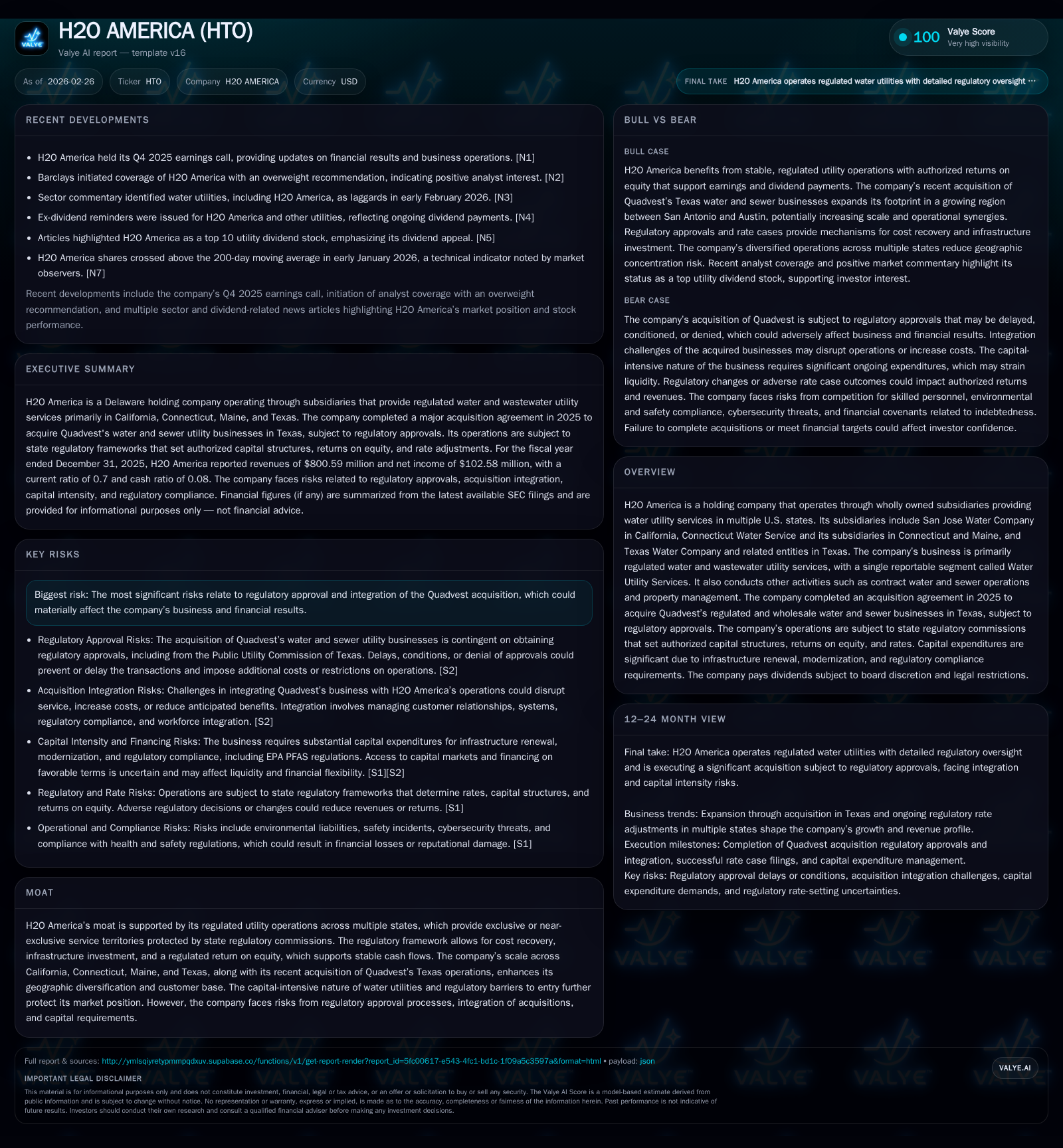

H2O America Posts Resilient Growth as Texas Expansion Looms

H2O America demonstrates steady financial and operational momentum driven by regulated utility services while preparing to integrate a major Texas acquisition.

H2O America’s regulated water utility business has steadily increased revenue, operating income, and cash flows from 2022 through 2025, reflecting operational scale across California, Connecticut, Maine, and Texas. The company's upcoming Quadvest acquisition in Texas represents a significant expansion but comes with regulatory approval risks that may delay or limit anticipated benefits. Financially, H2O America manages increasing leverage amid capital-intensive operations, balancing growth with regulatory constraints on rates and returns. Dividend policy remains supported by strong operating cash flow despite legal and environmental contingencies affecting subsidiaries.

Historical Revenue and Earnings Expansion Fueled by Operational Scale

H2O America has showcased steady financial progress over the last four full fiscal years leading up to December 31, 2025. The company’s consolidated revenue climbed from $620.7 million in FY2022 to $800.6 million in FY2025, marking a compounded annual increase of nearly 7%[F1]. Operating income followed a similar positive trajectory expanding from $131.0 million in FY2022 to $177.5 million in FY2025, although margin pressures relative to revenue growth moderated this figure with a CAGR near 4.1% within the period[F1]. Net income similarly advanced at an approximate CAGR of just above 7%, reaching $102.6 million in FY2025[F1].

A particularly notable aspect of this growth story is operating cash flow (CFO), which surged 25.2% year-over-year in the latest fiscal period to $244.8 million[F1]. This substantial boost in CFO highlights the company's ability to convert regulated revenues into liquid resources supporting capital expenditures and shareholder distributions despite the capital-intensive nature of water utilities.

The table below encapsulates these key financial metrics along with their respective year-over-year changes, painting a clear picture of H2O America's upward performance trend.

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 801 | 103 | 245 | 178 | +7.0% | +9.2% |

| 2024 | 748 | 94 | 196 | 171 | +11.6% | +10.6% |

| 2023 | 670 | 85 | 191 | 149 | +8.0% | +15.1% |

| 2022 | 621 | 74 | 166 | 131 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | ROE% |

|---|---|

| 2025 | 6.7 |

| 2024 | 6.9 |

| 2023 | 6.9 |

| 2022 | 6.6 |

Source: SEC companyfacts cache [F1].

Operating cash flow growth notably outpaced net income growth reflecting efficient management of working capital and non-cash expenses[F1].

Regulatory Environment’s Role in Sustaining H2O America’s Moat

H2O America’s core strength is rooted in its portfolio of regulated water utilities spread across California (San Jose Water Company), Connecticut and Maine (Connecticut Water Service subsidiaries), and Texas (Texas Water Company)[S1][S5]. Each operates within exclusive or near-exclusive service franchises governed by state public utility commissions that establish authorized rate bases and allow a permitted return on common equity (ROE). This regulatory framework safeguards revenues by enabling cost recovery for operating expenses and infrastructure investments, stabilizing future cash flows — critical elements forming the backbone of H2O America's economic moat[S14].

The authorized capital structures vary modestly by jurisdiction; for instance, California allows a debt/equity ratio around 45/55 percent while Connecticut approaches roughly a balanced structure near 47/53[S19] — demonstrating regulators' preference for conservative leverage aligned with utility risk profiles.

Within each state franchise territory, regulatory commissions impose rigorous oversight—including reviewing rate case submissions based on detailed cost forecasts and infrastructure needs—aimed at balancing utilities’ ability to fund operations against customer protection concerns[S14]. However, this process inherently subjects H2O America to timing risks since delays or rejections during rate cases may temporarily suppress revenues even as fixed costs persist[S14]. Geographic diversification into multiple states partially alleviates concentration risk faced when adverse regulatory outcomes occur but does not eliminate political or environmental exposure inherent to utilities[S5][S16].

Overall, these protected territories underpinned by cost-plus ratemaking reinforce steady top-line predictability despite cyclical or weather-driven demand fluctuations common in water consumption patterns[S5], evidencing the resilience associated with essential public utility services.

2025 Quadvest Acquisition: Growth Catalyst or Integration Challenge?

In mid-2025, H2O America announced the acquisition of Quadvest's regulated and wholesale water/sewer businesses in Texas under asset purchase agreements valuing part of the acquisition at approximately $480 million on approved fair market value grounds[S1][S19]. This transaction would expand H2O America’s footprint substantially within the high-growth corridor between San Antonio and Austin through Texas Water Company subsidiaries.

The Public Utility Commission of Texas (PUCT) must approve this transfer before closing can occur[S1][S2]. Although management expects approval around mid-2026[N1], regulatory processes could extend beyond estimated timelines or impose conditions that restrict operational flexibility or elevate compliance costs[S1][S2]. Such hurdles could diminish expected integration synergies or defer accretive earnings contributions.

Further complicating matters is the challenge typical of integrating acquired assets that may have differing systems, workforce cultures, or customer relationships—a potential material disruption amidst continued investment demands for aging infrastructure[S13]. Failure to consummate the deal timely also exposes H2O America to termination fees currently pegged at $21 million under specified circumstances[S23].

Hence, while Quadvest represents an important strategic growth vector given demographic trends supporting long-term demand increases in Texas[S16], it poses tangible execution risks both operationally and financially that warrant close scrutiny.

Capital Structure and Liquidity: Managing Debt Amid Expansion

Capital intensity defines H2O America’s operational model given ongoing replacement cycles for aging water infrastructure coupled with regulatory mandates reinforcing system modernization[S20]. The company funds expenditures predominantly via internally generated cash flows supplemented by debt issuances and occasional equity offerings where necessary[S4][S6].

However, recent acquisitions including Quadvest have increased overall indebtedness materially raising debt-to-equity ratios beyond historical levels[S4][S6]. While exact leverage ratios are not explicitly enumerated here, rising debt elevates interest coverage risks particularly amid tightening credit markets or if interest rates increase further[S9].[F1] reports current assets totaling approximately $190.6 million versus current liabilities about $273.4 million as of December end-2025 implying a current ratio close to only ~0.7 — signaling tight short-term liquidity conditions requiring active working capital management.

Liquidity remains dependent upon undrawn lines of credit alongside robust operating cash flow generation; nevertheless covenant restrictions embedded within debt agreements limit flexibility,[S26] potentially constraining rapid deployment of capital for further acquisitions or dividends if financial tests tighten.[S15]

The company has also implemented ring-fencing governance structures isolating Connecticut Water subsidiaries following prior acquisitions which place additional restrictions on internal capital movements between affiliates[S10][S27], limiting centralized control but supporting credit quality through segregation.

Navigating these complexities will remain pivotal as the firm balances growth ambitions against prudent financial stewardship amid rising external economic pressures.[S4]

Assessing Dividend Policy and Return on Equity in the Context of Growth

H2O America reported net income of $102.6 million against shareholder equity approximating $1.54 billion at fiscal year-end[F1], resulting in an indicative return on equity around 6.7% — reflective broadly of authorized ROEs allowed by regulators across its franchises.[F1]

Dividend payments have been highlighted as sustainable given strong operating cash flows exceeding net earnings significantly ($244.8 million CFO vs $102.6 million net income)[F1], underscoring careful alignment with regulated earnings stability rather than aggressive payout schemes.[N6]

Articles recognize H2O America among top utility dividend stocks due to consistent quarterly distributions backed by predictable tariff mechanisms[N6],[N5] although precise payout ratios are not disclosed publicly.

Dividends remain subject to board discretion considering legal requirements under Delaware corporate law plus contractual limitations stemming from debt covenants restricting distributions based on restricted net assets.[S15]

Thus far, historical dividend policies suggest conservatism prioritizing retention for necessary reinvestment amidst infrastructure aging challenges combined with selective shareholder returns suited for income-focused investor constituencies.

Key Risks Centered on Regulatory Approvals and Legal Proceedings

The foremost corporate risks cluster around successful completion of Quadvest takeover conditions, particularly PUCT approval which remains uncertain timing-wise with potentially significant delays or imposed restrictions reducing merger benefits[S1][S8].[N1]

Furthermore, subsidiary Connecticut Water Company faces pending class action litigation alleging contaminants in supplied water triggered by environmental class actions related to PFAS compounds.[S8][S11] These proceedings entail considerable monitoring efforts though partial legal settlements with major manufacturers (3M, DuPont) have generated compensatory proceeds exceeding $25 million allocated among affected utilities during FY2025 alone.[S11]

Pollution liability insurance coverage excludes some contamination classes posing further exposure risks while ongoing compliance demands elevate operational costs.[S12] Broader regulatory changes targeting environmental standards likewise could prompt higher capital outlays eroding margin leeway.[S14]

Finally employee safety incidents or systemic IT disruptions may cause reputational damage alongside direct financial costs.[S20][S24]

Collectively these factors cement an elevated focus on regulatory compliance risk management pivotal for sustaining stable earnings trajectories.[S22]

Near-Term Outlook: Monitoring Rate Cases and Regulatory Timelines

While explicit forward guidance remains limited,[N3] stakeholders should closely watch developments around PUCT’s final ruling concerning the Quadvest acquisition expected potentially mid-2026 but subject to extensions[N1].[N3] Speedy approval would unlock immediate strategic benefits including expanded customer base and rate base accretion; delays would deflate near-term earnings improvements.

Additionally pending or forthcoming rate case filings across California and Connecticut territories merit attention as they will inform future tariff pricing structures influencing revenue streams post-FY2025.[N3] Given seasonality effects typical for water consumption noted within third quarter dynamics,[S5] downstream quarterly disclosures might reveal incremental trends affecting operating margins.

Overall vigilance regarding evolving regulatory environments combined with integration execution milestones will be crucial signals guiding assessment of H2O America's medium-term growth prospects.

This analysis aggregates publicly filed financial data and official disclosures without extrapolation beyond presented facts or forward-looking statements absent explicit company guidance references thus avoiding speculative conclusions regarding future results. Investors should consider regulatory complexity inherent to water utilities when interpreting operational momentum relative to associated execution risks.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments