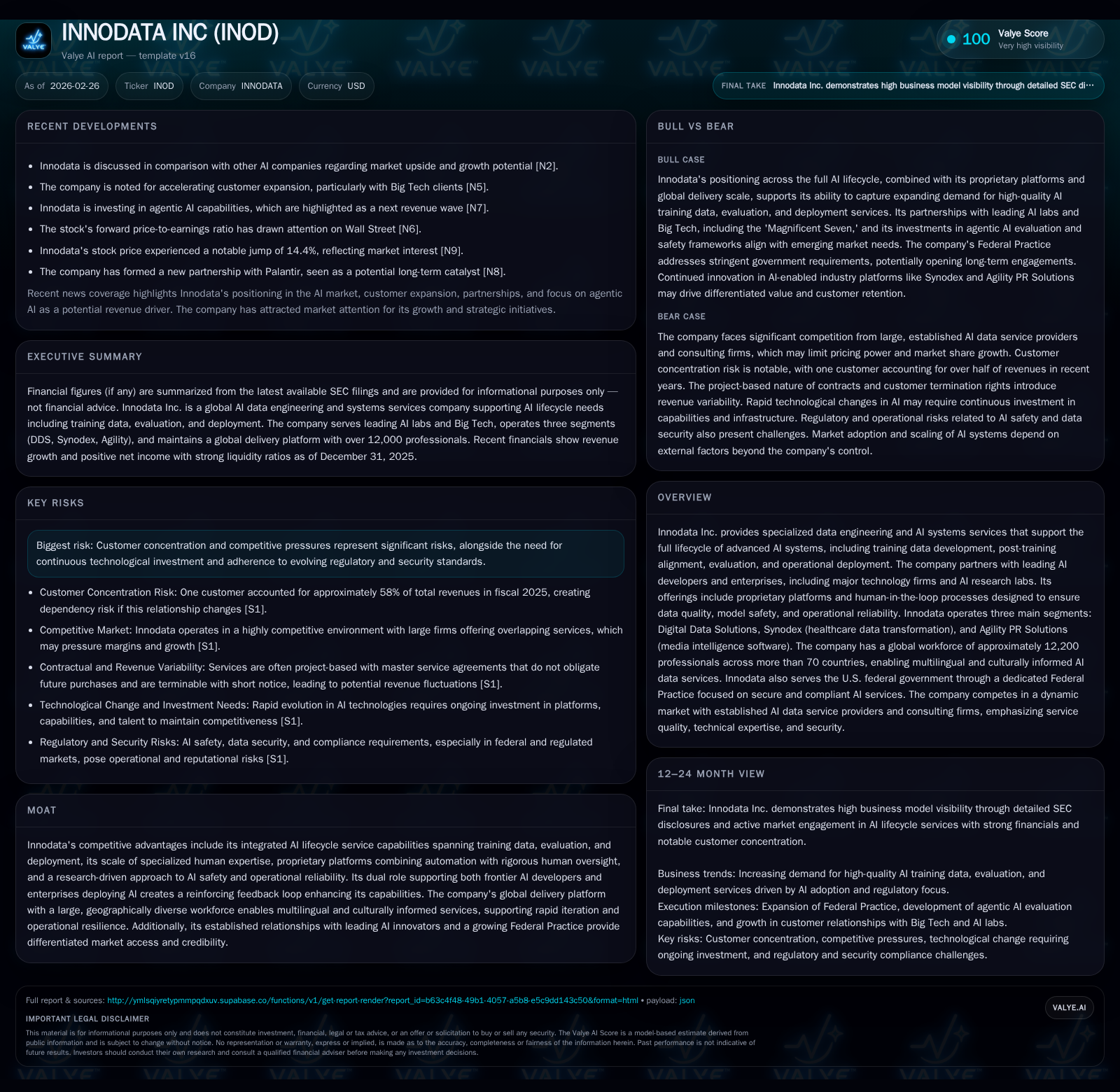

Innodata Fuels AI Lifecycle Growth amid Concentrated Customer Base and Innovation Push

AI data engineering leader Innodata leverages proprietary platforms and global expertise to capture expanding AI services demand while navigating customer concentration risks.

Innodata Inc. has demonstrated solid growth driven by its integrated AI lifecycle data services spanning training, alignment, evaluation, and deployment. Revenues reached $86.8 million in 2023 with operating income surging to nearly $39.9 million in 2025, reflecting strong operational leverage. Its competitive moat stems from proprietary platforms combined with a specialized global workforce serving major tech firms and federal clients. However, substantial revenue concentration on one customer—accounting for over half of total revenues—poses execution risk. Innodata’s ongoing innovation via its Labs and Technology Practices teams aims to sustain growth as AI adoption accelerates broadly across industries. Capital generation remains robust, supporting R&D investments and balance sheet strengthening.

Company Overview and Business Model

Innodata Inc. operates at the nexus of data engineering and artificial intelligence system development. Founded more than 35 years ago with roots in structured data for information retrieval systems, the company has evolved into a specialized services provider powering the full lifecycle of advanced AI systems [S1][S6]. Its offerings encompass training data development, post-training alignment and preference optimization, safety evaluation frameworks, and operationalization including integration for agentic AI technologies.

The company leverages proprietary platforms built to combine automation tools with rigorous human-in-the-loop oversight to ensure data quality and model reliability. These capabilities address increasing demands from leading frontier AI developers as well as enterprises adopting complex AI workflows across mission-critical applications.

Its three primary operating segments reported are Digital Data Solutions (DDS), focused on large-scale AI training data and evaluation; Synodex®, a healthcare-specific data transformation platform targeting insurance and medical workflows; and Agility PR Solutions™, a media intelligence software suite enhanced with AI-driven analytics [S15].

With approximately 12,200 professionals deployed across more than 70 countries, Innodata delivers multilingual and culturally informed services that support fast iteration cycles essential to modern AI development environments [S6]. This global delivery scale represents a competitive advantage against smaller or more localized service providers.

Historical Financial Performance

Innodata's financial trajectory over recent years reflects steady revenue growth alongside significant margin expansion due to operational leverage. Revenue increased from about $58.2 million in fiscal year (FY) 2020 to approximately $79 million in FY 2022 before reaching $86.8 million by FY 2023—a near 10% compound annual growth rate (CAGR) over that period based on available data [F1].

Operating income shifted decisively positive after years of losses earlier in the decade (e.g., negative $5 million range reported around FY 2016-17). By fiscal year-end 2025, operating income surged to roughly $39.9 million representing a substantial year-over-year improvement from about $24.3 million in FY 2024—a gain of nearly 64% YoY [F1].

Net income followed suit with an increase to about $32.2 million in FY 2025 compared to $28.7 million the prior year, implying strong bottom-line leverage amid consistent revenue gains [F1]. The company’s equity base expanded alongside retained earnings improving book value markedly.

A summary table capturing these data points is provided below:

Historical performance (annual)

| FY | Rev ($mm) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 32 | 47 | 40 | +12.3% | ||

| 2024 | 29 | 35 | 24 | +3256.4% | ||

| 2023 | 87 | -1 | 6 | +9.8% | +92.4% | |

| 2022 | 79 | -12 | -1 | +13.3% |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | FCF ($mm) | ROE% |

|---|---|---|

| 2025 | 36 | 30.0 |

| 2024 | 27 | 45.2 |

| 2023 | 0 | -3.5 |

| 2022 | -8 | -63.6 |

Source: SEC companyfacts cache [F1].

Note: CFO = Operating Cash Flow; Equity includes retained earnings plus other reserves [F1].

Growth Drivers and Future Prospects

The company’s future growth prospects are underpinned by the rapid expansion of AI adoption globally alongside persistent emphasis on trustworthy and safe AI deployment—domains where Innodata holds differentiated expertise [S16]. The market for high-quality training datasets, post-training alignment mechanisms, ongoing evaluation frameworks, and help enabling agentic or autonomous systems is expanding swiftly amid intensifying enterprise digitization.

Innodata's strategic positioning supporting both frontier AI developers (including five of the 'Magnificent Seven' technology leaders) and enterprises deploying these models creates reinforcing dynamics enhancing capability development and cross-selling opportunities [S6][S15]. Synergies emerging from co-development of standards around evaluation metrics and safety bolster its moat versus competitors focused narrowly on either model creators or end-user organizations.

Continued investment through Innodata Labs facilitates pioneering research into next-generation agentic capabilities, trust & safety detection techniques, post-training refinements, and regulatory compliance support—all critical as regulators worldwide increase oversight of powerful AI systems [S14][N1].

Expansion in adjacent domains such as healthcare digital transformation via Synodex® offers additional avenues for diversified growth leveraging existing technical foundations and customer relationships [S15]. Likewise, enhancements driven by AI integration bolster Agility PR Solutions’ market position amid growing appetite for media intelligence powered by machine learning.

However, potential constraints include the high revenue concentration risk posed by one DDS segment client contributing about 58% of fiscal year revenue in 2025 (up from approximately 48% in the prior year), exposing the firm to variability linked to contract renewals or shifting priorities by this key account [S4][S9]. Moreover, contract structures often entail master service agreements with project-based statements subject to termination within short notice windows (30–90 days), necessitating continuous successful new business development efforts.

Competitive pressures remain elevated given several sizable alternatives ranging from pure-play specialist firms like Appen or Scale AI to broader business process outsourcers such as Accenture or Cognizant which bundle overlapping services amidst fast-evolving technology trends [S28]. Innodata counters this through holistic lifecycle integration capabilities coupled with internal research rigor.

Forecasts Milestones & What To Watch

While explicit forward guidance was not provided in filings or recent press releases [N2][N3], investors should monitor:

- Renewal rates and volume trends with top DDS client(s), given outsized revenue impact;

- Expansion progress within Synodex healthcare platform adoption;

- Innovation breakthroughs or commercialization outcomes emerging from Innodata Labs initiatives;

- Margins sustainability as scale improves across segments;

- Customer diversification measures potentially mitigating concentration risks;

- Partnerships such as those announced with Palantir that may facilitate longer-term enterprise deployments beyond data preparation phases [N6].

Quarterly earnings updates will serve as primary barometers for execution against strategic objectives.

Capital Allocation & Returns Analysis

Innodata maintains a robust balance sheet featuring significant liquidity; cash & equivalents stood around $82 million at fiscal year-end 2025 while total equity totaled $107 million—more than quadruple compared to three years prior indicating retained earnings accumulation alongside capital raises or stock issuances supporting expansion initiatives [F1].

Operating cash flow generation grew impressively surpassing $46 million most recently versus just $5.9 million two years prior illustrating improved profitability translating into cash conversion efficiencies.

Capital expenditures elevated moderately reflecting investments into platform development infrastructure amounting roughly $11 million in FY25 versus prior levels near $5-7 million range historically [F1][S14]. The resulting free cash flow approximated $35.6 million—the surplus enabling agility for potential strategic acquisitions or partnerships without leverage increase pressure.

No significant share repurchases were recorded recently according to available data; thus capital prioritization currently appears tilted toward organic growth funding rather than direct shareholder returns via dividends or buybacks which aligns with typical tech-sector reinvestment norms [F1].

Return on equity around an estimated 30% evidences effective capital utilization although this figure can fluctuate with client concentration shifts affecting profitability periods [F1].

Innodata’s revolving credit facility imposes covenants including fixed charge coverage ratios which management appears compliant with but represent considerations should borrowing needs rise amid future M&A pursuits or working capital demands [S18][S22]. Variable interest expense exposures linked to SOFR dynamics remain potential cost volatility factors.

Competitive Positioning & Risks

The company competes primarily through quality service delivery infused with domain expertise spanning multiple stages of AI lifecycle development—a contrast versus competitors offering one-off capabilities or broader but less specialized IT outsourcing packages [S8]. Proprietary technology assets coupled with a large multinational workforce underpin scalability advantages required by frontier model developers undertaking massive computational experiments needing curated training data sets.

Key challenges revolve around client concentration highlighted above plus competitive pressures intensified by entrants offering leaner cost structures or alternative crowdsourcing solutions disrupting traditional human-in-the-loop models.

Legal proceedings noted include securities class action litigation related to alleged misrepresentations around AI technology disclosures —while unresolved this remains an uncertain downside factor potentially impacting reputation or costs depending on outcome [S22]. Continued vigilance regarding regulatory developments impacting data usage permissions along with cybersecurity safeguards remains crucial given operational nature relying on sensitive datasets managed globally.

Summary Thoughts

Innodata Inc.’s transformation into a critical enabler within the generative AI ecosystem has translated into accelerating revenue growth paired with margin expansion over recent years supported by proprietary platforms and a vast skilled workforce operating worldwide. The firm’s ability to serve a dual client base comprising leading-edge model developers alongside enterprises adopting these technologies imbues it with structural advantages few competitors replicate precisely. Despite notable customer concentration risks requiring continuous diversification efforts, current fundamentals exhibit healthy cash flow generation facilitating sustained innovation investments while preserving financial flexibility. Future monitoring will focus keenly on contract execution robustness within key accounts alongside milestones emerging from Innodata Labs research channeling into commercial offerings aimed at harnessing next-wave agentic AI capabilities safely at scale.

This analysis is informational only and does not constitute investment advice or a recommendation regarding any securities or companies mentioned herein.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments