Custom Truck One Source Faces Profitability Headwinds Despite Revenue Strength in Q1 2026

The company achieved revenue growth in Q1 2026 but continues to grapple with net losses and liquidity pressures amid competitive industry dynamics.

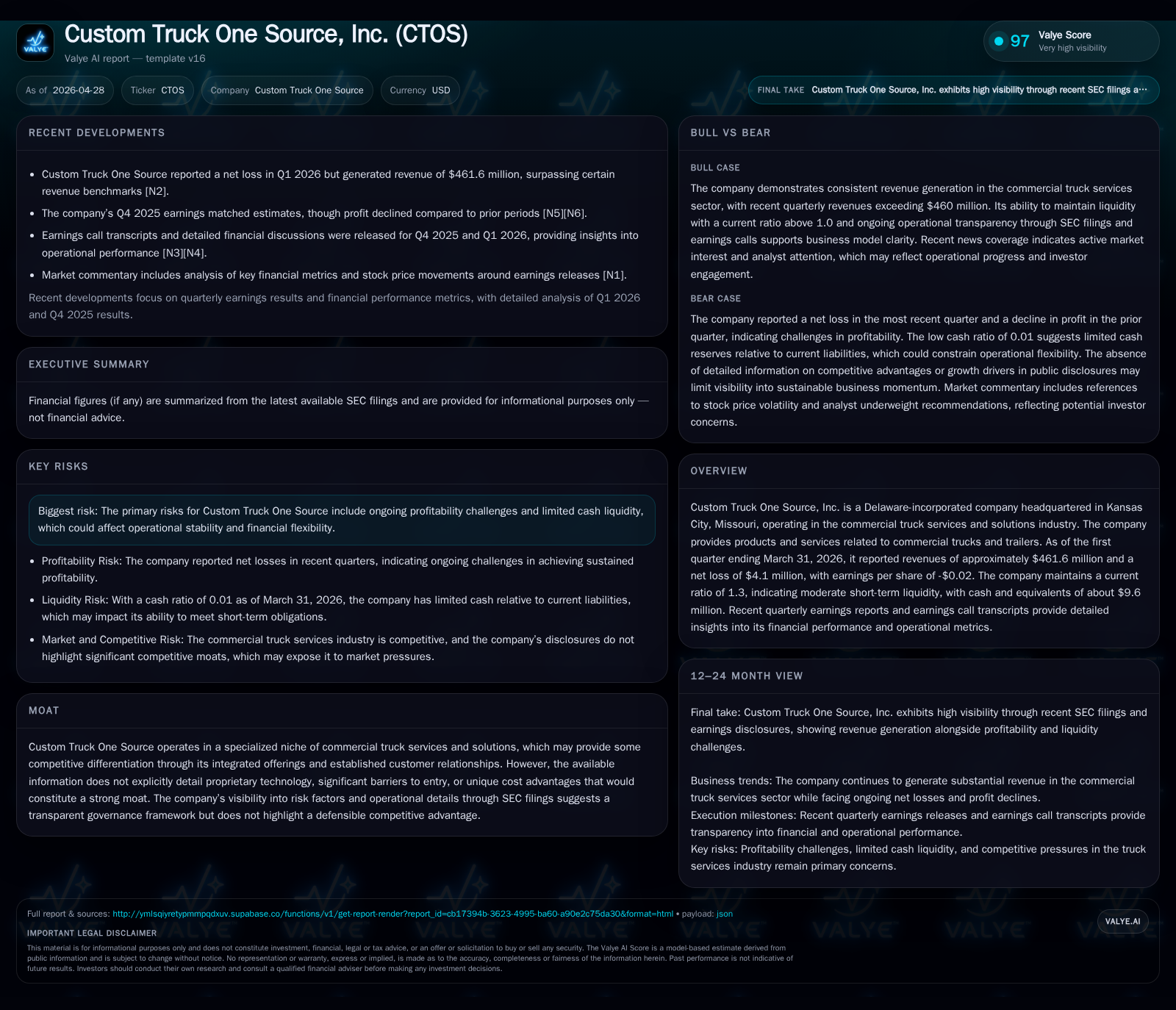

Custom Truck One Source reported Q1 2026 revenue of $461.6 million, beating expectations, yet posted a net loss of $4.1 million, reflecting ongoing profitability challenges. The firm operates an integrated commercial truck services business, balancing parts sales, rentals, and service repairs in a competitive landscape marked by supply and capacity constraints. While its established customer relationships offer some differentiation, heavy leverage and limited cash reserves constrain financial flexibility. Key growth drivers include expanding rental fleet utilization and aftermarket services, though margin improvement remains critical for sustainable gains. Investors should watch upcoming management guidance, operational efficiency initiatives, and potential refinancing developments.

First Quarter 2026 Results: Revenue Upside Against Net Loss

Custom Truck One Source delivered revenues of approximately $461.6 million for the first quarter ending March 31, 2026, surpassing analyst expectations by a notable margin [S2][N2]. Despite this topline strength—which reflects solid demand traction across its commercial truck solutions—the company reported a net loss of $4.1 million (EPS -$0.02), extending its sequence of profitability challenges [S2]. This juxtaposition signals pressure on operational efficiency and margin management despite stable top-line inflows.

Liquidity metrics at the quarter-end reveal cash and cash equivalents totaling about $9.6 million alongside current assets of roughly $1.26 billion versus current liabilities near $973 million, yielding a current ratio of 1.3 [F1]. This liquidity stance is modest but sufficient for near-term obligations; however, it leaves limited cushion against unforeseen shocks or aggressive investment needs.

Management's discussion emphasizes cost pressures driven by elevated fixed expenses inherent to maintaining a fleet-centric operations base alongside supply chain-driven increases in parts pricing [S2]. These factors weigh on gross margins and thereby contribute to the quarterly loss amidst still recovering freight volumes in the industry.

Understanding Custom Truck One Source’s Business Model and Product Offering

CTOS operates as an integrated commercial truck services provider with revenues derived principally from parts sales, equipment rentals, and repair/maintenance services spanning heavy-duty trucks and trailers [S1][S2]. The parts distribution network supplies OEM and aftermarket components critical for fleet upkeep, while rental offerings provide short- to medium-term vehicle solutions that support customer operational flexibility.

Service contracts frequently involve long-term maintenance arrangements that create switching costs and build customer stickiness through comprehensive coverage footprints across multiple U.S. regions [S1]. Such bundled solutions differentiate CTOS vis-à-vis standalone or single-segment competitors who lack scale or geographic breadth.

However, product mix dynamics show that higher-margin rental utilization has cyclical sensitivity tied to transportation sector activity levels; parts sales also fluctuate with economic cycles but benefit from an installed base requiring ongoing maintenance irrespective of new truck sales trends [N1]. CTOS’s balance across these segments helps modulate cyclicality but does not eliminate margin volatility.

Competitive Positioning in the Commercial Truck Services Industry

The commercial truck services sector is characterized by fragmented competition dominated by regional providers alongside national players like CTOS [S1]. While CTOS benefits from an integrated offering that couples distribution with rental and repair capabilities—facilitating one-stop-shop advantages—its moat is moderate rather than defensible at a high level due to lack of proprietary technology or exclusive supplier relationships.

Pricing power is constrained by competitive pressure among peers competing on cost efficiency and network accessibility [N4]. Supply chain complexities—especially parts availability—pose ongoing operational risks that can limit timely servicing capacity or drive up inventory carrying costs [S23]. Capacity bottlenecks also affect rental fleet utilization potential as capital outlays for fleet expansion are substantial.

Regulatory influences stem mostly from evolving safety standards and environmental compliance mandates governing fleet operations which can impact maintenance scheduling frequency and parts requirements but do not presently impose direct cost pass-through mechanisms [S19].

Key Growth Drivers Versus Operational and Financial Constraints

Growth prospects hinge on increasing rental fleet utilization rates supported by rising demand for flexible equipment access amid fluctuating transport volumes [S2]. Additionally, enhancing aftermarket services—including maintenance contracts—can boost recurring revenue streams less sensitive to capital expenditure downturns.

Nonetheless, operational constraints persist through margin compression caused by high fixed cost absorption challenges along with pricing competition reducing premium capture abilities. Capital expenditures to maintain and grow rental fleets amplify leverage burdens amidst elevated debt levels nearing $1.65 billion net of cash at quarter-end [F1].

The company needs to navigate refinancing risk prudently while managing working capital tightly to avoid liquidity crunches during cyclic downturns or macroeconomic shocks impacting freight activities.

Near-Term Catalysts and Risks to Monitor

Upcoming developments to watch include updated management guidance expected post-Q1 earnings calls which may clarify path toward profitability restoration initiatives such as cost reduction programs or pricing adjustments [S3]. Execution success in boosting margin profiles through improved operational efficiencies or higher rental utilization will be pivotal.

Refinancing milestones are noteworthy given the current debt load; any tightening in credit conditions could pressure financial flexibility unless addressed proactively [F1]. Regulatory policy shifts related to fleet emissions or safety standards remain potential risk factors capable of influencing operating costs indirectly.

Market demand fluctuations tied to broader transportation sector health remain cyclically exposed; sustained weakness could exacerbate margin pressures while sustained recovery might alleviate operating leverage issues over time.

Summary of Financial Health and Capital Structure

From a financial perspective, CTOS’s current liquidity position shows $9.6 million in cash holdings against a current ratio of approximately 1.3 (current assets of $1.26 billion vs liabilities of $972.8 million) as of March 31, 2026 [F1]. This suggests acceptable short-term solvency but limited excess liquidity available for non-operating uses.

Leverage stands elevated with net debt close to $1.64 billion after accounting for cash balances; this level raises concerns about interest burden sustainability amid recurring net losses and restricts strategic maneuverability regarding acquisitions or organic investment without incremental financing arrangements [F1].

In conclusion, while Custom Truck One Source demonstrates resilient top-line performance supported by its integrated commercial truck service delivery model, the company must address persistent profitability headwinds compounded by significant leverage constraints. Enhancing operating margins through efficiency improvements alongside careful capital structure management will be essential priorities moving forward.

This analysis is based solely on publicly available information from SEC filings dated through April 27, 2026, supplemented by relevant market reports as cited; it does not constitute investment advice.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments