Hecla Mining's Strategic Transition and Portfolio Resilience in Q1 2026

Hecla Mining advances its Casa Berardi divestiture while leveraging strong liquidity and diversified metal exposure amid lower-than-expected Q1 earnings.

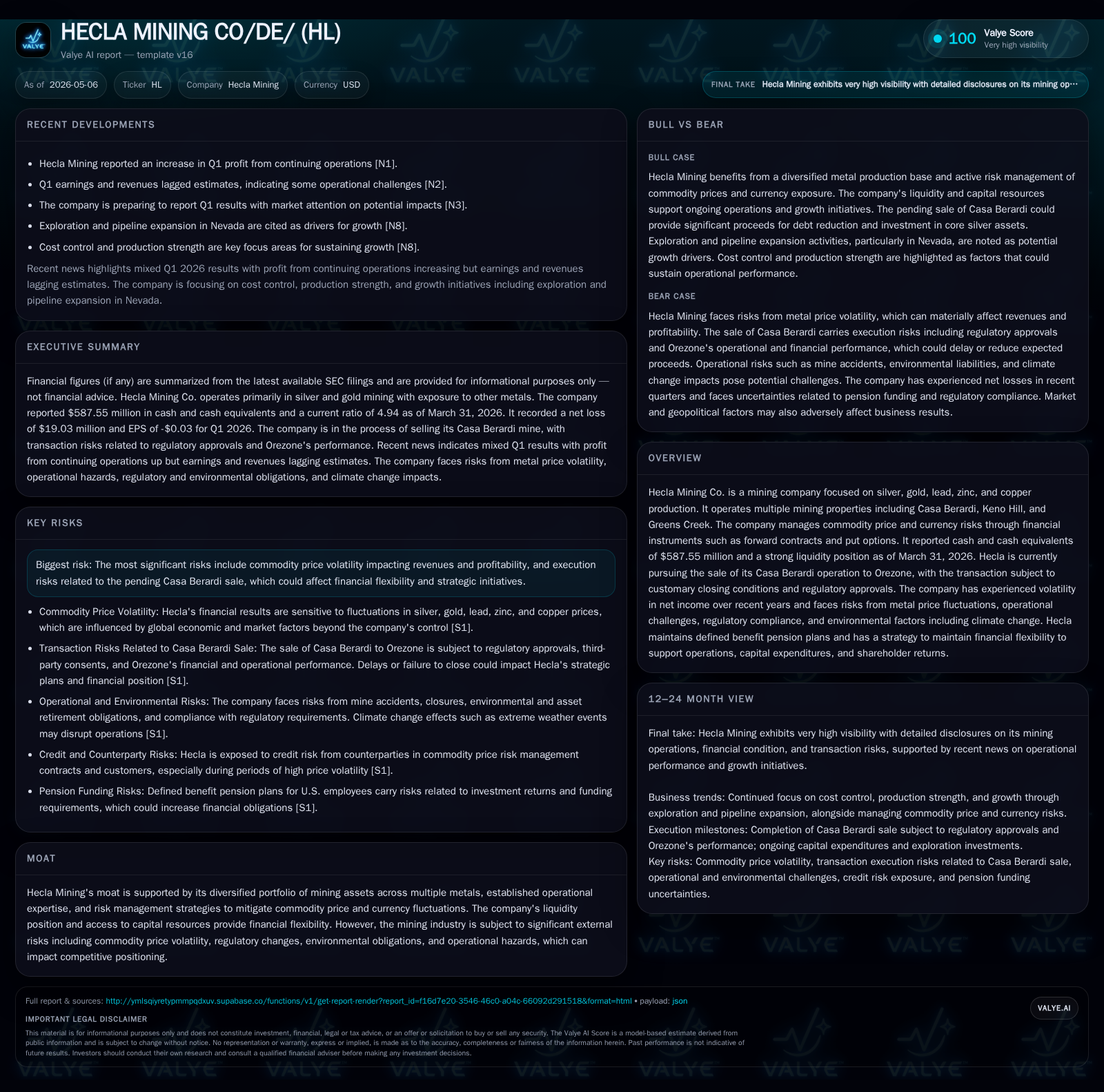

In the first quarter of 2026, Hecla Mining has initiated the strategic sale of its Casa Berardi gold operation to Orezone, signaling a shift toward portfolio optimization. Despite Q1 revenues and earnings lagging estimates, the company retains robust liquidity with cash reserves near $588 million and a healthy current ratio, supporting operational stability. Its diversified metal production—silver, gold, zinc, lead, copper—and active commodity price hedging underpin margin resilience despite ongoing commodity price volatility. Execution risks related to the asset sale and regulatory approvals remain key near-term considerations for Hecla’s financial flexibility and growth trajectory.

Q1 2026 Operating Update: Key Developments and Implications

Hecla Mining's latest quarterly filing dated May 5, 2026 (Form 10-Q) discloses that the company’s Q1 financial results fell short of revenue and earnings expectations cited by Nasdaq reports [N1], highlighting ongoing operational challenges as it navigates portfolio reshaping. Revenues from metals production were impacted by provisional sales pricing adjustments amid volatile commodity markets. The company has also formally announced in an 8-K event filing on the same date that it is advancing the sale of its Casa Berardi operation to Orezone Mining Corp., expected to receive approximately 65.7 million Orezone shares valued at about $112 million subject to closing conditions and regulatory approvals [S2][S3][S1]. This transaction signifies an important strategic pivot that aims to streamline Hecla's asset base towards properties with higher-margin potential or growth profiles.

Operationally, Hecla continues managing metal production volumes across multiple jurisdictions while dealing with costs pressures from labor and permitting environments. The lag in earnings relative to estimates points toward transient disruptions potentially linked to ramp-up expenditures or timing mismatches in sales settlements. Yet, the company's cash position remains strong—acting as a buffer against these near-term headwinds.

Business Model and Product Portfolio: Metals Mix and Revenue Drivers

Hecla Mining operates as a diversified precious metals producer with strategic exposures primarily in silver but also significant output in gold, zinc, lead, and copper. The company's business model monetizes by-products through concentrate shipments sold directly under long-term customer arrangements where revenue recognition occurs upon shipment with subsequent price adjustments as final settlement prices are determined [S1]. This provisional sales accounting introduces revenue volatility based on fluctuating commodity prices between shipment date and settlement.

To mitigate such earnings variability from metals price swings—particularly for silver, gold, zinc, and lead—Hecla employs financially-settled forward contracts alongside put options covering a sizeable portion (up to 75%) of planned metal exposure over up to five years [S1]. These derivatives stabilize margins by defining minimum realized prices albeit at the cost of capping upside during favorable spot markets.

Each metal stream contributes uniquely: silver remains the core revenue driver given its volume; gold provides diversification into bullion markets; zinc and lead supports additional margin layers through industrial metal demand cycles; copper presence supplements overall product mix balance. The company's ability to convert resources via exploration success into proven reserves sustains revenue drivers over longer horizons.

Industry Ecosystem: Competition, Pricing Dynamics, and Supply Chain Realities

Within the mid-tier precious metals mining sector, Hecla contends with peers like Coeur Mining who similarly balance growth through organic expansions and asset sales or acquisitions [N3]. Commodity price dynamics primarily influence competitive positioning—price swings can swiftly compress or expand margins given high fixed-cost structures in mining operations.

Treatment charges—fees paid for smelting and refining concentrates—are critical cost components influenced by market demand for processing capacity; increases here erode realized metal prices post-sale. Supply chain constraints affecting mining equipment availability or skilled labor shortages impose cost inflation risks affecting production efficiency.

Environmental compliance costs have been rising steadily due to intensifying regulations aimed at managing mine reclamation obligations as well as addressing climate-change externalities. These factors collectively pressure unit economics across competitors but also create barriers tied to permitting cycles that favor incumbents like Hecla with established operational footprints.

Growth Opportunities: Exploration, Asset Optimization, and Market Exposure

Key growth initiatives comprise Hecla’s ongoing exploration programs notably in Nevada where resource delineation efforts aim to convert exploration targets into economically mineable reserves [N13]. Expanding existing pipelines around core mines offers potential to extend mine life or increase throughput.

The prospective sale of Casa Berardi will free financial resources potentially earmarked for higher-return projects or debt reduction enhancing balance sheet flexibility for capital deployment. Concurrently, Keno Hill’s ramp-up phase represents a critical phase transitioning from development into commercial production which if successful will materially add ounces mined annually.

These growth angles hinge closely on measured KPIs: capital expenditure absorption rates on exploration spend reported in filings; timelines for completing major asset divestitures; steady or improving production figures from commissioned sites.

Challenges and Risks: Commodity Volatility, Asset Sales Execution, and Regulatory Factors

Volatile metals pricing remains the foremost risk affecting Hecla’s financial outcomes given direct impact on revenue per ounce/pound realized after derivative adjustments [S1]. The provisional pricing model exposes results further when final settlements diverge significantly from shipment-date assumptions.

The pending Casa Berardi sale carries execution risk tied to customary closing conditions—any delays could constrain liquidity refresh or slow strategic reallocation efforts [S3]. Regulatory scrutiny including approval timelines adds uncertainty to transaction closure chronology.

Additionally, mine safety incidents remain inherent operational hazards potentially curtailing output or inflating costs through remediation needs. Escalating environmental regulations introduce incremental expenditures influencing cost curves for existing assets requiring ongoing compliance investments.

Monitoring Indicators: Upcoming Catalysts, Closing Conditions, and Operational Milestones

Market participants should closely monitor updates regarding the completion of Casa Berardi’s sale process including any disclosures detailing progress on regulatory clearances or contractual amendments [S3]. Fluctuations in benchmark silver and gold spot prices will meaningfully affect provisional sales valuations seen in quarterly reporting cycles.

Operational reporting on Keno Hill’s production rate progression provides a tangible gauge on ramp efficiency impacting overall company output volumes. Additionally, any commentary from management regarding exploration findings or capital allocation shifts will be critical signals for directionality in growth potential.

Financial Snapshot: Liquidity Status and Capital Structure Overview

Latest financial snapshot

| Metric | Value | Period |

|---|---|---|

| Cash & equivalents | $588mm | |

| 2026-03-31 | ||

| Current assets | $958mm | |

| 2026-03-31 | ||

| Current liabilities | $194mm | |

| 2026-03-31 | ||

| Current ratio | 4.94x | |

| 2026-03-31 |

Source: SEC companyfacts cache [F1].

As of March 31, 2026 end-period data shows Hecla Mining holding $587.55 million in cash & equivalents with current assets totaling approximately $957.64 million against current liabilities near $193.85 million yielding a current ratio of approximately 4.94—a strong indicator of short-term financial strength capable of funding working capital needs comfortably without dependency on credit lines [F1][S2].

Prior reported total debt stood around $586.7 million as of late 2019 but net debt effectively rounds near zero today reflecting ample cash coverage [F1]. This liquidity buffer supports Hecla’s exploration programs and general corporate activities amid ongoing metal price fluctuations.

This analysis emphasizes Hecla Mining’s multifaceted approach balancing asset portfolio realignment through the Casa Berardi sale while maintaining robust financial health supported by diversified metal production streams and active commodity risk management strategies. Notwithstanding pressures from commodity volatility and execution uncertainties tied to asset divestitures, Hecla’s liquidity stance underpins flexibility necessary for seizing growth opportunities embedded in exploration advances and operational efficiencies at newer mines such as Keno Hill.

Disclaimer: This report is prepared solely for informational purposes based on publicly available SEC filings (), news sources (), and validated financial data ([F1]). It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments