Galaxy Digital Amplifies Institutional Reach While Scaling AI Infrastructure Amid Regulatory Challenges

Galaxy Digital advances its integrated digital assets and HPC platform, expanding product offerings and data center capacity while managing legal and market risks.

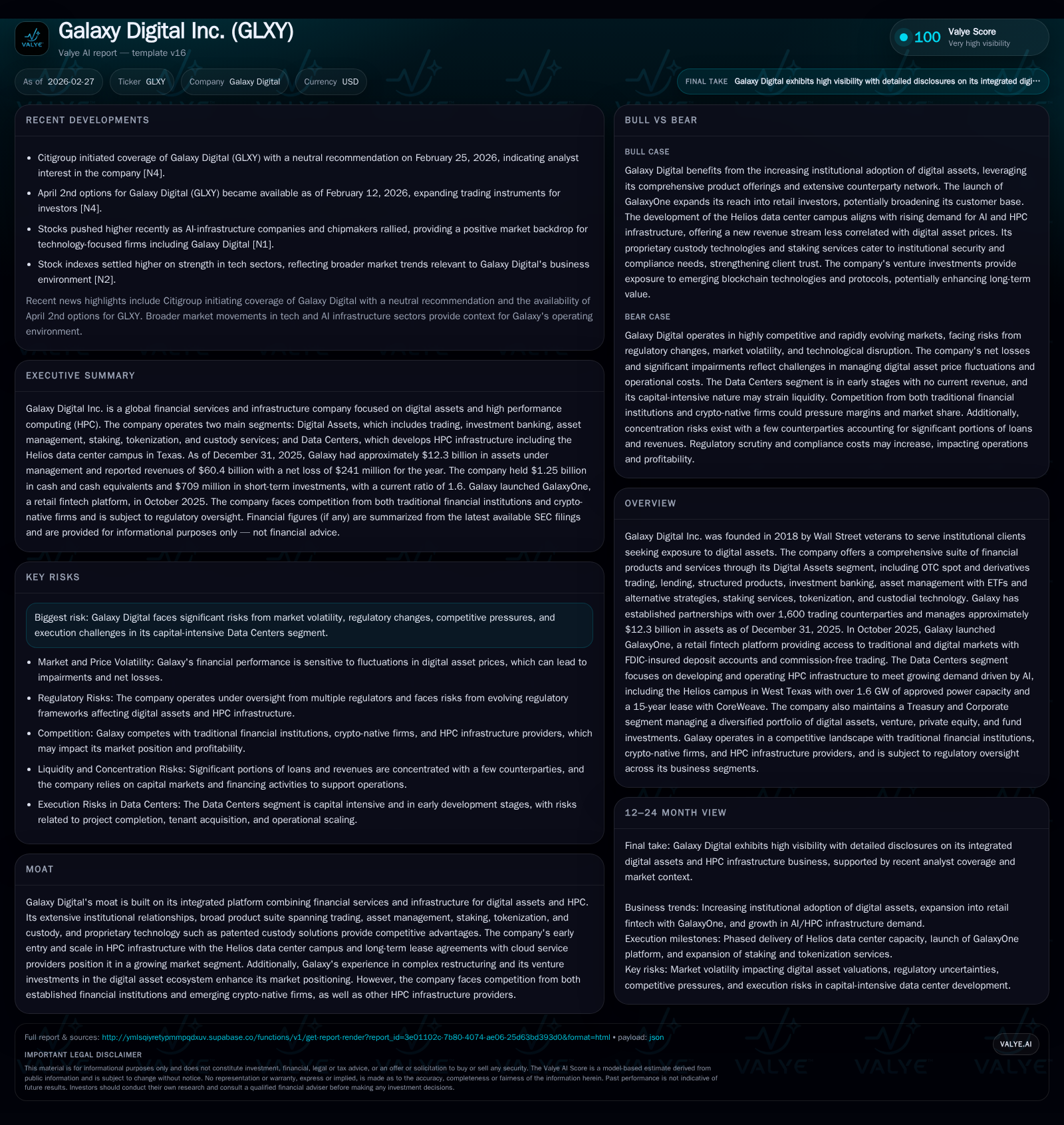

Founded in 2018 by experienced Wall Street professionals, Galaxy Digital has established significant institutional footing across digital assets through comprehensive financial services and infrastructure. As of the end of 2025, its assets under management reached approximately $12.3 billion, complemented by the launch of GalaxyOne retail fintech and the expansion of high-performance computing (HPC) data center infrastructure tied to AI demand. Despite these growth vectors, the company navigates substantial legal contingencies related to past LUNA investments and operates within evolving regulatory frameworks that impact operational costs and compliance requirements. Financially, Galaxy Digital posted revenue exceeding $60 billion in 2025 but recorded a net loss, reflecting heavy reinvestment in technology, data centers, and legal provisions. Capital structure is leveraged via multiple exchangeable notes supporting HPC expansion, with liquidity bolstered by over $1.2 billion in cash and equivalents.

Company Background and Business Overview

Founded in 2018 by seasoned Wall Street veterans anticipating the intersection of traditional finance with emerging digital assets markets, Galaxy Digital Inc. has positioned itself as a global financial services and infrastructure firm catering primarily to institutional investors interested in digital asset exposure [S25]. With headquarters in New York City and dual listing on Nasdaq and Toronto Stock Exchange under ticker "GLXY," Galaxy operates chiefly through two pillars: Digital Assets services and Data Centers dedicated to high-performance computing (HPC), increasingly focused on AI workloads.

The firm offers a full spectrum of institutional solutions including OTC spot and derivatives trading, margin lending, structured product issuance, investment banking advisory (M&A and capital markets), asset management encompassing ETFs plus alternative strategies, staking services, tokenization technologies, custody with proprietary security features like patented custody solutions, as well as a retail fintech platform called GalaxyOne launched in October 2025 that extends FDIC-insured cash deposits alongside commission-free market access across equities and cryptocurrencies [S25], [S3].

Historical Performance Drivers

Galaxy’s growth roots are anchored in leveraging deep institutional relationships—over 1,600 trading counterparties across both crypto-native entities and traditional finance firms—and scaling product breadth to meet diverse client demands from trading through custody [S25]. Strategic acquisitions such as GK8 (secure self-custody technology provider) acquired out of Celsius bankruptcy estates in early 2023 underscored commitment to proprietary infrastructure innovation [S20]. Similarly, acquiring Helios bitcoin mining operations expanded physical infrastructure know-how that now underpins its HPC data center ambitions.

Financially for the calendar year ended December 31, 2025:[F1]

Historical performance (annual)

| FY |

|---|

| 2025 |

Source: SEC companyfacts cache [F1].

Revenue reflects gross proceeds from digital intangible asset sales alongside fee-based income streams from asset management and advisory services [S20]. The net loss reflects substantial investment costs including approximately $1.3 billion toward HPC buildout at Helios facility [S14], legal provisions mainly associated with LUNA litigation settlements (~$151 million accrued end-2025) [S17], plus regulatory compliance expenses [S14], [S17].

Cash on hand nearly tripled from $462 million at end-2024 to $1.25 billion by end-2025 driven by financing activities including equity raises totaling approximately $851 million net of issuance costs as well as over $2 billion raised through exchangeable senior notes to fund innovations particularly at Helios campus [S8], [S14], [S29]. Working capital improvement supported by growing current assets contributed to a current ratio approximating 1.6.

Future Growth Prospects

Galaxy is actively scaling its Digital Assets segment by enhancing its institutional suite—adding staking programs, margin financing options as well as expanding its ETF line-up—and concurrently pushing GalaxyOne retail access which integrates seamlessly with regulated partners offering commission-free trades may drive incremental customer acquisition [N14], [S25]. This diversification aims to capture both institutional mandates seeking regulated exposure along with growing retail interest facilitated by improved user-friendly fintech offerings.

On the infrastructure side, Galaxy’s Data Centers segment focuses heavily on constructing HPC facilities tailored for accelerated AI workloads that demand reliable power supply coupled with scalable compute capabilities at industrial scale—a market poised for rapid growth given AI’s rising adoption [S25]. Continued investments include an outstanding ~$530 million deeded construction commitment on the Helios facility alone as of year-end[S16]. Financing flexibility is maintained by sizable credit facilities including a $1.4 billion senior secured loan facility entered August 2025 supporting the Dickens County Texas data center project fulfilling these HPC needs [S9].

Risks to growth include:

- Regulation changes impacting crypto activities; shifts could require costly operational restructuring or constrain some lines like derivatives trading or staking due to classification debates around digital asset status under securities laws [S21].

- Market volatility inherent to crypto assets affecting trading revenues unpredictably.

- Competitive pressure from expanding traditional finance players entering digital asset markets alongside nimble crypto-native firms offering decentralized alternatives.

- Execution risk related to large capital commitments in HPC infrastructure—timeliness of buildouts versus competition’s cloud hyperscalers critical.

- Ongoing management of legal contingencies tied notably to LUNA class actions with outcomes still uncertain [S11], [S17].

Financial Expectations & Milestones

Explicit forward guidance was not provided; however,[S3] highlights areas to monitor:

- Progression toward ‘Stabilization’ phase for debt covenants linked to Helios credit facility requiring minimum debt service coverage ratios.

- Continued ramp-up metrics around GalaxyOne user adoption rates driving new retail deposit volumes.

- Asset under management growth trajectory amid volatile macroeconomic backdrop influencing digital asset prices.

- Legal outcomes on class action motions scheduled mid-2026 potentially impacting future earnings volatility.

Returns & Capital Allocation Strategy

Galaxy generated negative returns on equity estimated at approximately -12% based on last reported net income relative to equity at year-end 2025[F1]. Free cash flow dynamics reveal meaningful cash burn with approximately -$1.51 billion estimated using operating cash flow less capital expenditures[F1]. Capital allocation activities emphasize raising funds predominantly via equity offerings ($851 million net proceeds) plus debt issuances surpassing $2 billion in recent years fueling expansion needs rather than returning capital via dividends or buybacks [S29]. The company has not declared dividends nor repurchased shares during recent periods per official policy statements [S1].

Competitive Positioning & Moat Analysis

Galaxy’s moat stems from its integrated ecosystem fusing broad institutional-facing financial products with distinctive proprietary technology (patented custody solutions), extensive counterparty network (>1600 counterparties), plus early foothold in developing scalable HPC infrastructure strategically targeted at burgeoning AI workloads[S24], predating many pure-play competitors attempting entry into this niche vertical.

Notwithstanding these strengths,[S24] acknowledges intense competition emanating simultaneously from large traditional banks extending into crypto custodial/trading arenas plus rapidly innovating crypto-natives leveraging decentralized finance protocols circumventing intermediaries. Additionally,HPC infrastructure rivals include hyperscale cloud providers aggressively fighting for share within AI compute demand curves.[S24]

Risks Summary

Besides typical market fluctuations seen across cryptocurrency holdings influencing revenue swings,[S4] elucidates material ongoing risks associated with regulatory shifts particularly involving SEC interpretations classifying certain digital assets or swap transactions which could impose additional compliance burdens or restrict product offerings.[S20] Further,[S11], [S17] depict sustained litigation exposure notably linked to historical LUNA asset involvement producing large settlement accruals affecting balance sheet flexibility.

Operational risks also arise from rapid technological scaling necessities inherent in developing state-of-the-art data centers requiring alignment between capital deployment timing and commercial utilization ramp.[S24]

Conclusion

Galaxy Digital walks a complex yet strategic appeal path combining established institutional digital asset finance leadership augmented by ambitious development of next-generation HPC infrastructure addressing AI computational needs—a confluence positioning it for potential durable competitive relevance provided it successfully manages execution discipline alongside evolving regulatory landscapes. Carefully watching upcoming legal proceedings outcomes alongside performance ramp of GalaxyOne platform usage metrics will be critical near-term indicators.

This analysis is intended for informational purposes only based on publicly available filings and news as of early 2026; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments