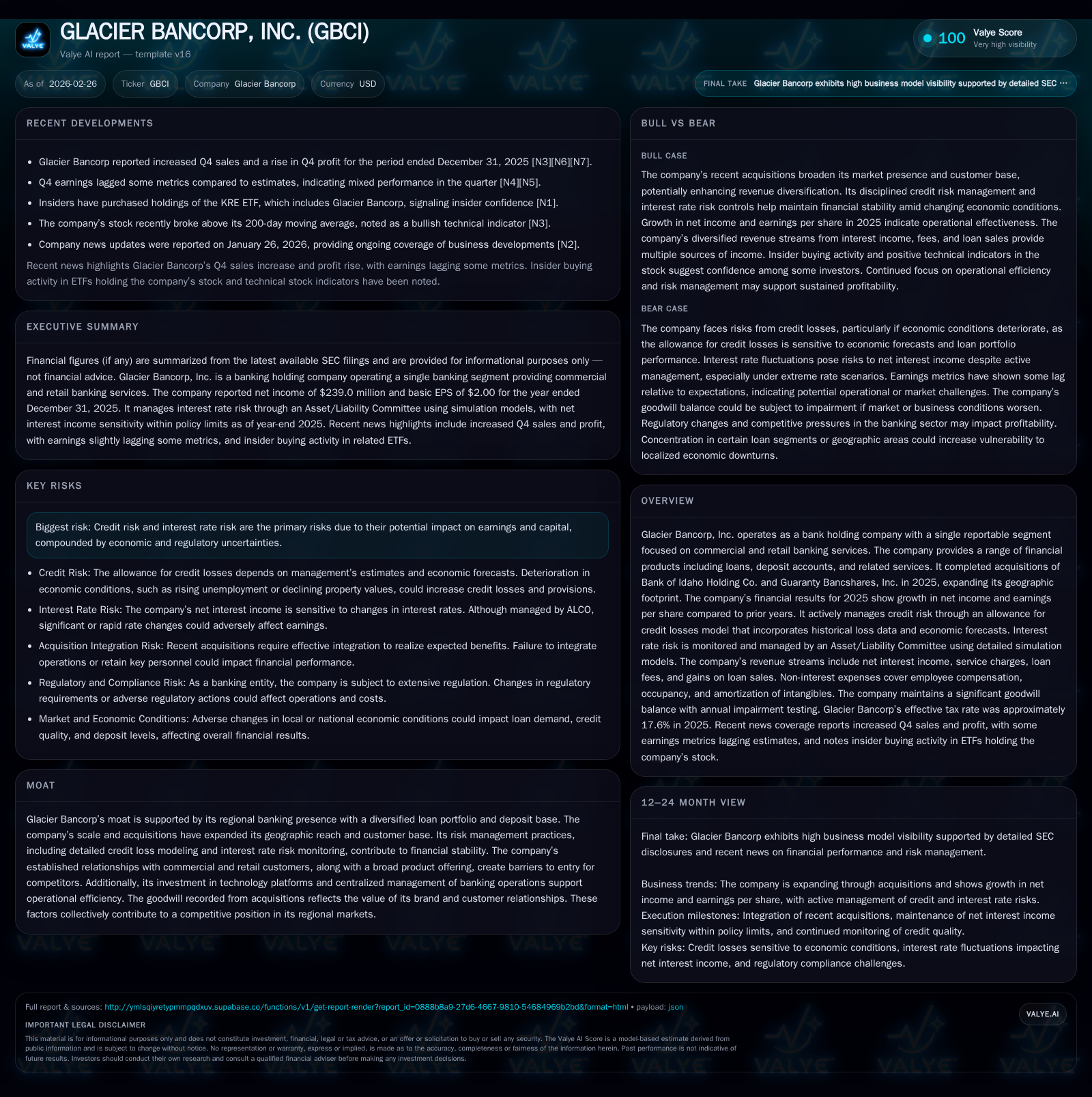

Glacier Bancorp's Expansion and Earnings Surge: Assessing the Impact of 2025 Acquisitions

Analyzing how strategic acquisitions in 2025 propelled Glacier Bancorp's net income growth alongside evolving risk management and capital allocation.

Glacier Bancorp, Inc. experienced a pronounced acceleration in net income in 2025, largely driven by the acquisitions of Bank of Idaho Holding Co. and Guaranty Bancshares, which expanded its regional footprint. The company's disciplined allowance for credit losses (ACL) modeling and comprehensive interest rate risk hedging underscored financial stability amid economic uncertainties. While revenue dipped slightly year-over-year, robust operational cash flows and strategic capital management supported shareholder returns through dividends. Future growth depends on successful integration of acquisitions and navigating credit cycles amid an evolving interest rate environment.

Historical Growth Trajectory and Income Drivers Through 2025

Glacier Bancorp demonstrated a significant inflection in profitability in fiscal year 2025, propelled predominantly by strategic acquisitions that reshaped its operational scale. The company reported net income soaring to $239.0 million in 2025, marking an extraordinary 287.1% increase over the prior year’s $61.8 million [F1]. This leap contrasts with a marginal decline in total revenue of 4.5% year-over-year, indicative of pressures on overall top-line performance despite expanded loan portfolios and deposit accounts [F1].

Operating cash flow showed resilient strength with a 45.1% increase to $374.4 million, underscoring strong underlying cash generation capacity amidst moderate capex reduction from $48.3 million in 2024 to $26.8 million in 2025 [F1]. This capex cut likely reflects efficiencies gained through consolidation post-acquisitions.

Loan portfolio diversification played a key role historically — segment disclosures confirm concentration across commercial real estate ($13.6 billion at end-2025), other commercial loans, residential real estate, and consumer lending categories, supporting balanced income streams from interest and fees [S3][S4][S20]. The company’s ACL methodology further modulates earnings volatility by dynamically accounting for expected credit losses using loan delinquency trends combined with economic forecast inputs [S1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|

| 2025 | 239 | 374 | 27 | +287.1% |

| 2024 | 62 | 258 | 48 | +13.7% |

| 2023 | 54 | 501 | -31.8% | |

| 2022 | 80 | 471 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 163 | 348 | 5.7 |

| 2024 | 150 | 210 | 1.9 |

| 2023 | 147 | 1.8 | |

| 2022 | 158 | 2.8 |

Source: SEC companyfacts cache [F1].

Note: Detailed revenue exact amounts are not presented explicitly beyond historical trends; net income and cash flow data cited from [F1].

Strategic Acquisitions: Bank of Idaho Holding Co. and Guaranty Bancshares Impact Analysis

In April and October of 2025 respectively, Glacier Bancorp consummated two material acquisitions: Bank of Idaho Holding Co., based in Idaho Falls, Idaho; and Guaranty Bancshares, Inc., headquartered in Mount Pleasant, Texas [S4]. These community bank acquisitions were accounted for under the acquisition method leading to immediate consolidation of financial results from the respective dates.

Goodwill recorded on acquisition rose sharply by approximately $327 million to $1.38 billion reflective of intangible assets such as customer relationships, brand equity, and anticipated synergistic benefits embedded in these deals [S4][S1]. Management emphasizes annual goodwill impairment testing under GAAP given the elevated goodwill base — no impairments recorded to date but sensitivity remains high relative to regional economic shifts or operational challenges [S1].

Operationally, these acquisitions expanded Glacier Bancorp's geographic footprint markedly into new regions across the Mountain West and South Central United States markets broadening both commercial and retail customer bases.

No segment reporting distinctions were introduced post-acquisition; rather internal management recognizes the firm as a unified operating entity serving consistent customer cohorts via standardized technology platforms facilitating scale efficiencies [S15].

Credit and Interest Rate Risk Management: Crucial Levers for Stability

Effective risk management is central to Glacier Bancorp’s sustained financial health particularly amid an uncertain macroeconomic landscape characterized by fluctuating interest rates and variable credit cycles.

The allowance for credit losses (ACL) framework incorporates multiple predictive factors including loan volumes, delinquency status, borrower credit ratings, historical loss experience adjusted for reasonable economic forecasts such as unemployment trends and interest rate trajectories [S1][S20]. The increase in provisioning to $61.8 million in FY2025 compared with $27.2 million prior reflects prudent management response anticipating possible credit deterioration linked with broader economic headwinds.

Interest rate risk is systematically controlled through the Asset/Liability Committee which utilizes detailed simulation models evaluating potential impact on net interest margin (NIM), liquidity, and earnings under diverse interest rate scenarios [S6]. Derivative instruments including interest rate swaps designated as fair value hedges effectively mitigate repricing mismatches on investment securities portfolios valued over $7 billion at year-end [S6][S17]. Additionally, interest rate cap agreements serve as cash flow hedge mechanisms protecting variable rate subordinated debt exposures against adverse rate spikes while maintaining hedge accounting effectiveness sustaining earnings stability.

These layered hedging activities ensure volatility dampening support enhancing risk-adjusted profitability over time.

Earnings Trends Versus Market Expectations in Q4 2025

Quarterly earnings reports revealed a mixed picture relative to analyst consensus during Q4 of fiscal year 2025.

Headline Q4 sales showed increases mainly attributed to core deposit fee income growth alongside rising loan fee revenue streams evidencing operational resilience beyond traditional net interest margins [N8]. However, reported earnings slightly lagged estimates due primarily to episodic expense items related to integration costs following recent acquisitions plus heightened provision allocation impacting profitability metrics [N2][N3]. Despite this miss on bottom-line estimates, the quarter reinforced overall revenue diversification through service charges including overdraft fees plus debit card interchange revenues that represent stable non-interest income components important during periods of loan yield pressure [S22].

Capital Structure Evolution and Shareholder Returns in a Transitional Year

Glacier Bancorp ended FY2025 with stockholders’ equity reaching approximately $4.2 billion representing substantial growth from $3.2 billion in prior year driven by retained earnings accumulation along with paid-in capital from issuance activities linked partly to acquisition financing structures [F1][S19].

Regulatory capital adequacy guidelines classify the company as well-capitalized across Tier 1 and total capital ratios preserving dividend distribution capacity under Federal Reserve oversight without constraints typical in transitional acquisition periods [S21].

Dividend distributions modestly increased from $150 million in FY2024 to about $163 million reflecting confident capital return policies aligned with sustained net income improvements [F1][S16]. No share repurchases were disclosed suggesting focus remained on reinvestment priorities post-acquisition plus maintaining conservative leverage levels amidst market volatility.

Return on equity approximates at a measured ~5.7%, indicating solid but disciplined profitability consistent with regional bank profiles navigating integration complexities while augmenting franchise value incrementally [F1].

Future Outlook: Regional Expansion Prospects and Economic Challenges

Looking forward, Glacier Bancorp expects sustained growth leverage opportunities emanating from its widened geographic coverage achieved through the Idaho and Texas acquisitions expanding its client base within commercially attractive Western U.S markets alongside Texas's growing economy [N3][S4]. Loan portfolio quality will remain a focal point given cyclicality risks tied closely to local economies’ performance.

Credit cycle vigilance will be required as elevated provisions suggest forward-looking precautionary buffers responding to potential upticks in delinquencies should employment or interest rates move unfavorably [S8]. Deposit growth could benefit from brand recognition gains catalyzed by enhanced regional presence although competition remains intense among community banks for both consumer relationships and commercial lending deals.

Continued investment into technology platforms facilitating centralized banking operations aims at cost efficiency optimization that could partially offset margin pressures caused by rising funding costs or compressed spreads influenced by monetary policy shifts.

What Investors Should Monitor Ahead

Analysts should closely watch integration milestones of Bank of Idaho Holding Co. and Guaranty Bancshares encompassing cultural assimilation, retention of key personnel, cost synergy realization timelines versus projections disclosed previously.

Updates on ACL adjustments will provide real-time insight into how macroeconomic developments translate into credit quality shifts impacting future provisions.

The evolution of derivative hedge effectiveness particularly regarding net interest margin protection during changing interest rate regimes warrants scrutiny alongside regulatory model amendments affecting capital calculations or dividend distributions.

Monitoring legal proceedings remains prudent though current disclosures affirm no material adverse impacts expected from ongoing claims or litigations borne under adequate insurance coverage frameworks [S8].

In summary, Glacier Bancorp enters early stages of an expanded market phase backed by improved earnings power though layered with transitional complexities requiring sustained risk discipline amid variable economic conditions.

This analysis is prepared solely for informational purposes without any investment recommendations or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments