Navigating Ambiguity: An Analytical View of GRAHAM CORP’s Financial Posture Amid Sparse Disclosure

GRAHAM CORP presents a robust liquidity profile in its latest filings, yet operational opacity challenges thorough evaluation.

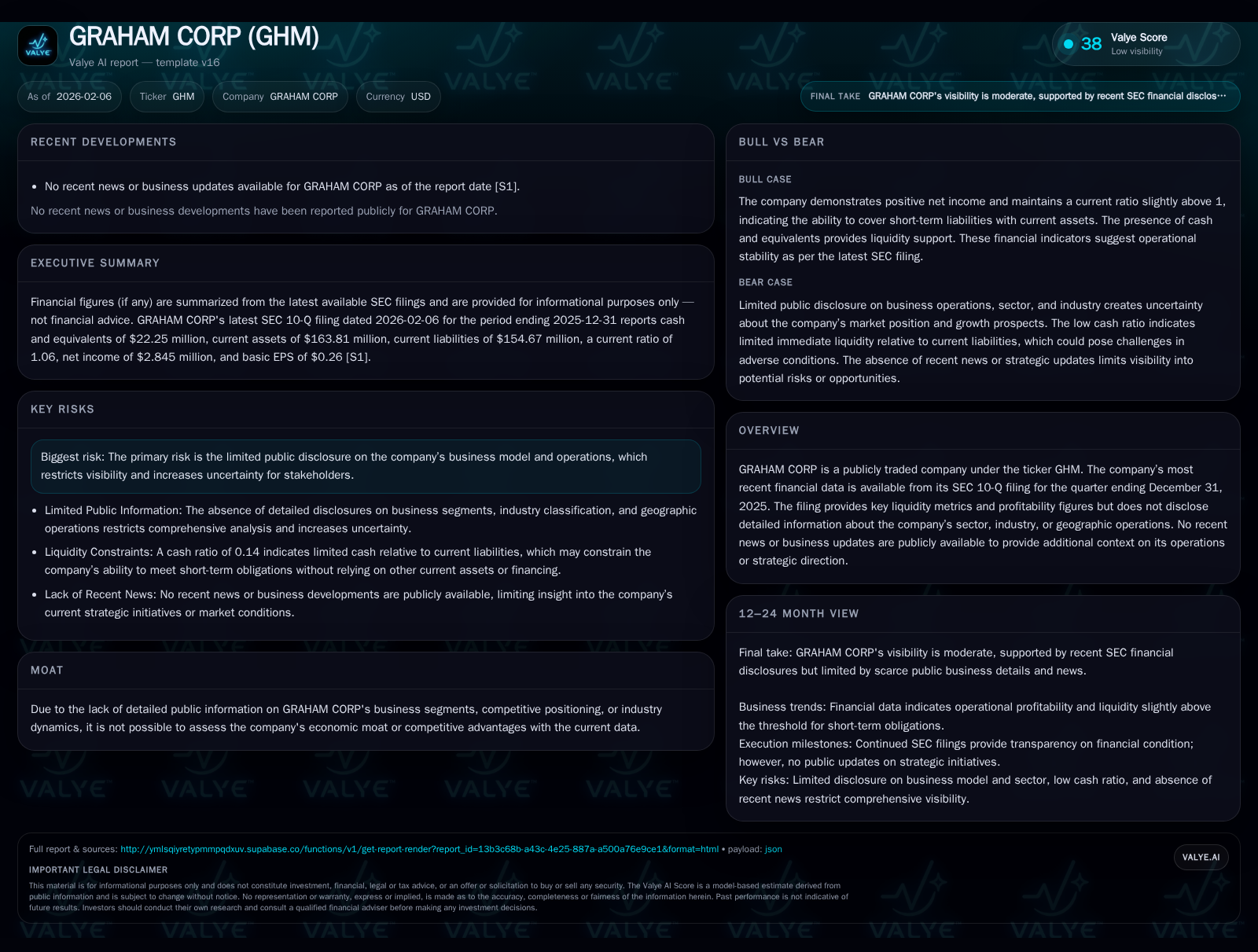

GRAHAM CORP’s most recent 10-Q reveals a company with solid short-term financial metrics, including a net income of $2.85 million and a current ratio slightly above one, reflecting a manageable liquidity position. However, the lack of publicly available information regarding its industry, business model, or strategic direction creates significant challenges in assessing competitive positioning or long-term prospects. This analysis explores the tension between quantitative financial stability and qualitative uncertainty, underscoring the complexities investors face when critical contextual data is absent.

Unmasking Financial Strength in the Face of Operational Opacity

GRAHAM CORP’s recent filings present an intriguing dichotomy: financially measurable stability yet an opaque operational story. The company's latest SEC Form 10-Q for the quarter ending December 31, 2025 provides clear numeric indicators — notably liquidity and earnings figures — but conspicuously omits any detail on industry affiliation, product lines, customer base, or geographic footprint [S2][F1]. This absence establishes an analytical tension; while balance sheet metrics appear solid on the surface, the foundational context to interpret these figures meaningfully remains veiled.

Against this backdrop, analysts encounter the challenge of unpacking raw financial data without supportive qualitative information. The firm’s reported net income and asset-liability positions suggest current viability but leave open fundamental questions about growth drivers or sector-specific risks. Without disclosed operational narrative or segment breakdowns, we must approach conclusions conservatively, balancing observed financial health with recognition of substantial blind spots.

Liquidity Metrics: The Pillar Supporting GRAHAM’s Short-Term Stability

At the core of GRAHAM’s financial resilience lies its liquidity stance. As of December 31, 2025, cash and equivalents stand at approximately $22.3 million within a total current asset base just over $163.8 million [F1]. Against these assets are current liabilities summarized near $154.7 million — yielding a current ratio of roughly 1.06. This metric indicates that GRAHAM possesses slightly more current assets than immediate obligations.

However, while above the conventional threshold of 1.0 that signifies basic solvency, this margin is noticeably thin. Such proximity suggests limited buffer against unexpected cash flow disruptions or spikes in obligations. The company can cover its near-term debts but only with narrow flexibility — a fact magnified by missing operational clarity which otherwise could illuminate cash conversion cycles or working capital dynamics.

Moreover, cash reserves relative to liabilities call attention to potential liquidity risk. Holding $22.3 million cash provides some immediate flexibility but represents just over 14% of current liabilities [F1]. This further underscores the delicate balancing act between asset availability and creditor demands within this limited disclosure environment.

Profitability Snapshot: Net Income Insights from the Latest 10-Q

Complementing liquidity statistics is GRAHAM CORP’s reported net income totaling approximately $2.85 million for Q4 2025 [F1]. This figure confirms positive earnings generation amid what appears to be a challenging transparency landscape.

Yet absent accompanying revenue totals or segment profitability details dilute interpretive power here. The scale and sustainability of earnings remain unknown without insight into underlying operational drivers — whether they stem from recurring core activities or potentially ephemeral factors like asset sales or one-time adjustments.

Consequently, while net income reflects some degree of profitability discipline at GRAHAM’s helm, prudent analysis demands restraint in extrapolating forward performance expectations from this isolated data point alone.

Risk Shadows: How Limited Disclosure Elevates Uncertainty

The principal risk emerging from GRAHAM’s latest reporting is informational deficiency—a condition that inherently compounds uncertainty in market valuations and investor decision frameworks [S2]. Management's discussion and risk factor sections offer no clarifying illumination on business specifics but note only limited overarching disclosures.

This strategic opacity can increase stock price volatility due to event-driven speculation when baseline knowledge is insufficient to anchor expectations securely. It also hampers proper benchmarking against industry peers or sector norms since classification itself remains undisclosed.

Such disclosure gaps translate into heightened perceived investment risk owing not to underlying operational failings necessarily but to diminished capacity for stakeholders to perform rigorous due diligence or monitor evolving fundamentals effectively.

Decoding the Current Ratio: A Narrow Margin for Cushion

Interpreting GRAHAM’s current ratio warrants nuanced consideration given its proximity to unity at approximately 1.06 [F1]. From a solvency perspective, surpassing a 1-to-1 mark implies assets can nominally cover liabilities maturing within the year — meeting standard quick-turnover criteria.

Yet this slight advantage carries dual implications. On one hand, it suggests neither insolvency nor immediate liquidity crisis; on the other hand, it signals vulnerability should unforeseen cash demands arise or if asset realizations prove slower than anticipated.

In environments transparent about operating cycles and working capital efficiency, analysts could better contextualize whether such margins are sustainable or sporadic results of timing irregularities—here they must acknowledge both sufficiency and fragility within these figures given missing contextual inputs.

Strategic Blind Spots: Challenges in Assessing Moat and Competitive Standing

Arguably the most significant analytic void concerns GRAHAM CORP’s economic moat and relative competitive positioning [valye_report_excerpt]. Explicit absence of any industry designation hinders attempts to identify sources of differentiation whether technological innovation, cost leadership, regulatory barriers, or customer loyalty.

Without visibility into product portfolios or market penetration depth, it is effectively impossible to ascertain long-term defensibility against competitors or entry barriers that typically anchor durable earnings streams.

Management has not disclosed elements commonly linked with structural moats such as patents or proprietary processes [valye_report_excerpt]. Consequently any inference regarding sustainable competitive advantage would be speculative outside observable financial snapshots provided by filings.

Investor Implications: Gauging Confidence Amid Stretched Visibility

From an investor standpoint — particularly institutional mandates stressing due diligence protocols — GRAHAM Corp represents a conundrum characterized by “trust but verify” tensions intensified by sparse updates beyond numerical filings [S2][F1][valye_report_excerpt].

Retail participants may find comfort in reported profitability and headline liquidity yet confront uncertainty amplified by absent narrative context supporting those numbers.

Institutional investors’ frameworks often require segmentation analysis and market trend insights before allocating resources; such requirements remain unmet here given non-disclosure beyond standard statutory filings.[S2]

Thus confidence calibration must involve weighing documented short-term financial health against unknown operating parameters—a calculus prone to wider margin-of-error assumptions.

The Investment Conundrum: Weighing Quantitative Signals Against Qualitative Unknowns

Ultimately GRAHAM CORP exemplifies a scenario faced frequently within equitized markets: robust quantitative disclosure outpaces qualitative transparency requisite for comprehensive valuation layering [S2][F1][valye_report_excerpt].

While recent filings evince stable earnings generation alongside narrowly sufficient liquidity buffers providing some assurance against immediate distress scenarios, this clarity resides atop an informational vacuum where key operational characteristics remain undisclosed.

For sophisticated market participants valuing data integrity over conjecture,the primary takeaway involves balancing faith in hard numbers with humility regarding interpretative limits imposed by non-disclosure policies.

The absence of a discernible moat narrative cautions against extrapolation beyond measured appreciation for reported results – underscoring how omitted context forms critical opaque layers pressing repeated due diligence rigor.

Disclaimer: This analysis is based solely on publicly available information as of February 6, 2026 and does not constitute investment advice or predictions regarding future performance.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments