Tri Pointe Homes Faces Margin Compression and Profitability Challenges with Strategic Geographic Expansion

Strong land holdings and a diversified product portfolio underpin Tri Pointe’s operations as it contends with slowing revenue growth and margin pressures in 2025.

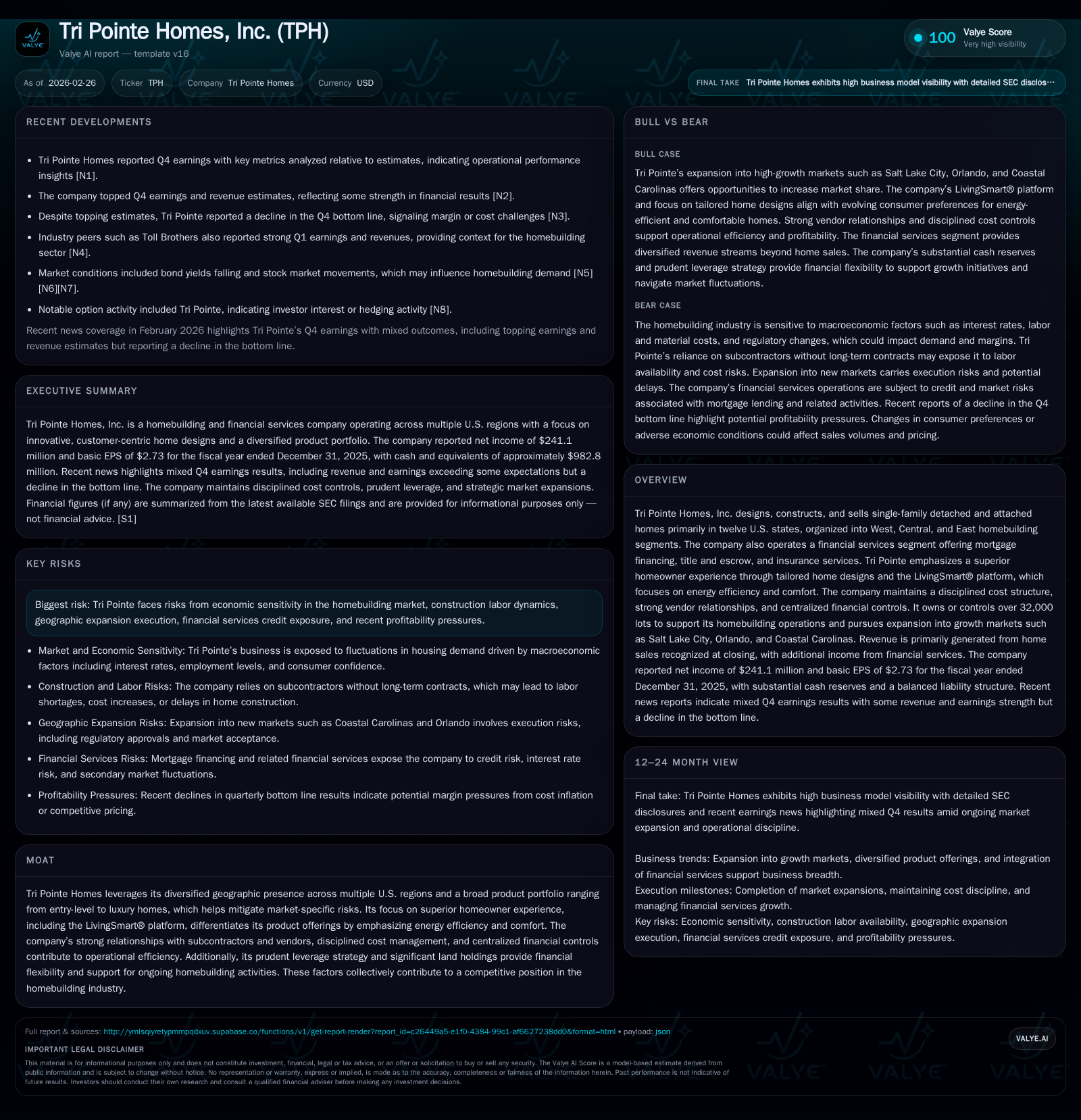

Tri Pointe Homes, Inc. reported a notable decline in profitability in 2025 despite generating solid operating income and maintaining substantial liquidity. The company’s revenue contracted by approximately 7% year-over-year, pressured by market headwinds and heightened economic sensitivity in its core homebuilding segments. With over 32,000 lots controlled and expansion into high-growth markets like Salt Lake City and Coastal Carolinas underway, Tri Pointe’s future growth hinges on successful geographic diversification and improved operational efficiency. While capital returns via share buybacks increased, the firm experienced significant erosion in net income and operating cash flow, highlighting mounting challenges in margin management amid cyclical market shifts.

Company Overview and Business Model

Tri Pointe Homes operates primarily as a residential homebuilder with three distinct geographic segments—West, Central, and East—including mature markets such as California and emerging expansion zones like the Salt Lake City region. The company complements its core home construction business with a financial services segment offering integrated mortgage financing, title escrow, and insurance products under "Tri Pointe Solutions." Through a diversified product range spanning entry-level to luxury homes and specialized active adult communities, Tri Pointe positions itself as a "progressive" builder emphasizing the LivingSmart® platform that enhances energy efficiency and homeowner comfort.

Historical Performance: Trends Through 2025

Over recent years leading up to 2025, Tri Pointe’s annual revenues stabilized around the $1.1 billion mark before contracting in 2025. Operating income peaked near mid-2020s levels but took a sharp downturn last year. Below is a summary of key financial metrics extracted from the latest consolidated statements [F1]:

Historical performance (annual)

| FY | Net ($mm) | CFO ($mm) | OpInc ($mm) | Capex ($mm) | Net YoY |

|---|---|---|---|---|---|

| 2025 | 241 | 161 | 302 | 33 | -47.4% |

| 2024 | 458 | 696 | 23 | +33.3% | |

| 2023 | 344 | 195 | 25 | -40.3% | |

| 2022 | 576 | 444 | 747 | 44 |

Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 277 | 129 | 7.3 |

| 2024 | 147 | 673 | 13.7 |

| 2023 | 175 | 170 | 11.4 |

| 2022 | 203 | 401 | 20.3 |

Source: SEC companyfacts cache [F1].

Revenue declined by approximately seven percent from prior full-year figures, driven largely by weakening demand dynamics in key markets amid broader economic uncertainty [S1][S3]. Operating income shrank disproportionately by nearly sixty percent reflecting margin compression due to elevated input costs like labor and materials coupled with potential cancellation rate upticks [S9]. These pressures cascaded into net income falling almost half year-over-year.

Operating cash flow exhibited significant contraction over the same period (-77%), indicating working capital stress or build-out timing differences relative to cash inflows from closings [F1]. Capital expenditures remained relatively low at $33 million but increased compared to prior years.

Geographic Diversification and Market Expansion

Tri Pointe maintains significant strategic land holdings exceeding 32,000 lots spread across twelve states [S19], underpinning future unit deliveries over multiple years. The company actively pursues growth in newer high-demand metro areas characterized by expanding populations and employment bases such as Salt Lake City (Utah), Orlando (Florida), and Coastal Carolinas [S19]. This expansion strategy offers diversification away from legacy markets which may face more pronounced cyclical limitations.

Execution risk exists related to entering these nascent regions including integration complexity and local regulatory landscapes [S9]. Nevertheless, seasoned local management teams provide operational know-how potentially smoothing entry hurdles.

Product Differentiation Through LivingSmart® Experience

Tri Pointe emphasizes creating a tailored homebuyer experience focused on quality design innovation and sustainability features within its LivingSmart® framework [S25]. This platform integrates energy-efficient building methods along with enhanced occupant comfort controls aiming to reduce utility bills long-term—attributes increasingly important in buyer decision-making today.

This focus on lifestyle-oriented home development serves as both a competitive edge against commoditized builds and an effort to navigate changing consumer preferences across generational cohorts.

Financial Services Segment Complementing Core Operations

The financial services arm provides mortgages, title insurance, escrow services, and property casualty insurance primarily targeting Tri Pointe buyers [S25]. By integrating these offerings internally under 'Tri Pointe Solutions,' the company captures additional margin streams beyond construction profits.

Credit risk related to mortgage financing is an ongoing concern due to macroeconomic shifts impacting real estate lending environments [S9]. Active portfolio management here will be crucial amid evolving interest rates or borrower credit profiles.

Capital Structure and Liquidity Profile

At December 31, 2025, Tri Pointe held cash and equivalents approaching $983 million—a robust liquidity cushion for operational needs or opportunistic investments [F1][S4]. The company maintains financing facilities including term loans, revolving credit lines, senior notes with staggered maturities providing diversified debt funding sources [S4][S7].

Share repurchases accelerated sharply in FY25 totaling $277 million versus $147 million in FY24—reflecting management’s preference for returning capital amid uncertain growth prospects [F1]. Dividend activity was not explicitly detailed but appears immaterial relative to repurchase activity.

Free cash flow—which approximates operating cash flow less capex—remained positive though significantly compressed at around $129 million last year [F1].

Profitability Returns and Efficiency Metrics

Approximate return on equity softened materially with last year’s net income of $241 million against equity of about $3.3 billion yielding ~7.3% ROE—a clear deceleration from prior periods characterized by double-digit returns [F1]. This reflects margin degradation pressures coupled with continued land investment diluting capital efficiency.

Operational discipline articulated through centralized financial controls aims to mitigate some cost inflation effects; yet industry-wide supply chain volatility continues presenting challenges [S9].

Outlook Considerations and Monitoring Factors (Analysis)

Absent explicit guidance within current filings or news releases [N1][N2][S3], critical indicators going forward will include:

- Volume trends in each geographic segment reflecting local housing demand health;

- Margin trajectory tied to input cost control including subcontractor labor availability;

- Financial services performance particularly mortgage credit loss trends under tightening underwriting standards;

- Cancellation rates which directly impact revenue recognition consistency;

- Success converting controlled lot inventory into deliveries amidst environmental or regulatory delays;

- Balance sheet management vis-à-vis debt maturities given sizable senior notes outstanding through late decade.

Macro variables such as interest rate fluctuations influencing mortgage affordability also bear watching given their substantial effect on purchasing power for prospective buyers.

Industry Context Note (Analysis)

Homebuilding historically exhibits pronounced cyclicality dictated by macroeconomic cycles impacting consumer confidence, interest rates, labor market tightness, material availability/pricing, as well as regulatory constraints on land supply. Companies like Tri Pointe benefit from geographic diversification—a mitigant—as local economies often cycle out of sync. However inflation spikes pose near-term operational headwinds for all builders.

Consumer preferences shifting toward sustainability add another layer requiring continuous product innovation backed by credible certifications which LivingSmart® seeks to fulfill.

Conclusion Summary

Tri Pointe Homes finds itself balancing entrenched operational strengths—including sizeable land assets and scalable regional presence—with profit margin challenges accentuated in FY25's results. Expansion initiatives targeting vibrant growth metros provide medium-term avenues but bring execution risks amid competitive, cost-sensitive environments. Financial prudence evident through liquidity reserves contrasts with bottom-line contractions underscoring the need for rigorous cost discipline going forward.

Investors should track quarterly updates elucidating recovery cadence of margins alongside sales volumes as the housing market navigates evolving macroeconomic headwinds.

This analysis is based solely on publicly available data up to February 26th, 2026 including SEC filings [F1][S#] and relevant news coverage [N#]. It does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments