Horizon Space’s SPAC Model Hinges on SL Bio Merger Amid Liquidity and Timing Pressures

Horizon Space Acquisition II Corp. faces critical deadlines and tight liquidity as it seeks to complete its merger with SL Bio Ltd., a pivotal step in its SPAC business model.

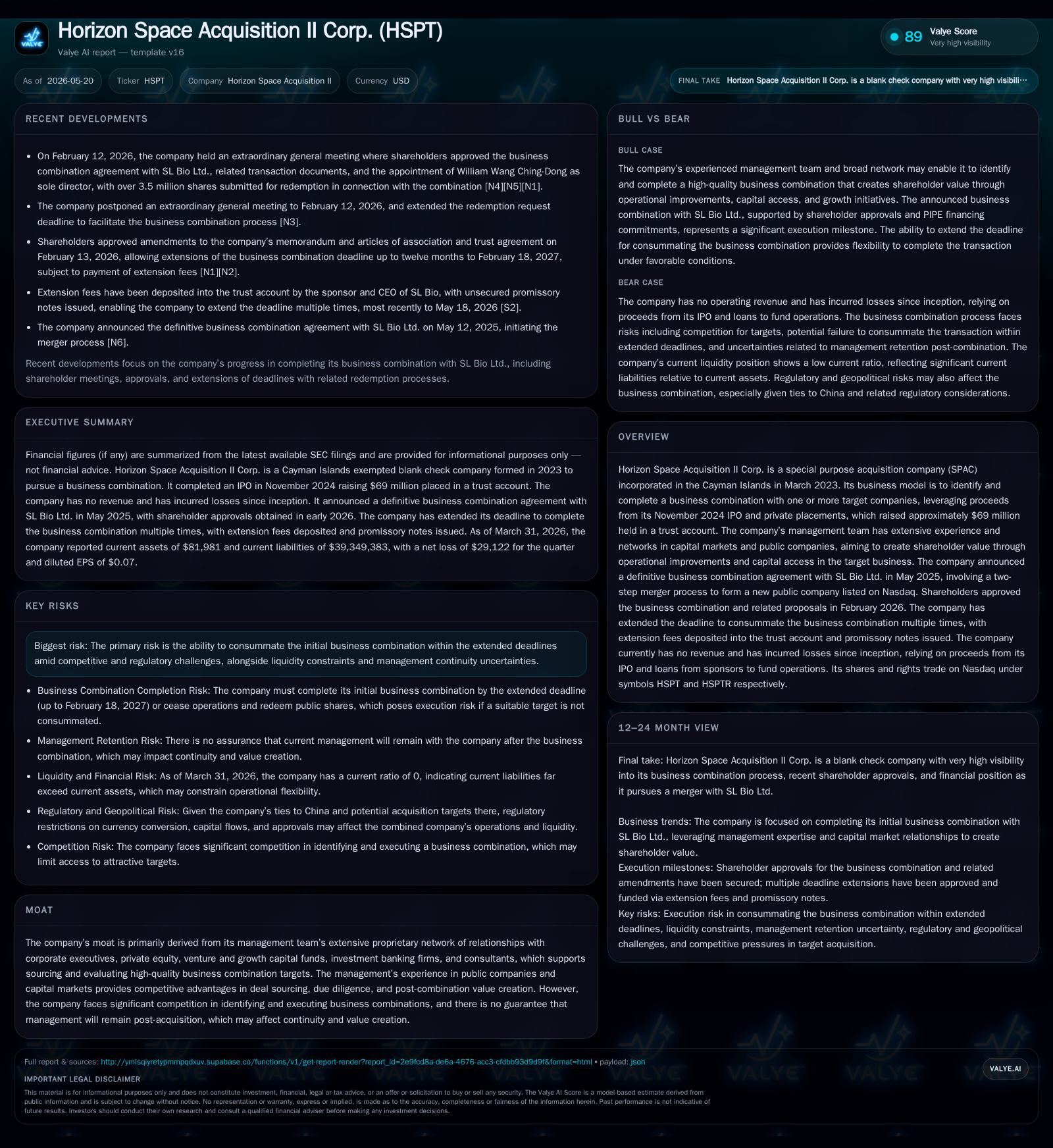

The latest quarterly filing of Horizon Space Acquisition II Corp. reveals ongoing deadline extensions and the issuance of unsecured promissory notes reflecting near-term liquidity pressures. The company aims to consummate a two-step merger with SL Bio Ltd. that would transition it into an operating public entity listed on Nasdaq. Horizon Space relies heavily on its management team's network and capital markets experience to source and close this transformative deal. However, challenges persist around timing, financing, regulatory approvals, and post-merger management continuity that will critically shape value creation prospects.

Latest Operating Developments: Deadline Extensions and Financing Moves

Horizon Space Acquisition II Corp.'s Q1 2026 filing dated May 20 reveals that the company continues to extend the period permitted to consummate its initial business combination with SL Bio Ltd. The company's charter allows up to twelve monthly deadline extensions beyond the original February 18, 2026 expiry; the recent 8-K filed April 21 shows this is now the third such extension [S2][S3]. To facilitate these deadline extensions—each requiring a $50,000 deposit into the trust account—Horizon issued unsecured promissory notes totaling $140,000 covering payments made in November 2025 ($690K), February 2026 ($50K), March 2026 ($50K), and April 2026 ($50K) [S3][S10]. These notes bear no interest and are payable either upon closing the business combination or at company term expiry.

This pattern underscores heightened urgency in managing working capital while navigating protracted deal closure timelines. The latest balance sheet as of March 31 shows extreme liquidity pressure: current assets stand at $81,981 against current liabilities of $39.3 million—a current ratio effectively zero reflecting reliance on trust account cash and sponsor support to meet near-term obligations [F1][S2]. The unsecured nature of the promissory notes calls attention to heightened execution risk during constrained financial flexibility.

SPAC Business Model: Mechanics and Value Creation Drivers

Horizon Space Acquisition II is a Cayman Islands-exempted blank check company incorporated in March 2023 specifically for leveraging capital raised from an IPO and private placements (gross proceeds approximating $69 million) held in trust pending completion of a qualifying business combination [S1]. Its fundamental value proposition centers on identifying one or more high-potential target businesses irrespective of geographic or industry boundaries but with particular affinity toward China-related opportunities due to management's network ties.

Units sold in its November 2024 IPO bundle ordinary shares alongside rights exercisable for fractional shares post-combination [S1]. Management holds broad discretion over trust account proceeds application, primarily directed at consummating a business combination or fueling working capital needs

The defining value driver lies in management’s capital markets expertise and expansive proprietary relationships spanning corporate executives, private equity groups, venture funds, investment banks, and consultants. This ecosystem supports sourcing differentiated targets capable of offering operational scalability combined with opportunity for revenue growth or profit margin expansion post-combination [S1]

However, inherent risks accompany this model due to intense competition for quality deals among peers in an active SPAC market with many sponsors vying for limited attractive targets. Additionally, post-merger value hinges critically on management continuity and successful integration execution.

Competitive Landscape: Positioning Within the SPAC Ecosystem

In the prolific second-wave SPAC environment circa mid-2020s, Horizon Space faces fierce rivalry from numerous blank check vehicles similarly positioned to capitalize on underserved or innovating sectors through publicly-listed merger targets [S1]. The ability to differentiate relies heavily on management teams’ networks for exclusive transactional access alongside demonstrated skills steering public companies.

Sponsors like Horizon emphasize targeting entities nearing inflection points—companies needing new capital infusion or experienced operational leadership capable of driving accelerated growth or margin optimization [S1]. Furthermore, evolving regulatory scrutiny and investor caution increasingly raise barriers for closing transactions efficiently. Ensuring alignment with PIPE investors who provide supplementary funding alongside public shareholders remains another competitive dimension shaping deal viability.

Target Company Focus: Strategic Rationale Behind SL Bio Transaction

The definitive agreement announced May 9, 2025 sets forth a two-tiered merger involving Horizon Space first merging into a newly created Cayman-based parent (PubCo), followed by SL Bio merging into another PubCo subsidiary—resulting in SL Bio operating as a Nasdaq-listed entity under PubCo’s umbrella [S13][S14]. This structure not only facilitates regulatory compliance with Nasdaq listing standards but also merges ownership while aligning incentives across former Horizon and SL Bio shareholders.

SL Bio’s selection fits Horizon’s strategic criteria targeting companies close to transformative events requiring additional operational expertise or capital deployment. The transaction anticipates capturing growth through organic expansion initiatives supported by prospective follow-on acquisitions and enhanced profitability from streamlined cost structures [S11].

The PIPE component supplements capital structure enhancement needed to sustain growth post-merger while supporting sufficient cash runway for scaling operations [S14]. These factors collectively make the SL Bio deal pivotal beyond a mere closing event—it represents Horizon’s evolution from shell into operating public entity.

Liquidity and Capital Structure Challenges Ahead of Combination Close

Financial disclosures highlight pressing liquidity constraints. Current assets barely cover routine payables; substantial liabilities create an imminent need for trust account funds release triggered only upon successful deal consummation or liquidation instructions if unconsummated by final deadlines [F1][S2]. This dynamic elevates default risk should timing slip further despite prior sponsor-funded note issuances covering incremental extension fees totaling almost $840K since late 2025 [S3][S10].

Absent material new financing sources besides existing PIPE commitments embedded within the transaction framework [S14], Horizon must navigate near-term working capital demands conservatively while finalizing complex legal and shareholder approval processes necessary before Nasdaq listing can occur.

Sponsor support evidenced via these unsecured notes—but absence of interest payments—signals tight financial maneuvering around capital allocation priorities given an absence of operating cash flows typical for SPACs pre-business combination closure [S2][F1]. The slender liquidity buffer necessitates rigorous monitoring as failure to meet milestones risks forced liquidation sequences unfavorable for all stakeholders.

Growth Opportunities Post-Merger: Scalability and Synergies

Upon completion, PubCo is expected to leverage public market access to accelerate SL Bio’s organic growth trajectory through targeted product innovation investments complemented by potential bolt-on acquisitions leveraging retained cash flow improvements post-integration [S11]. Enhanced transparency typical among Nasdaq-listed firms should unlock additional institutional investor interest possibly facilitating more favorable cost of capital conditions.

Operationally, synergies are envisioned via streamlined overhead rationalization while expanded marketing reach catalyzes market share gains especially within fast-evolving technology or biotechnology sub-sectors associated with SL Bio’s profile [S11]. Nonetheless growth success predicates on executing integration plans effectively alongside retention of key management personnel including CEO William Wang Ching-Dong appointed sole director following first merger phase approval early 2026 [S14].

Risks and Watchpoints: Deal Execution, Regulatory Hurdles, and Management Continuity

Central risks remain tightly coupled with completing the business combination within permitted timeframes despite multiple deadline extensions approved by shareholders thus far [S3][S14][S21]. Delays raise uncertainty regarding final closing amid potential exacerbation from competitor bids or adverse regulatory developments affecting SPAC mergers generally.

Nasdaq listing approvals depend not only on financial metrics but also governance structures—key milestones include appointed board composition post-merger which has been addressed via sole director approval but could face scrutiny upon detailed exchange review [S14]

Furthermore, shareholder redemption rates could materially shrink available merger consideration funds directly influencing pro forma capitalization adequacy post-closing [S12][S15]. Additionally absent guaranteed sponsor continuity post-merger may introduce execution risk particularly if management turnover disrupts strategic momentum devised during diligence phase.

What to Monitor Next: Milestones and Market Signals Ahead

Critical near-term indicators involve adherence to extended closing dates potentially approaching April-May-June windows following successive monthly extensions since original February expiration with periodic investor communications clarifying track progress [S2][S3][S10].

Watch for announcements regarding final shareholder vote outcomes if required amendments arise plus PIPE financing closings confirming committed funding availability as stipulated in subscription agreements already executed during proxy solicitation phases earlier this year [S14].

Regulatory comment letters or SEC feedback regarding registration statements (Form F-4) related filings may foretell timeline shifts or disclosure enhancements necessary before effective listing occurs [S13][S26]. Also monitor any further sponsor funding arrangements or additional promissory note issuances indicative of tightening cash reserves [S3] that may foreshadow increased execution risk.

Overall progress towards transforming from a shell entity holding trust funds into an operationally active public company backed by SL Bio will be defining for Horizon’s future market credibility.

Financial Profile Brief Summary

As of March 31, 2026, Horizon reported $81,981 in current assets against $39.3 million in current liabilities resulting in negligible short-term liquidity cushion absent release of trust account funds tied directly to deal closure conditions [F1][S2]. No operating revenues exist at this stage consistent with blank check company status; net income last reported positive at modest scale mainly reflects accounting artifacts rather than core earnings given no operating subsidiaries yet consolidated [F1].

Sponsor support through unsecured promissory notes totaling several hundred thousand dollars since late 2025 partially offsets working capital demands though lack interest accrual suggests informal financing terms aimed solely at preserving going concern until transaction closing [S3][S10]. This financial posture underscores urgency attached to completing business combination imminently given material liabilities looming against limited liquid resources.

Financial position in context

Current assets of $81981 and current liabilities of $39mm imply a current ratio near 0x for 2026-03-31 [F1]

This analysis is prepared solely for informational purposes based on publicly filed documents dated through May 20, 2026. It does not constitute investment advice or research views regarding any securities. Investors should conduct independent due diligence before making any financial decisions related to Horizon Space Acquisition II Corp.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments