Green Dot Corp’s Q1 Reveal: Merger Risks and Customer Concentration Spotlighted

The latest quarterly filing underscores significant merger execution uncertainties alongside concentrated revenue streams shaping Green Dot’s near-term outlook.

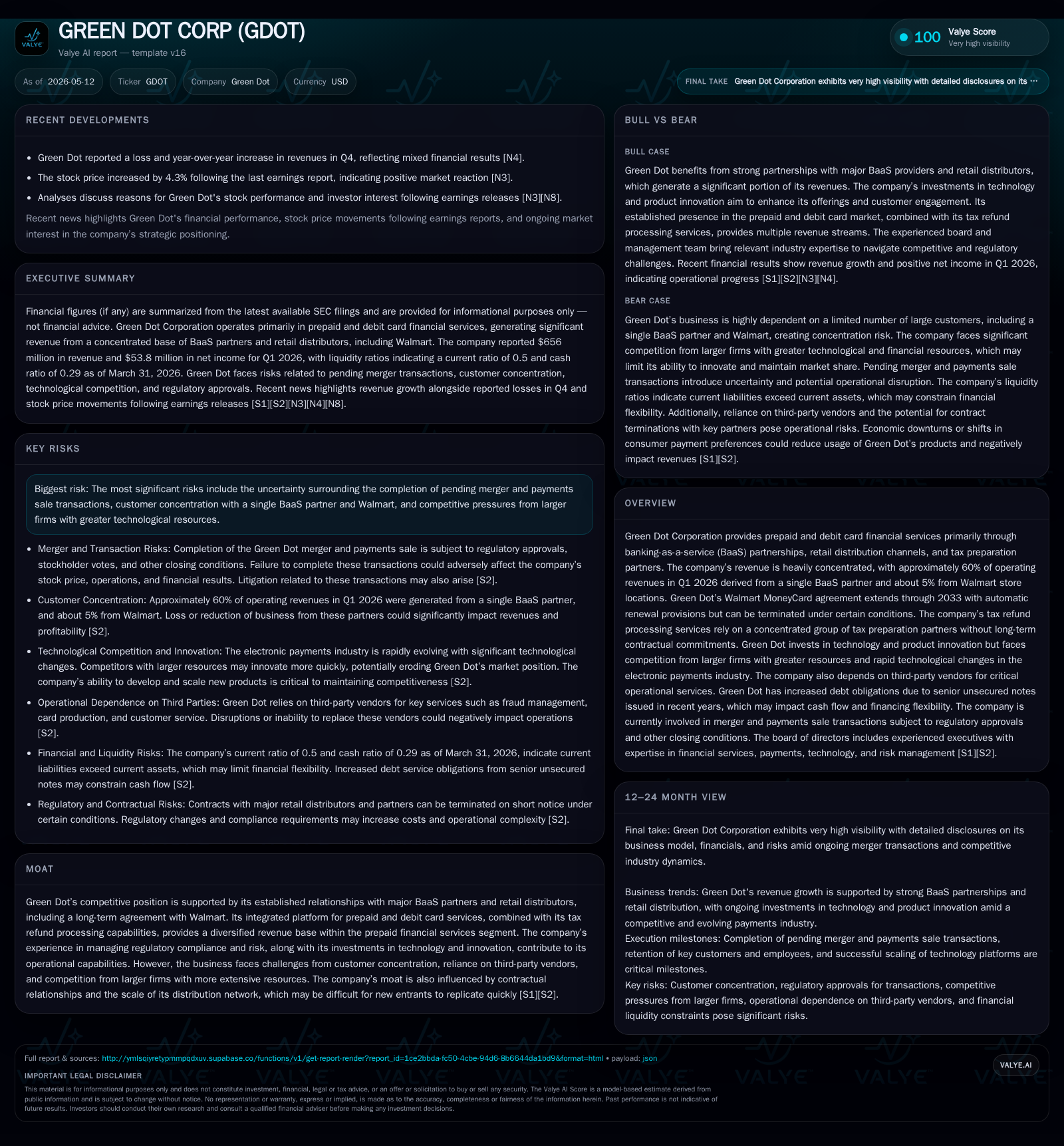

Green Dot Corporation's Q1 2026 10-Q highlights critical risks related to pending merger and payments sale transactions, which could materially affect its business trajectory if not completed successfully. The firm's revenue remains heavily dependent on a single banking-as-a-service partner and Walmart, underscoring concentration risks. Despite a durable Walmart MoneyCard agreement providing some stability, the company faces pressures from competition and regulatory changes. Key growth avenues center on enhancing partner wallet share and expanding retail distribution, though execution hinges on navigating these near-term operational uncertainties.

Q1 2026 Operating Update: Transaction Uncertainties Take Center Stage

Green Dot’s May 2026 10-Q filing decidedly centers its near-term narrative on the uncertain fate of two pivotal strategic transactions: a merger with CommerceOne and a related payments sale agreement [S2]. The filings underscore that completion conditions for these deals remain unsettled; failure to close could result in $27 million in termination fees payable by Green Dot as well as substantial expenses already incurred that would not yield anticipated benefits. This transactional limbo also poses soft costs such as management distraction and adverse market reaction risks.

The company explicitly acknowledges risks to employee retention during this period of uncertainty—a critical factor given its dependence on talent for technology development and partner management. Moreover, there is material concern over potential customer dislocations as counterparties respond to the pending merger environment or reassess their relationship dynamics [S2][S3]. These disclosures highlight an immediate structural risk dimming visibility into Green Dot’s business momentum.

Business Model Overview: Prepaid Financial Services and Revenue Concentration

Green Dot’s core operations revolve around offering prepaid debit cards and financial services delivered principally through banking-as-a-service (BaaS) partnerships combined with retail distribution networks and tax-refund facilitation channels [S1]. Notably, about 60% of their operating revenues in Q1 2026 derive from a single large BaaS partner—reflecting significant client concentration vulnerability—while Walmart store locations contribute approximately 5% under an agreement extending through 2033 with automatic renewal clauses but stipulated termination rights [S1][S2].

This partnership ecosystem drives revenue chiefly via interchange fees, account maintenance charges, reload fees, card activation fees, and ancillary service offerings linked to prepaid card usage. Since customers pay fees embedded in card transactions or services often connected to tax refund processing done through concentrated tax preparation partners without long-term contracts, revenue streams can exhibit volatility depending on consumer activity cycles and regulatory fee pressures.

Technology investment efforts focus on evolving product features such as real-time balance notifications, direct deposit optimization, fraud prevention enhancements, and user-friendly mobile interfaces designed to increase usage frequency and stickiness. However, the company’s reliance on third-party vendors for platform infrastructure introduces operational dependencies that could impact service reliability or affect margins if vendor cost structures or service levels fluctuate.

Competitive Landscape: Scale-Driven Pressures and Distribution Moat

Operating within a competitive prepaid financial services industry characterized by rapid technological innovation and incumbent dominance by larger players—including major banks and payment networks—Green Dot stakes its competitive advantage on entrenched relationships with key BaaS clients (notably the dominant one contributing about 60% of revenues) and retail distributors such as Walmart [S1].

Their integrated platform approach encompassing prepaid debit issuance plus tax refund processing services offers diversified revenue exposure within the prepaid segment. Additionally, regulatory compliance expertise—especially navigating complex bank holding company requirements—and risk management capabilities represent operational strengths few newcomers can quickly replicate.

That said, scale economies favor larger rivals who can invest more aggressively in technology upgrades and marketing spend to capture wallet share. The high customer concentration also limits resilience against partner departures or contract renegotiations unfavorable to Green Dot. Consequently, while distribution network scale confers some moat qualities by creating switching frictions for established large clients, it simultaneously concentrates risk exposure.

Growth Drivers: Innovation, Partnership Expansion, and Market Penetration

Green Dot plots growth primarily through deepening engagement with its existing sizable BaaS clients by cross-selling upgraded financial products coupled with leveraging innovation in mobile fintech features designed to boost cardholder usage intensity [S1][S2]. Effective rollout of new offerings targeting segments like underbanked consumers or gig economy workers forms part of this strategy.

Retail channel expansion beyond Walmart remains an aspirational lever for broadening physical presence while direct-to-consumer marketing initiatives aim at enhancing brand recognition in crowded prepaid markets. Success in these areas is measurable through KPIs such as incremental monthly active users linked to BaaS platforms, same-store sales growth at retail outlets carrying Green Dot cards, wallet share increases in multi-product customers, and subscription upticks for value-added services.

Timing of product launches alongside marketing campaigns plays a pivotal role in turning investments into tangible top-line revenue gains given lag effects inherent in customer adoption curves. Competent execution addressing customer retention amidst intensifying competition is equally vital.

Risk Factors: Merger Completion, Customer Concentration, and Partner Dependency

Foremost among disclosed risks is failure to finalize the merger with CommerceOne or close the payments sale transaction which would impose immediate financial impacts including termination fees plus sunk cost write-offs associated with transaction execution activities [S2]. This transactional risk eclipses routine operating concerns due to potential adverse effects on stock price valuations plus possible disruptions in ongoing business due to employee attrition or shaken customer confidence.

Customer concentration compounds these challenges—with most revenue coming from one major BaaS partner—raising vulnerability should that relationship sour or contract terms change under competitive pressure or shifting strategic priorities by that partner [S2]. Similarly, although the Walmart MoneyCard agreement spans several years with renewal provisions ensuring medium-term stability, specific conditions exist enabling termination which remains a watchpoint given its significance as a distribution channel contributor.

Additional headwinds arise from intensifying industry-wide regulatory scrutiny around interchange fee rates which underpin substantial portions of Green Dot’s income. Legislative initiatives aiming to lower these rates could necessitate fee structure adjustments detrimental to customer acquisition or retention dynamics thereby compressing margins [S20]. The firm has also increased debt service obligations following senior unsecured notes issuance elevating fixed financial commitments that may constrain flexibility if operating cash flow falters [F1][S4].

Monitoring Points: Key Milestones and Execution Variables Ahead

Market participants should closely track progress toward merger approval milestones including shareholder votes alongside regulatory clearances influencing deal closure timing. Parallelly important are greenlight signals from dominant BaaS partners reflecting contract renewals or expansions providing insight into revenue durability post-transaction timeframe [S2][S3][S9].

Operational readouts evidencing new product adoption rates or expanded retail footprint penetration will serve as tangible indicators whether growth initiatives gain traction despite transactional distractions. Regulatory developments impacting interchange fee regimes or compliance costs constitute critical external variables warranting monitoring due to their potential effect on revenue mix viability.

Finally, liquidity trends revealing ongoing ability to meet increasing debt servicing demands without restricting investment capacity merit scrutiny given midterm capital structure implications [F1][S4].

Current Financial Snapshot: Liquidity Constraints Amidst Debt Obligations

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $1.646 billion | |

| 2026-03-31 | ||

| Current assets | $2.830 billion | |

| 2026-03-31 | ||

| Current liabilities | $5.644 billion | |

| 2026-03-31 | ||

| Current ratio | 0.5 | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026—per latest quarter data—the company reported cash & equivalents totaling approximately $1.65 billion set against current liabilities exceeding $5.64 billion resulting in a constrained current ratio of around 0.5 which signals near-term liquidity tension under standard working capital metrics [F1].

The firm’s increased leverage profile reflects $65 million aggregate principal senior unsecured notes maturing in September 2029 entailing heightened fixed interest payments reducing free cash flow available for discretionary uses such as growth funding or shareholder returns [F1][S4].

It does not constitute investment advice but aims to provide a grounded operational perspective on Green Dot’s business model dynamics facing critical near-term events._

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments