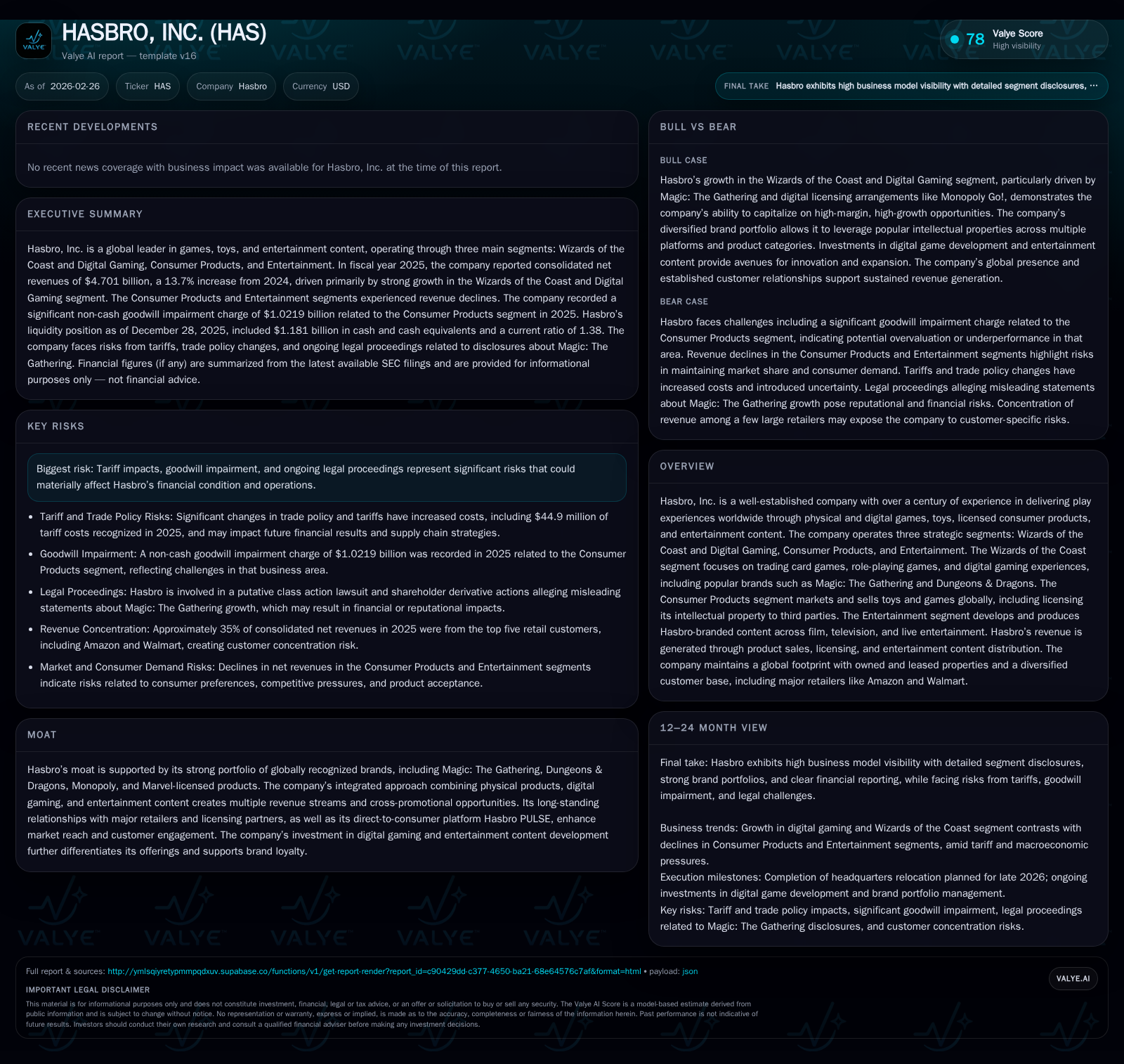

Hasbro’s Growth Slump Amid High-Profile Brand Revitalization Efforts

Hasbro’s recent financial performance reveals a stark contrast between revenue gains and profitability challenges as it pursues an integrated strategy across gaming, consumer products, and entertainment.

Hasbro reported a 13.1% revenue increase in FY2025 driven by growth in digital gaming and steady consumer product sales, yet operating income plummeted by over 98%, primarily due to significant goodwill impairments and asset disposals. The company’s segment performance is mixed: Wizards of the Coast continues to expand while Consumer Products faces impairment headwinds, and Entertainment struggles with non-cash charges. Despite strong operating cash flow and ongoing investments in digital content and brand revitalization, large legal contingencies and tariff pressures pose risks. Capital returns continue via dividends and a fresh $1 billion buyback authorization, though recent share repurchases were dormant.

Revenue Growth and Profitability: A Mixed Performance

Hasbro’s financial results for fiscal year 2025 illustrate a multifaceted story where top-line expansion masks severe bottom-line erosion. Total revenues reached approximately $5.37 billion, marking a 13.1% increase year-over-year from the prior year’s $4.75 billion [F1]. This rebound reflects sustained growth momentum particularly within the Wizards of the Coast (WotC) segment alongside stable consumer product sales outside North America.

Contrasting these revenue improvements is an operating income collapse from $690 million in 2024 down to just $11 million in 2025 — an alarming decline of nearly 98.4% [F1]. Net earnings swung into negative territory at around -$322 million versus positive net income of $386 million last year, representing a plunge of over 183% [F1]. The precipitous drop is primarily attributable to non-cash items including substantial goodwill impairments concentrated in Consumer Products ($1+ billion) alongside losses associated with the divestiture of entertainment businesses as detailed in segment disclosures [S9].

EBITDA metrics exhibit similar stress reflecting these exceptional items in concert with amplified operating costs tied to marketing campaigns and content development initiatives.

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 5.4 | -322 | 893 | 11 | +13.1% | -183.6% |

| 2024 | 4.7 | 386 | 847 | 690 | -5.1% | +125.9% |

| 2023 | 5.0 | -1489 | 726 | -1539 | -14.6% | -831.8% |

| 2022 | 5.9 | 204 | 373 | 408 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 393 | 830 | |

| 2024 | 390 | 0 | 760 |

| 2023 | 388 | 0 | 516 |

| 2022 | 385 | 125 | 199 |

Source: SEC companyfacts cache [F1].

Data reflect continuing operations; impairment charges heavily distort profitability metrics [F1], [S9].

Strategic Segment Deep Dive: Wizards of the Coast, Consumer Products & Entertainment

Hasbro operates through three principal segments each contributing distinct dynamics:

Wizards of the Coast and Digital Gaming: This segment generated net revenues of approximately $2.19 billion in FY2025—a sharp rise from about $1.51 billion in FY2024—propelled by continued strength in both tabletop games like Magic: The Gathering (MTG) and role-playing games such as Dungeons & Dragons alongside digital platforms [S12], [S17]. Operating profit here was robust at roughly $1 billion before corporate allocations, reinforcing WotC’s position as a key growth driver [S17]. However, ongoing litigation alleging misleading representations around the segmentation strategy for MTG introduces legal uncertainties that may affect brand perception or require future reserves [S1].

Consumer Products: This historically core business saw net revenues decline slightly to about $2.44 billion from approximately $2.54 billion prior year amid macroeconomic headwinds and competitive pressures [S12]. Furthermore, Hasbro recorded aggregate pre-tax goodwill impairments close to $1.02 billion against regional reporting units focused on North America and Europe driven by discounted cash flow recalibrations incorporating tariff impacts and softer market demand [S22], [S24]. Management cautions that continued economic volatility could necessitate further adjustments.

Entertainment: Contributions shrank considerably due to structural changes including the completion of eOne Film & TV business sale at end-2023 which reduced FY2025 revenues for film/TV dramatically from prior years [$10 million vs hundreds previously] [S12], [S25]. Additionally, this segment absorbed a non-cash goodwill impairment charge exceeding $1.19 billion alongside losses totaling over half a billion dollars from asset sales further eroding EBIT [S9]. Core family brands held up better with positive fair value measures indicating some resilience.

Intersegment synergies exist mainly through intellectual property licensing agreements enabling cross-promotion between physical toys/games and digital content as well as entertainment offerings; however, these have not yet translated into offsetting profit gains amid recent disruptions.

Digital Transformation and Content Investments: Future Growth Levers or Cost Centers?

The Company emphasizes an integrated approach combining physical products, digital gaming capabilities via Wizards of the Coast digital titles plus licensing third-party developers, complemented by original entertainment content creation under its Entertainment segment , [S9], [S13].

Management views digital innovation—particularly expansions around Magic: The Gathering Arena and new Dungeons & Dragons virtual tools—as critical for long-term engagement but acknowledges development expenses inflate cost bases near term without guaranteed returns given market competition intensifying globally , [S13].

Meanwhile, substantial impairment charges related to eOne Film & TV indicate that content investments carry notable execution risk despite potential franchise value extraction plans going forward [S9]. The ongoing legal scrutiny relating to purported segmentation tactics affecting investor confidence adds complexity.

Ultimately these initiatives aim to deepen brand loyalty via diversified revenue streams but require monitored capitalization on scaling opportunities while containing margin pressure.

Financial Health: Liquidity, Debt Structure, and Capital Resources

At fiscal year-end December 28, 2025 Hasbro held approximately $777 million in cash and cash equivalents complemented by short-term investments worth around $105 million alongside total long-term debt exceeding $3.28 billion spread across maturities from near term through mid-2040s [F1], [S4].

The company maintains access to sizeable credit facilities including a revolving credit agreement initially providing up to $1.25 billion—recently amended extending maturity through February 2031—with covenants consistent with investment grade thresholds such as maintaining consolidated interest coverage ratio above 3x and total leverage ratios below specified limits varying quarterly between roughly 3.75–4x EBITDA equivalents [S4], [S6], [S8]. As of year end no borrowings were outstanding under this facility though letters of credit approximating $3.3 million remained active supporting international operations.

Tariff expenses contributed nearly $45 million headwind embedded within cost of sales underscoring supply chain exposure given geographic sourcing footprints spanning North America, Asia Pacific regions among others [S4], [S26]. The company operates a supplier finance program enhancing working capital efficiency without balance sheet liability transfer [S16].

Overall liquidity ratios remain healthy with current ratio near 1.38 reflecting manageable near-term obligations relative to liquid assets; however residual risks from macro volatility may test capital flexibility if operating losses persist.

Capital Allocation Policy: Dividends, Share Buybacks, and Investment Priorities

Throughout recent years Hasbro consistently returned capital via steadily increasing quarterly dividends totaling approximately $392 million distributed during FY2025—largely aligned with positive operating cash flow generation though major impairments affect reported earnings negatively undermining return on equity which stood near -10.8% for fiscal year ending December 2025 based on net losses relative to equity reported previously circa early FY20s levels [F1], [S7], [S20].

While no share repurchases occurred throughout FY2025 contrasting earlier smaller buyback transactions ($125 million repurchased back in FY2022) management secured a fresh authorization for up to $1 billion shares with no set expiration allowing opportunistic deployment depending on market conditions going forward [S7], [S15]. Investment priorities remain centered on digital capability expansion balanced cautiously against overhead rationalization post eOne exit.

Cash conversion remains robust supported by stable operational cash flows exceeding capex spending considerably facilitating sustained dividend distributions absent excessive leverage escalation risks.

Navigating Risk: Tariffs, Litigation, and Goodwill Impairment

Hasbro acknowledges multiple prominent risk factors prominently disclosed including material tariff-related cost increases impacting gross margins ($44.9 million identified for calendar year 2025 alone), ongoing securities class action litigation filed alleging misrepresentations related to growth narratives around Magic: The Gathering segmentation strategy spanning September 2021–October 2023 periods leading to motions dismiss pending February 2026 with outcomes still uncertain potentially exposing the company financially or reputationally [S1], [S29].

Goodwill impairment risks remain acute following significant non-cash write-downs during fiscal year 2025 exceeding one billion dollars localized mostly within Consumer Products regional reporting units alongside Entertainment family brands albeit assessed above carrying values at measurement date suggesting moderate cushion currently maintained but subject to economic fluctuations affecting future valuations [S22], [S24].

These expose earnings volatility unrelated directly to cash operations but materially effect investor perceptions especially when aggregated with legal uncertainties.

What to Watch Next: Key Milestones and Potential Catalysts

Given absence of formal forward guidance disclosed within recent filings or press releases monitoring upcoming quarterly results post-restatement triggered by credit agreement amendments will be critical—particularly observing margins recovering beyond exceptional charge normalization along with integration efficacy following relocation of Toy & Game headquarters scheduled Q4 2026 impacting operating costs structurally could shift profit narratives meaningfully [N3], [S3], [S1].

Progress in litigated matters is vital given potential financial provisions required or reputational impact influencing brand valuation long-term.

Investor focus should also center on measurable returns on investments targeted at expanding digital gaming ecosystems (e.g., MTG Arena enhancements) plus monetization approaches within direct-to-consumer platforms such as Hasbro PULSE that aggregate customer engagement insights feeding back into product innovation cycles.

Macroeconomic effects including trade policy shifts or currency fluctuations will continue warranting cautious outlook adjustments given global revenues comprise sizable shares outside U.S markets driving sensitivity.

This analysis is based solely on publicly available SEC filings dated through February 26, 2026 ([F1],), company narrative excerpts () ,and does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments