S1]. Meanwhile, rising bunker fuel prices and EU carbon regulations elevate voyage expenses impacting profitability unless those costs can be passed through or managed efficiently.

An additional layer derives from orderbook dynamics where speculative newbuilding orders amid perceived low asset prices can eventually flood supply depressing charter hire levels before natural attrition via scrapping occurs—a variable factored into impairment assessments conducted every quarter using nine-year historical average rates aligning expected recovery values with volatile market peaks/troughs [S10][S16].

Growth Opportunities: Fleet Optimization, Joint Venture Expansion, and Share Repurchases

StealthGas continues capitalizing on selective acquisition opportunities to consolidate its stake over joint venture vessels thereby securing greater discretionary control over earnings streams—a move improving cash flow visibility while rationalizing fleet composition toward higher-margin assets [S3][S20]. Recent acquisitions of remaining interests in two JV vessels at reported payments totaling $8 million underpin this approach.

Parallelly asset disposition programs reduce older/lower-efficiency tonnage improving operating expense profiles while freeing capital for reinvestment or shareholder returns. The vessel sales scheduled for April and September 2026 — one each sized ~5k cbm & ~3.5k cbm — will slightly lower overall capacity but align with modernization aims [S1].

Management’s steady stock repurchase program aggregating over $21 million signals internal confidence bolstered by strong operating cash flows exceeding $85 million annually supporting both organic growth investments and capital returns without compromising liquidity reserves [N1][S3]. This balance sheet discipline positions StealthGas advantageously against peers with heavier leverage amid uncertain cycle duration.

Constraints to Growth: Asset Utilization Risks and Spot Market Exposure

Aside from Eco Wizard's extended idling materially trimming revenue days (estimated loss equivalent to approx three to four vessels’ output), near-term utilization faces impacts from scheduled maintenance downtime including five anticipated drydockings for wholly-owned vessels during 2026—necessary capital intensive events that simultaneously decrease available revenue days though preserve long term operational integrity [S3][S14].

Further pressure stems from reliance on spot market segments sensitive to global LPG demand swings affected by macroeconomic downturns or energy transition dynamics possibly dampening fossil fuel volumes over time—even as product diversity partially mitigates this risk.

The current ratio approximating 9.3x suggests exceptionally conservative working capital conservancy providing operational liquidity room for unforeseen expenditure spikes or opportunistic investments without dependency on external financing access which may at times prove costly or restrictive given prevailing interest rate environments [F1][S3].

This enhanced credit posture pragmatically underpins management’s flexibility in contracting leverage selectively for acquisitions if economically warranted while minimizing interest burden during softer cycle periods.

Key Milestones Ahead: Vessel Sales, Drydockings, and Demand Indicators

Looking forward through mid-to-late 2026 StealthGas will focus execution on planned vessel disposals scheduled for April (one medium gas carrier at approx. 5,025 cbm) followed by a smaller ~3.5k cbm unit set for September delivery away from the fleet reducing nominal capacity but potentially improving overall yield metrics following replacement or redeployment moves [S1].

Simultaneously five major drydockings slated across owned vessels require careful cost management as these temporarily reduce daily available ship capacity though are crucial for regulatory compliance ensuring vessel competitiveness longer term.

Market watchers should closely track Asian LPG charter rate trends given their disproportionate impact on global seaborne flows influencing spot fixture activity—a bellwether reflecting underlying demand strength ahead of seasonal winter uplift phases integral to earnings volatility calibration.[S1]

Disclaimer: This analysis is based solely on information publicly disclosed through SEC filings as of early 2026 and verified news sources without incorporating any non-public data or projections beyond stated facts. Interpretation focuses on factual business model elements rather than investment recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments