Global AI Advances Agentic Platform Growth with Strategic M&A and Regulatory Navigation

Global AI progresses its autonomous AI platform commercialization with key leadership arrangements and a recalibrated M&A strategy amid regulatory scrutiny.

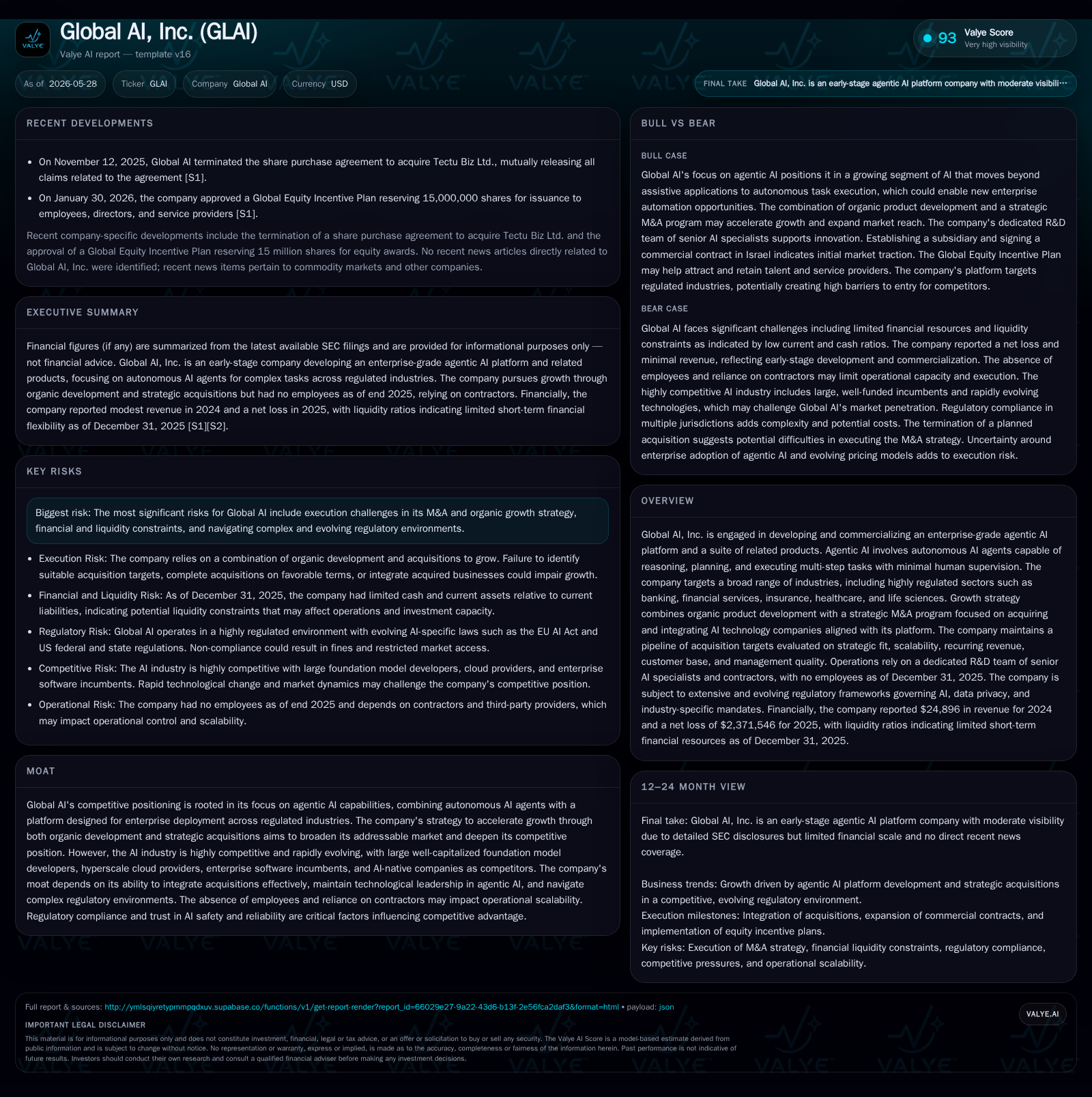

Global AI, Inc., focusing on its enterprise-grade agentic AI platform, reported recent developments including termination of a significant acquisition deal and an executive employment agreement aligning CEO incentives to performance milestones. Its growth strategy combines organic R&D led by senior AI specialists with a disciplined acquisition program targeting scalable AI technology firms. The company operates under tight liquidity constraints, with substantial operating losses and a limited workforce model reliant on contractors. Regulatory complexity in the AI sector presents both challenges and barriers that may impact acquisition execution and product deployment.

Latest Operating Highlights and Corporate Developments

The most recent filings from Global AI delineate pivotal shifts in operational focus and governance alignment. The 2025 third-quarter 10-Q [S2] underscores continued developmental spending resulting in sizable operating losses exceeding $2 million annually. These losses accompany a lean organization model consisting solely of contracted teams without direct employees as of year-end 2025 [S14]. On May 13, 2026, an 8-K filing [S3] revealed the CEO Darko Horvat’s employment agreement stipulating a base salary of $650,000 plus incentive compensation up to 50% based on Board-approved key performance indicators (KPIs). This alignment is further enhanced by milestone-contingent restricted stock unit grants valued between $18.75 million to $37.5 million contingent on market capitalization achievements.

Concurrently, the termination of the acquisition deal involving Tectu Biz Ltd., initially agreed upon for ~$1 million consideration [S4][S5], highlights operational execution challenges or strategic reassessment in inorganic growth pacing. This mutually consensual withdrawal from the transaction removes expected near-term expansion but reins in integration risk amidst evolving regulatory dynamics.

Agentic AI Platform: Business Model and Product Offering

Global AI’s core proposition is centered on its 'Agentic AI Platform,' designed for enterprises requiring autonomous agents capable of multi-step reasoning, planning, tool usage, and independent task execution across digital and physical domains [S1][S6]. Unlike passive conversational AIs typical in the market, these agentic systems aim to reduce human supervision by delivering active problem-solving capabilities tailored for highly regulated sectors such as banking, insurance, healthcare, and life sciences.

The platform offers not only autonomous operational features but also extensive governance tools essential for compliance management in these sectors—enabling clients to discover, deploy, measure effectiveness, continuously improve their agentic workflows while adhering to strict regulatory mandates such as GDPR and CCPA [S14]. Revenue generation follows a model where enterprises pay for access to integrated solutions combining platform licensing plus potential consumption or outcome-based pricing linked to autonomous agent usage.

Industry Dynamics and Competitive Environment

Global AI operates within a fiercely competitive landscape characterized by several intertwined layers of players [S10][S28]. Foundation model developers represent a concentrated group that train large-scale neural networks forming the substrate for emerging applications. Hyperscale cloud providers supply computational infrastructure alongside managed services hosting these models. Meanwhile, traditional enterprise software incumbents integrate incremental AI capabilities into established solutions competing directly with fast-growing AI-native startups creating fundamentally new software categories anchored in autonomous intelligence.

Regulatory scrutiny has intensified globally with frameworks like the EU AI Act imposing phased compliance deadlines starting August 2026 [S14], complicating deployment timelines and increasing operational compliance costs. In addition to anticipated FTC/DOJ oversight impacting potential acquisitions through Hart-Scott-Rodino clearance requirements [S1], these pressures affect competitive dynamics by slowing M&A activity—particularly around ‘‘killer acquisitions’’ or data moat strategies perceived as anti-competitive.

Strategic Growth Drivers: Organic Development and M&A Program

The company maintains a dual-pronged growth strategy emphasizing robust internal R&D supported by a contracting model employing fourteen senior AI specialists developing secure, scalable agentic-AI solutions [S1][S6]. Parallelly, Global AI operates a strategic M&A program aimed at acquiring complementary businesses that align with its platform roadmap. Targets are rigorously evaluated based on strategic fit within the Agentic AI Platform ecosystem, scalability of technology/business models, recurring revenue strength, customer retention quality, and management team capabilities [S1].

Post-acquisition integration plans focus on sales/marketing scaling enhancements alongside harmonizing technical platforms to leverage synergies while deepening vertical market penetration. However, the recent Tectu deal termination illustrates challenges in identifying suitable targets compliant with evolving regulatory constraints as well as integration risk considerations [S4][S8]. The ability to successfully execute on this strategy will materially influence growth velocity and competitive positioning.

Risks and Operational Constraints: Capital, Integration, Compliance

Substantial risks shadow Global AI’s ambition. Most notably is the company's fragile financial footing: the current ratio stood at an acute 0.05 as of December 2025 indicating severe short-term liquidity pressure relative to liabilities totaling over $5.8 million versus current assets approximating $315k [F1]. Although total debt is manageable ($94k reported mid-2023) compared to cash reserves ($112k near Q3 2025), tight working capital constrains operational flexibility amidst ongoing development investment [F1].

The lack of direct employees heightens dependency on independent contractors which could constrain rapid scaling or coordination during complex integrations post-acquisition [S14][S13]. Furthermore, execution risk includes potential diversion of management attention away from organic innovation due to integration demands.

Regulatory uncertainty adds another layer; compliance obligations under nascent frameworks such as the U.S. Safe Secure Use Orders or EU high-risk system rules present evolving requirements that could restrict feature deployments or impose costly safeguards leading to delayed time-to-market [S14][S24]

Near-Term Watchpoints: Execution Milestones and Market Signals

Key upcoming indicators include progress on closing alternative acquisitions given regulatory clearance complexity by FTC/DOJ authorities [S1][S14], expansion beyond initial Israel commercial contracts signed through its GL AI Ltd subsidiary formed late 2024 [S6], and delivery against Board-defined KPIs tying directly to CEO incentive awards laid out in the May 2026 employment agreement [S3].

Market capitalization thresholds triggering significant equity grants reflect internal valuation targets suggesting management confidence yet also invoke material dilution concerns risking shareholder value erosion if unmet [S3]. Ongoing equity capital raises are critical given 'going concern' doubts stated explicitly in annual filings highlighting funding necessity or risk of curtailed business plans if financing falters [S25][S29].

Financial Overview: Liquidity and Profitability Context

The financial position of Global AI underscores operational vulnerability. As of late 2025 data points reveal revenue generation remains minimal (~$24,896) compared with operating losses surpassing $2.3 million annually reflecting hefty investment in technology development without scaling commercial receipts [F1]. Net losses reached over $2.3 million demonstrating persistent unprofitability.

Cash reserves approximate $112k against sizeable current liabilities exceeding $5.8 million exacerbate liquidity stress with a critically low current ratio near 0.05 signaling working capital insufficiency pressuring day-to-day operations funding [F1]. Total debt levels are relatively low making leverage an immaterial immediate concern but do not mitigate underlying cash burn issues.

This financial snapshot supports analysis that additional capital raises—whether equity or collaborative partnerships—are indispensable for sustaining activities prior to meaningful revenue scale.

Disclaimer: This analysis presents an evaluation based exclusively on sourced SEC filings and company disclosures without providing investment research views or price forecasts.

Financial position in context

Current assets of $315643 and current liabilities of $6mm imply a current ratio near 0.05x for 2025-12-31 [F1]

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments