Houlihan Lokey's Strategic Leap: Robust Earnings and European Market Expansion Amidst Technical Volatility

Analyzing Houlihan Lokey’s Q3 2026 earnings surge alongside aggressive European expansion against a backdrop of uneven market sentiment.

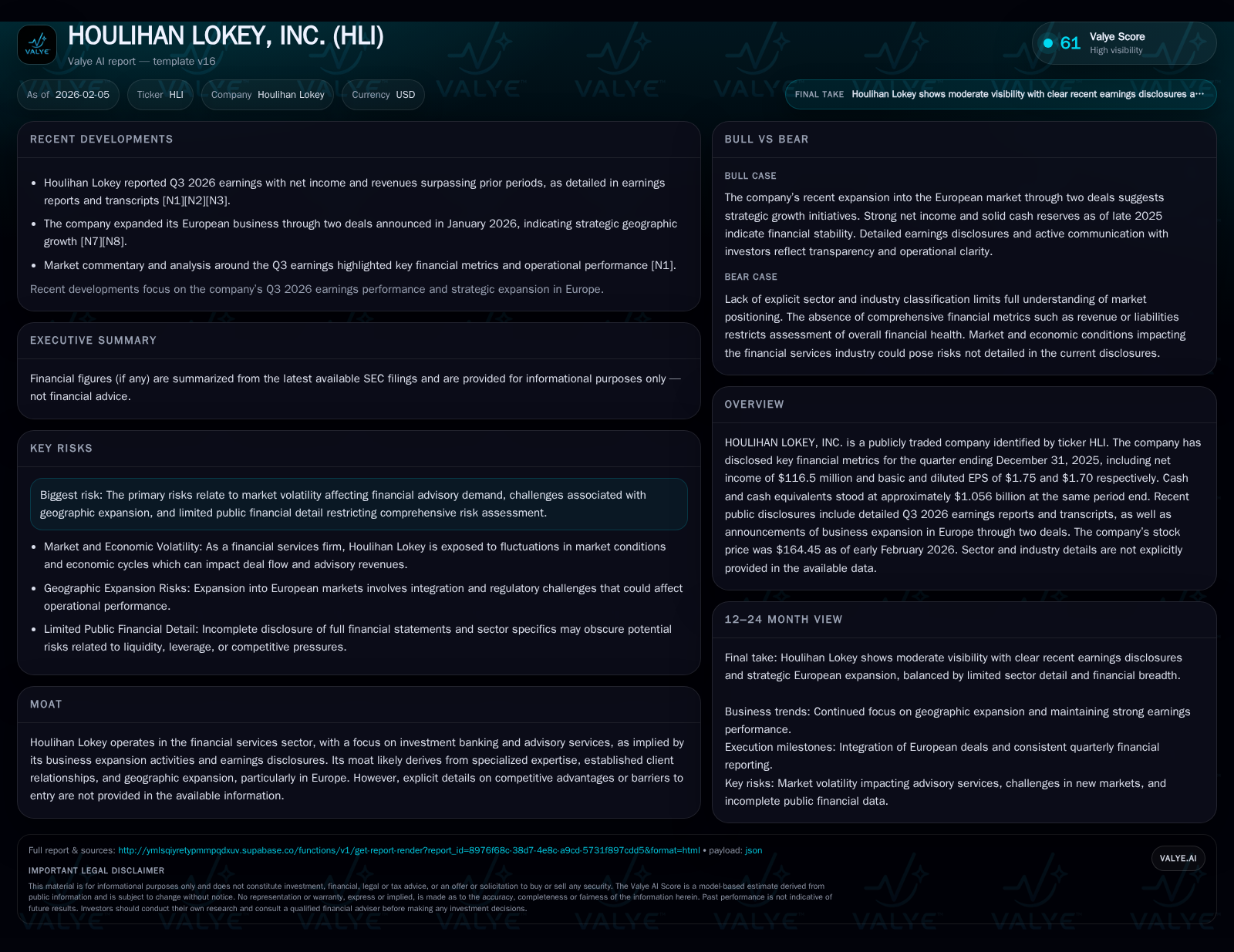

Houlihan Lokey (HLI) delivered impressive Q3 2026 financial results with net income of $116.5 million and EPS surpassing estimates, signaling strong operational execution. Concurrently, the firm advanced its European footprint through two key deals, potentially extending its global advisory reach and diversifying geographic risk. Yet, its stock recently dipped sharply into oversold technical territory, reflecting cautious investor sentiment despite fundamental strength. Balancing robust cash reserves and a specialized advisory moat, HLI faces risks from market volatility and integration complexities as it positions for sustainable growth.

Surging Q3 Earnings: A Closer Look at HLI's Financial Health

Houlihan Lokey reported a net income of $116.5 million for Q3 ending December 31, 2025, supported by basic and diluted EPS of $1.75 and $1.70 respectively—both figures outstripping market expectations [F1][N1][N2][N3]. This results from a well-executed revenue mix where advisory fees benefitted from resilient deal flow despite pockets of market volatility noted during the quarter. The earnings transcript points to disciplined cost management alongside top-line expansion as key drivers underpinning profitability gains [N2]. While specific revenue line items were not fully detailed publicly, the consistent EPS beat signals underlying momentum that is not solely reliant on transient market conditions.

European Expansion: Deals That Broaden the Advisory Footprint

In parallel with its earnings strength, Houlihan Lokey announced two deals concretely expanding its presence in Europe [N10][N11]. These transactions effectively diversify the company’s geographic revenue base beyond traditional U.S. markets. European financial advisory is competitive yet fragmented, allowing HLI to leverage its brand and specialized expertise to carve out incremental share. Geographic diversification reduces reliance on any one regional economy and dilutes idiosyncratic risks tied to domestic market cycles.

However, integration risk looms as a logical consequence; meshing different corporate cultures, systems, and regulatory regimes can incur transitional costs or delays in expected synergies. There is no explicit disclosure on integration timelines or hurdles yet available publicly but cautious monitoring will be warranted as these expansions unfold.

Market Sentiment vs. Fundamentals: Navigating Oversold Territory

Contrasting its fundamentally sound performance, HLI’s stock price encountered sharp downward pressure recently, crossing below critical moving averages such as the 200-day mark before entering technically oversold conditions [N8][N9][N12]. Earlier bullish enthusiasm indicated by a prior upward cross gave way to profit-taking or broader sector-related selling pressures.

This divergence underscores a nuanced interplay where short-term technical factors seemingly discount strengths visible in quarterly results. Investor caution may stem from concerns about macroeconomic headwinds impacting deal volumes or financial services firms broadly. The trading patterns highlight how equity prices can deviate from intrinsic value proxies in volatile environments—a challenge for stakeholders interpreting signals from both fundamental reports and chart analytics.

Balance Sheet Strength: Cash Reserves Fuel Flexibility

One of Houlihan Lokey’s structural advantages lies in its strong liquidity position: $1.056 billion in cash and cash equivalents as of year-end 2025 offers considerable runway for opportunistic investments or cushioning during uncertain periods [F1]. Such a cash buffer is particularly valuable given ongoing expansion initiatives abroad which may necessitate capital deployment.

Moreover, this level of liquidity equips the firm to absorb episodic earnings fluctuations without destabilizing operations or forcing distressed asset sales—an important consideration given cyclical risks inherent in investment banking businesses.

Operational Moat: Specialized Expertise and Client Relationships

Though direct statements on competitive moats are absent in public filings, synthesis of reported activities infers that Houlihan Lokey garners advantage from deep advisory specialization coupled with longstanding client trust [valye_report_excerpt]. Its focus on middle-market M&A advisory and restructuring differentiates it from larger bulge bracket banks often targeting bigger-ticket mandates.

Client loyalty built over years enhances deal pipeline visibility while geographic extension into Europe could further entrench HLI’s network effects. This niche positioning likely creates meaningful barriers for new entrants who must replicate both reputation depth and sector insight simultaneously.

Risks in Focus: Market Volatility and Expansion Challenges

The company’s most salient risks revolve around demand swings tied to broader economic cycles affecting merger activity—as documented in the mandated SEC risk disclosures [S2]. A cooling macro environment or credit tightening could substantially dampen transaction volumes.

Additionally, the pursuit of transcontinental integrations introduces complexities including regulatory compliance diversity, operational assimilation costs, and potential cultural frictions that may impair near-term profitability if not carefully managed. The lack of granular risk detail diminishes transparency but urges prudence regarding execution uncertainty.

Valuation Considerations Amidst Technical Crosses

At a recent price point of $164.45 per share, HLI trades amid stock price behaviors reflective of technical re-pricing despite solid quarterly fundamentals [F1][N8][N9]. The fall below critical moving averages highlights nervousness among short-term investors potentially influenced by macro discourse or sector rotation strategies.

While earnings strength supports underlying intrinsic value arguments fundamental analysis alone cannot fully explain this dichotomy without factoring in trader psychology and broader market flows affecting financial services equities currently.

Strategic Outlook: Positioning for Sustainable Growth

Bringing these elements together paints a picture of Houlihan Lokey at an inflection point characterized by robust core profitability leveraged through geographic expansion juxtaposed against episodic investor caution evidenced in technical trends. Its substantial liquidity reserves provide maneuverability to capitalize on arising strategic opportunities or cushion external shocks.

Continuing focus on maintaining specialized advisory excellence alongside executing integration plans will be critical to sustaining momentum built during recent quarters. Vigilance toward evolving risk dynamics remains essential given inherent cyclicality in deal activity especially amid international ventures.

Overall, Houlihan Lokey’s trajectory suggests careful balancing between seizing growth avenues while navigating nuanced market signals—a dynamic common across mid-sized investment banks expanding globally today.

This analysis is based solely on publicly available data as of early February 2026. It does not constitute investment advice but aims to provide an informed overview combining quantitative metrics with qualitative considerations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments