J M Smucker Faces Margin Pressure But Reinforces Brand Portfolio

Recent impairment charges and liquidity challenges highlight strategic pivots within J M Smucker's core segments.

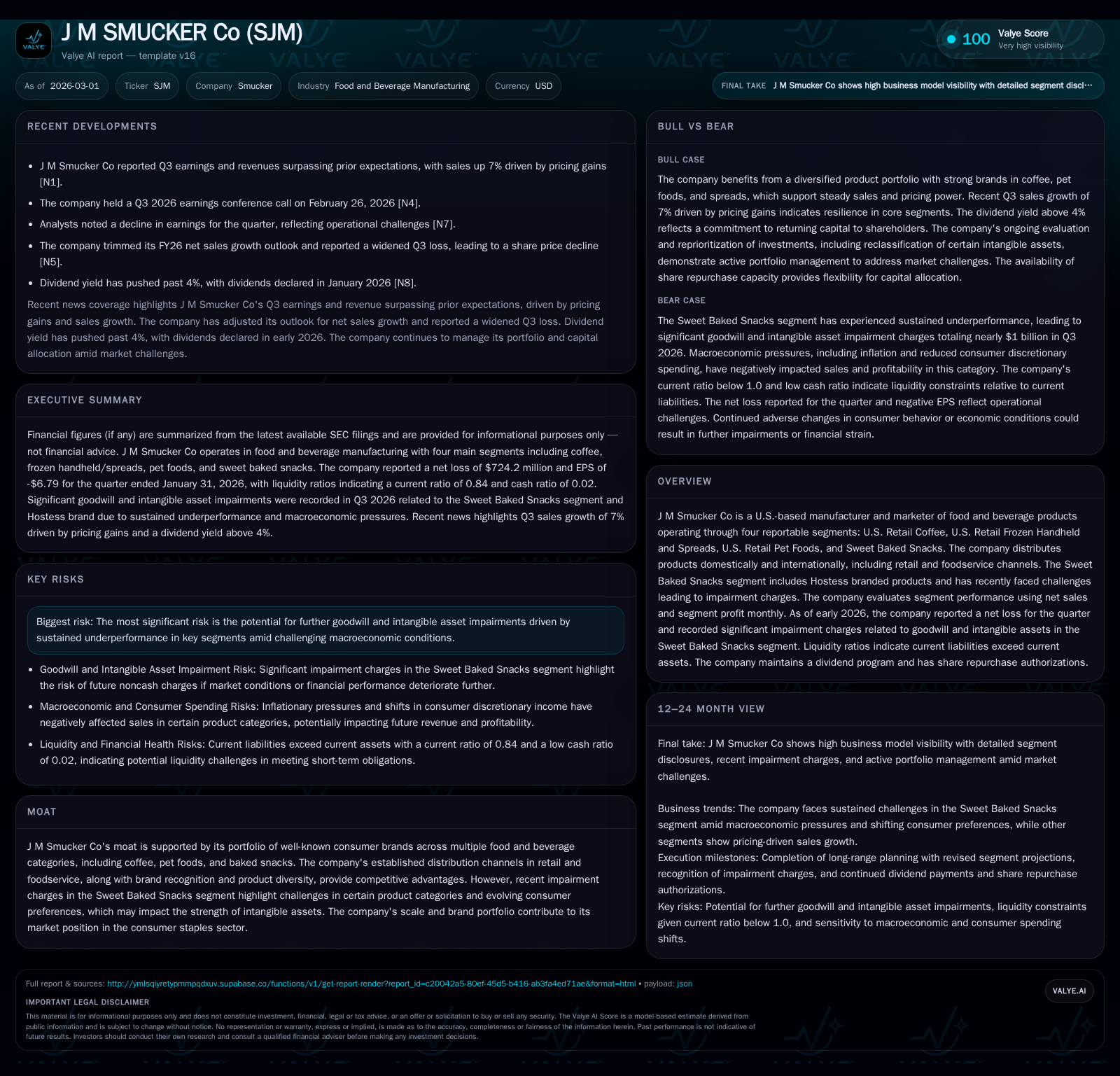

J M Smucker Co, known for its iconic consumer brands in coffee, pet foods, and baked snacks, has reported significant impairment charges primarily impacting its Sweet Baked Snacks segment. These financial headwinds have contributed to a sharp contraction in operating and net income in the latest fiscal years. Despite these challenges, the company’s U.S. Retail Coffee and Pet Foods segments remain strong pillars with substantial intangible asset backing, preserving the overall brand moat. Meanwhile, liquidity strains reflected in a subdued current ratio necessitate cautious capital allocation, balancing dividends with limited share repurchases and reduced capex. Management’s trimmed sales outlook for FY26 underscores risks tied to evolving consumer trends and macro pressures affecting discretionary categories.

Iconic Brands Under Pressure: Overview of Segment Performance

J M Smucker Co operates through four principal segments: U.S. Retail Coffee, U.S. Retail Frozen Handheld and Spreads, U.S. Retail Pet Foods, and Sweet Baked Snacks. The company's competitive moat rests on its portfolio of well-established consumer brands across these categories supported by robust retail and foodservice distribution channels [S2]. However, recent quarterly disclosures reveal marked pressures particularly in the Sweet Baked Snacks division — home to Hostess-branded products — which encountered sustained sales and profitability declines due to evolving consumer preferences away from sweet baked goods amid inflationary constraints on discretionary spending [S2]. This necessitated an interim impairment analysis during Q3 2026 resulting in a full write-down of goodwill associated with that segment and reclassification of the Hostess brand as a finite-lived intangible asset.

The impairment charge eliminated all remaining goodwill in Sweet Baked Snacks, signaling severe valuation reset and highlighting executional challenges alongside slow category recovery [S2]. In contrast, U.S. Retail Coffee and Pet Foods segments retain approximately 80% of total goodwill carrying value ($2.1 billion and $1.6 billion respectively), underscoring their relative stability within the portfolio despite increased market competition [S2]. These facts illustrate a dichotomy within the company: while some core brands maintain enduring value-based moats, others face acute headwinds threatening their intangible asset recoverability.

From Growth to Contraction: Historical Financial Trends and Drivers

J M Smucker’s historical financial trajectory exhibits significant volatility driven by operational setbacks coupled with noncash impairment events. The company reported operating income of $1.02 billion and $157 million for fiscal years 2022 and 2023 respectively, before a stark reversal yielding a negative operating income of approximately -$674 million in FY2025 — a decline of over 151% year-over-year [F1]. Net income followed an even more pronounced pattern falling from positive territory ($631 million in FY2022) to a net loss exceeding $1.23 billion for FY2025 (-265% YoY) [F1].

Despite this earnings compression, operating cash flow remained relatively stable near $1.2 billion annually through FY2025, indicating underlying cash generation ability separate from accounting charges [F1]. Capital expenditures waned sharply from $586 million in FY2024 to about $394 million (a nearly 33% drop), reflecting tightened investment discipline amid profitability uncertainties [F1]. Shareholders’ equity contracted from approximately $7.69 billion in FY2024 to $6.08 billion at the end of FY2025 consistent with accumulated losses including impairments [F1].

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | -1231 | 1210 | -674 | 394 | -265.4% |

| 2024 | 744 | 1229 | 1306 | 587 | +914.9% |

| 2023 | -91 | 1194 | 158 | 477 | -114.5% |

| 2022 | 632 | 1136 | 1024 | 418 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 455 | 3 | 817 |

| 2024 | 438 | 373 | 643 |

| 2023 | 430 | 368 | 717 |

| 2022 | 418 | 270 | 719 |

Source: SEC companyfacts cache [F1].

*FY2025 figures represent the most recent fiscal year ended April 30 per latest SEC filings [F1].

Sweet Baked Snacks Segment: Impairment Impact and Strategic Response

Segment-level disclosures from the February 2026 Form 10-Q detail continued underperformance in the Sweet Baked Snacks segment attributed to "ongoing executional and operating challenges" compounded by a "dynamic macroeconomic environment," including regulatory developments straining category economics [S2]. Revised long-range planning lowered projected net sales and segment profit compared with estimates used during prior impairment assessments quarter-end Q4-25 revealing deteriorating cash flow visibility within this segment.

The Hostess brand underwent reclassification from indefinite-lived goodwill into finite-lived intangible classification reflecting management's revised view on asset life amid falling consumer demand patterns away from traditional baked goods categories subject to inflation-induced discretion reduction [S2]. This constellation of pressures triggered noncash impairment charges substantially curtailing net worth allocated to this reporting unit emphasizing sector-specific cyclicality vulnerability.

Coffee and Pet Foods Segments as Anchors in a Shifting Portfolio

By contrast to Sweet Baked Snacks turmoil,J M Smucker’s U.S. Retail Coffee segment carries $2.1 billion of goodwill while its Pet Foods operations hold roughly $1.6 billion centered primarily on intangible assets such as trademarks that support these businesses’ competitive positioning [S2]. These segments reflect core earnings engines behind recent pricing gains that contributed positively to Q3 revenue growth per news reports [N1], suggesting resilience amid broader macroeconomic constraints affecting discretionary consumer spend.

Preserving these assets is critical given their contribution toward over four-fifths of total goodwill value reported early-2026; thus safeguarding brand equity here is fundamental to sustaining enterprise valuation floor despite losses elsewhere [S2],[F1]. Segment profits in these areas have fared better comparatively but require monitoring given ongoing input cost inflation dynamics.

Liquidity Snapshot: Current Ratio and Capital Structure

Liquidity indicators show modest stress as current assets totaled approximately $1.99 billion versus current liabilities around $2.36 billion at January-end reflecting a current ratio near a concerningly low level of ~0.84 signaling short-term coverage inadequacy without relying on longer-dated funding structures or working capital improvements [F1],[S2].

The debt profile remains weighted toward long-dated senior notes totaling over $7 billion including multiple tranches maturing between late-2027 through mid-2050 backed by credit facilities featuring ample revolving capacity totaling $2 billion unused as per latest reports [S5][S6][S8]. The Term Loan instrument drawn fully in March ’25 carries an interest rate near mid-5% levels requiring ongoing interest expense funding commitments with amortization not scheduled before maturity March ’27 maintaining principal balance via bullet repayment structure [S5][S6]. Compliance with covenant metrics such as interest coverage has been affirmed as of late-2025 filings despite operating volatility demonstrating creditor confidence thus far [S16].

The company also employs commercial paper backed by revolving credit facilities used short-term for working capital needs evidenced by outstanding balances fluctuating between ~$640 million and ~$950 million across quarterly periods with weighted average borrowing costs above four percent reflective of market rate environment changes post-pandemic tightening phases [S5][S8][S19].

Capital Allocation Dynamics: Dividends and Repurchases

Despite confronting accumulated deficits due notably to impairments and operational losses offsetting earlier profits,[F1] J M Smucker continues paying regular cash dividends maintaining yields north of four percent appealing to income-focused investor bases especially when juxtaposed against high-grade staples peers' yields [N11],[S4].[S29] Fiscal year dividend outlays slightly increased YoY nearing $455 million to sustain shareholder returns amidst adversity while share repurchase activity nearly halted with only approximately $3 million spent for FY25 compared with hundreds of millions previously reflecting prioritization toward liquidity preservation over aggressive capital return programs.

Capital expenditure reductions (~33% YoY cut) completed down to approximately $394 million reinforce an operational tightening dynamic intending expenditure discipline amid dampened near-term growth expectations consistent with cautious stewardship strategy described by management at recent earnings calls [F1],[S25],[N10].

Future Trajectory: Management Guidance and Market Risks

In their February earnings communication managing expectations for full-year fiscal ‘26 results saw revised downward projections for net sales growth citing persistent sluggishness in discretionary categories like sweet baked goods potentially extending recovery timelines outside original plans framed last quarter.[N10][S2] This tempered guidance incorporates macroeconomic risks including inflationary pressures impacting consumer purchasing power plus regulatory uncertainties influencing compliance costs or product formulations affecting the Sweet Baked Snacks reporting unit significantly.

Moreover,"a material impairment risk remains if adverse conditions persist," warns SEC risk disclosure highlighting vulnerability residing chiefly around intangible asset recoverability should further prolonged underperformance transpire threatening future noncash charges impacting net equity foundationally.[S2]

Key Metrics to Monitor Going Forward

Investors should watch upcoming earnings for signs of stabilization or turnaround including segment profit margins especially from impaired baked snacks operations alongside steady or improving cash flow generation metrics indicative of operational resilience.[N3],[N10],[S2] Liquidity status updates through current ratio trends plus debt refinancing or amortization activities will illuminate balance sheet flexibility while management commentary on any shift in capital return strategies could signal evolving confidence levels.

Market reactions post-reports might further clarify how stakeholders assess risk-return tradeoffs inherent at this juncture when assessing J M Smucker’s equity story after recent shakeups.[N9]

This analysis is based solely on publicly available documents without investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments