HealthStream Inc’s Strategic Growth and Innovation Drive in Healthcare Workforce Solutions

HealthStream leverages its integrated hStream platform and targeted acquisitions to sustain growth, despite margin pressure and healthcare sector uncertainties.

HealthStream Inc has built a specialized SaaS offering around its proprietary hStream technology platform, providing integrated workforce development solutions tailored to healthcare organizations. The company reported revenue growth of 9.6% in 2025, while operating income and net income declined modestly. Strategic acquisitions like MissionCare Collective broaden network and clinical staffing capabilities, reinforcing its competitive position. Capital allocation included $30 million in share repurchases and $3.7 million in dividends supported by strong cash flow generation. Liquidity remains robust with $57 million in cash and equivalents plus a $50 million revolving credit facility maturing in late 2026. Growth prospects focus on AI integration and regulatory-driven demand amid macroeconomic risks.

Sustained Revenue Growth Amid Margin Pressures

HealthStream has demonstrated consistent revenue growth over recent years, with total revenue increasing from approximately $170.7 million in 2014 to an estimated $272 million in 2025 based on a reported 9.6% increase over the prior year [F1]. This reflects continued adoption of their subscription-based SaaS workforce development solutions tailored for healthcare organizations.

Despite top-line growth, operating income declined by 4.9% from $21.3 million in 2024 to $20.2 million in 2025 [F1]. Net income similarly decreased by 8.3% to $18.3 million during this period, indicating margin compression possibly due to higher personnel costs, cloud hosting fees, third-party software expenses, or amortization related to acquisitions [F1][N1][N3].

Operating cash flow increased by nearly 10% to $63.3 million in 2025 supporting capital expenditures that more than doubled to $3.7 million as the company intensified investments in software development and technology infrastructure [F1]. This reflects a strategic reinvestment phase focused on product enhancement.

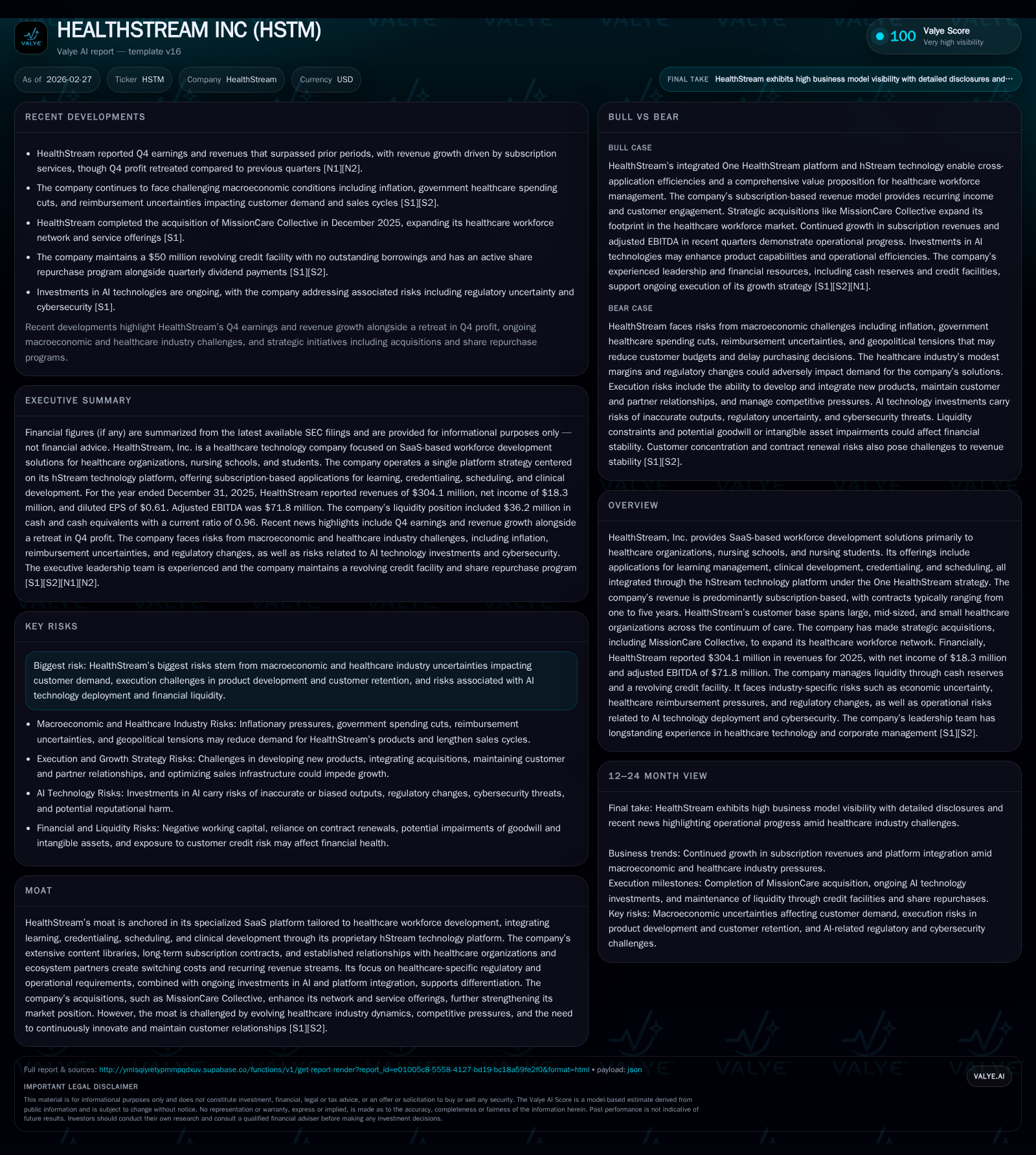

Table: HealthStream Annual Financial Performance (Selected Metrics)

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 18 | 63 | 20 | 4 | -8.3% |

| 2024 | 20 | 58 | 21 | 1 | +31.5% |

| 2023 | 15 | 64 | 16 | 2 | +25.8% |

| 2022 | 12 | 51 | 12 | 2 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Div ($mm) | Buybacks ($mm) | FCF ($mm) |

|---|---|---|---|

| 2025 | 4 | 30 | 60 |

| 2024 | 3 | 0 | 56 |

| 2023 | 9 | 62 | |

| 2022 | 23 | 49 |

Source: SEC companyfacts cache [F1].

Revenue figures for years other than FY2017 and FY2025 are not explicitly provided [F1].

One HealthStream Platform Underpinning Competitive Advantage

At the core of HealthStream’s strategy is the One HealthStream approach which consolidates all services onto the proprietary hStream technology platform [S1][S2]. This platform integrates learning management systems (LMS), credentialing workflows, scheduling logistics, and clinical development tools tailored specifically for healthcare workforce complexities.

By offering a unified SaaS framework aligned with regulatory requirements such as HIPAA compliance and healthcare-specific credentialing standards, the company creates significant switching costs for customers reliant on integrated workflows.

Multi-year subscription contracts generate recurring revenue streams supported by extensive content libraries developed for nursing schools, hospitals, and outpatient providers.

The platform also incorporates features like privileging verification automation and dynamic scheduling algorithms optimized for clinical labor variables enhancing operational efficiency.

Strategic Acquisitions Expand Market Reach

HealthStream has extended its solution set through acquisitions including MissionCare Collective which broadens its clinical staffing network capabilities beyond digital learning offerings [S1].

This acquisition aligns credentialing with physical staffing placement needs faced by healthcare delivery systems expanding cross-selling opportunities across service lines.

Integration efforts require focus on cultural alignment and system interoperability as noted among disclosed risk factors [S20].

Financial Performance Insights: Cash Flow Strength Amid Profitability Challenges

Despite declines in operating income and net income due to increased costs including stock-based compensation and amortization expenses related to acquisitions, operating cash flow improved significantly reaching over $63 million in FY2025 [F1][N1][N3].

Days Sales Outstanding (DSO) improved from approximately 40 days in prior years to around 37 days supporting better cash collections.

Capital expenditures increased sharply reflecting intensified investments primarily aimed at software development to maintain competitive positioning.

Return on equity remained moderate at about 5.2%, reflecting a substantial equity base accumulated through retained earnings and goodwill from acquisitions [F1].

Growth Outlook Supported by AI Integration and Regulatory Demand

HealthStream is advancing AI-driven analytics within its hStream platform targeting enhanced credentialing accuracy, predictive workforce demand modeling, and personalized learning pathways [S20].

Simultaneously ongoing regulatory mandates enforcing workforce credentialing compliance provide steady baseline demand for subscription services.

Demographic trends emphasizing nursing workforce replenishment alongside digital transformation initiatives across healthcare settings further support medium- to long-term growth fundamentals.

Risks from Macroeconomic Environment and Healthcare Sector Dynamics

Risks include inflationary pressures increasing labor costs for clients potentially affecting discretionary spending on elective offerings such as health equity content modules [S20].

Government reimbursement reductions especially impacting Medicaid could constrain budgets limiting solution uptake.

Labor shortages induce uncertain employment patterns influencing user volumes tied to subscriptions.

Budget cuts or insolvencies among healthcare providers may negatively impact contract renewals or pricing power contributing to revenue volatility.

Capital Allocation Emphasizes Share Repurchases and Dividends

In calendar year 2025, HealthStream completed share repurchases totaling approximately $30 million under multiple authorization programs at average prices around the mid-$20s range per share reflecting management confidence without compromising liquidity [F1][S4][S6][S13].

Quarterly dividends paid totaled about $3.7 million aligned with a dividend policy adopted since early-2023 demonstrating consistent shareholder returns.

Free cash flow after capex approximates $59.6 million supporting disciplined capital deployment amidst ongoing investments.

Strong Liquidity Position Maintained

At December 31, 2025, HealthStream held approximately $36 million in cash and equivalents supplemented by marketable securities contributing additional liquidity toward meeting working capital needs [F1][S10].

A revolving credit facility of up to $50 million maturing October 6, 2026 remains undrawn with full covenant compliance ensuring financial flexibility [S7][S8][S15].

Investor Considerations: Execution Risks and Monitoring Points

Full-year guidance for fiscal year ending December 31, 2026 has not been disclosed prompting focus on quarterly earnings results for signs of margin stabilization amidst heavy investment phases [N3].

Execution risks include timely AI integration aligned with customer expectations alongside managing contract renewal rates sensitive to economic conditions.

Ongoing efforts toward seamless user experience enhancements across platform modules will be critical to maintaining competitive advantage against emerging specialized healthcare SaaS providers.

Investors should track updates on new contract wins, renewal retention metrics at current pricing levels, outcomes related to contingent consideration from acquisitions, and potential impacts of inflation-related contract adjustments commencing mid-2024 onward [N3][S12][S24].

This analysis is based on audited financial data and company disclosures up through early-2026 without constituting investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments