Hexcel Corporation's Defensive Stance Amid Earnings Shifts in Advanced Composites

Hexcel balances a strong liquidity position with earnings volatility as it navigates evolving market conditions in specialized composites.

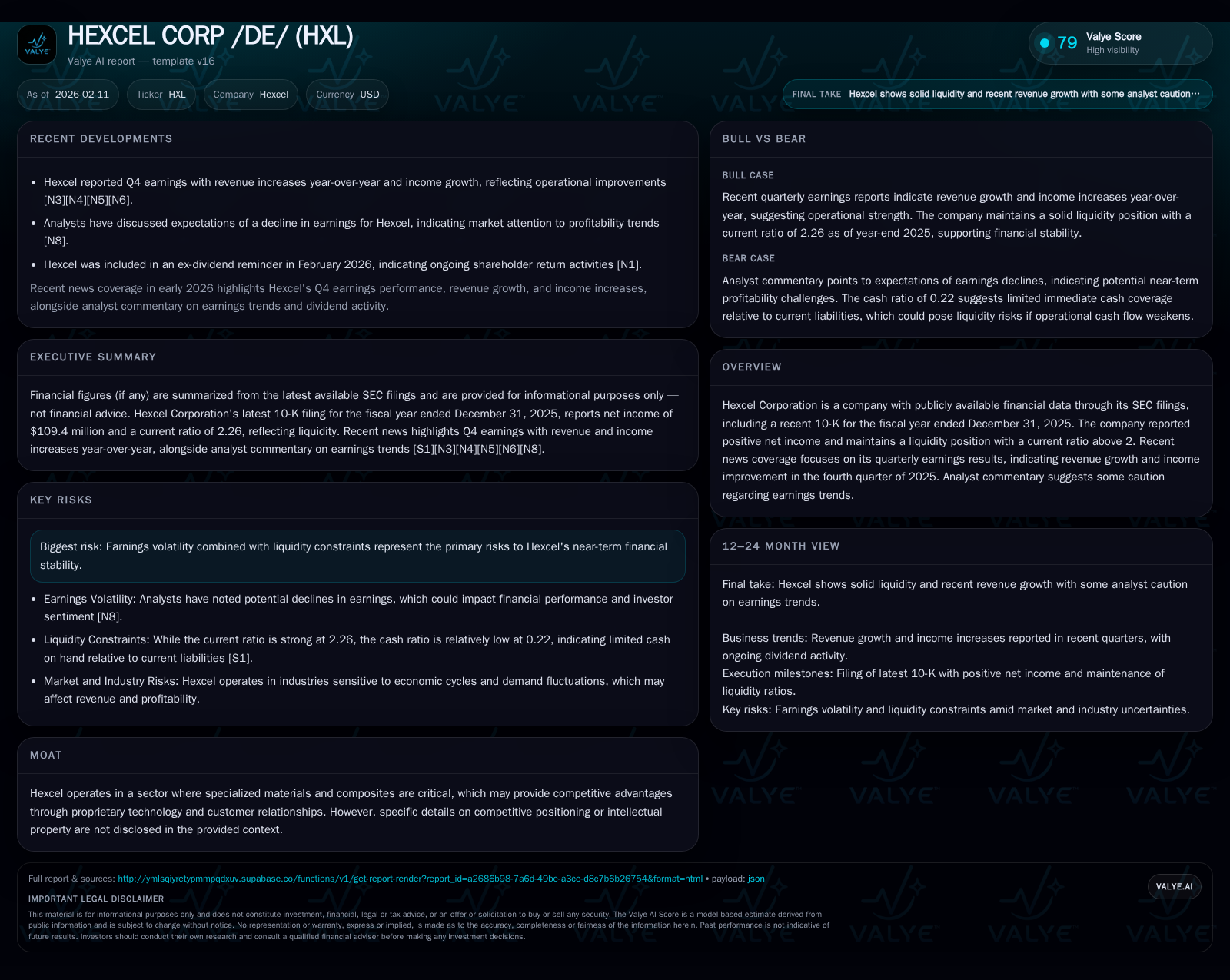

In the fourth quarter of 2025, Hexcel Corporation delivered better-than-expected revenue growth and net income gains, underscoring operational resilience. A robust current ratio above 2.2 further buttresses its financial footing, offering a buffer against cyclical industry pressures. Nonetheless, lingering concerns about earnings consistency and market skepticism temper enthusiasm, pointing to ongoing challenges in sustaining momentum amid sector volatility.

Crafting Competitive Edges: Hexcel’s Role in Advanced Composites

Hexcel Corporation occupies a vital niche within the advanced composite materials sector, primarily serving aerospace, defense, and industrial end markets where performance-critical applications dominate. The company’s reliance on sophisticated fiber-reinforced polymer composites and related technologies positions it as a key supplier in an industry where product differentiation often hinges on proprietary formulations and optimized manufacturing processes [S1]. Although explicit descriptions of Hexcel’s intellectual property portfolio remain sparse in public disclosures, the company’s repeated emphasis on its role supplying indispensable composite solutions suggests entrenched relationships with aerospace OEMs and Tier 1 suppliers that potentially constitute a defensible competitive edge [valye_report_excerpt]. These client ecosystems create high switching costs and facilitate sustained demand for Hexcel's materials amid industry barriers such as certification requirements and specialized engineering expertise.

Analyzing Q4 2025: Surpassing Expectations Against Cautious Forecasts

Hexcel’s fiscal Q4 2025 results revealed a notable stride forward, crossing revenue thresholds above street consensus and delivering net income gains that bucked recent cautionary signals from analysts [N3][N4]. Revenue growth year-over-year aligned with signs of recovery in aerospace production rates and increased industrial demand, underscoring the company’s ability to capitalize on improving market conditions [N2]. The reported net income of roughly $109.4 million for the full year reflects operational efficiency improvements coupled with favorable product mix effects [F1]. This encouraging financial momentum contrasts with earlier reservations about potential downturns in earnings caused by cyclical softness or supply chain disruptions [N6], illustrating Hexcel's capacity to exceed expectations despite an uncertain backdrop.

Financial Fortresses: Liquidity Metrics and Balance Sheet Health

A cornerstone of Hexcel’s recent strategic positioning lies in its robust liquidity profile, evidenced by a current ratio around 2.26 at year-end 2025 [F1]. With current assets surpassing $730 million against approximately $323 million of current liabilities, the balance sheet conveys ample short-term resource availability to sustain operations and absorb shocks without reliance on external financing [S1]. Cash and equivalents totaling approximately $71 million bolster this cushion further. Such liquidity strength enables Hexcel to weather industry cyclicality and invest selectively in innovation or capacity expansion without immediate solvency concerns. This defensive posture is significant given the inherent volatility typical of specialized materials sectors where capital expenditure timing and working capital management are critical.

Earnings Volatility: What Underpins Market Unease?

Despite positive headline results, the market remains wary of underlying earnings swings that have characterized Hexcel over recent periods. Analysts point to factors such as uneven aerospace production cycles influenced by airline order backlogs, geopolitical tensions affecting defense spending, raw material price fluctuations, and lingering supply chain bottlenecks as key contributors to periodic profitability fluctuations [N6][S1]. The company’s SEC Risk Factors explicitly cite volatile earnings patterns alongside liquidity constraints as primary risks that could materially impact future financial performance [S1][S2]. This dual challenge—managing cash flow stability while sustaining profit margins amid shifting demand—forms the core tension investors watch closely.

Competitive Moat or Market Mirage? Examining Hexcel’s Defensibility

While Hexcel promotes its status as a technological leader in advanced composites delivering critical materials for demanding applications, the absence of detailed public disclosures creates ambiguity around the sustainability of its competitive moat [valye_report_excerpt][S1]. The reality likely lies between visible proprietary product advantages—such as patented prepreg systems or automated manufacturing capabilities—and more intangible benefits deriving from established customer partnerships and regulatory certifications unique to aerospace constituents. However, without explicit articulation of intellectual property strength or distinctive cost advantages in filing narratives or investor messaging, questions linger whether Hexcel's defenses can fully insulate it from intensified competition or commoditization pressures over time.

Risk Radar: Insights from SEC Filings on Earnings and Liquidity

Reviewing Hexcel’s latest SEC submissions underscores persistent operational risks chiefly anchored around financial variability. The annual 10-K highlights that adverse shifts in aerospace production rates or raw material costs could drive substantial earnings volatility while constraining free cash flow generation [S1]. Complementary quarterly updates reinforce that no material change has occurred regarding risk exposures since prior disclosures, implying continuous vigilance required on liquidity fronts especially should market conditions deteriorate or capex demands rise unexpectedly [S2]. These embedded risk acknowledgments affirm the company’s awareness yet simultaneously flag caution for stakeholders analyzing stability beyond headline metrics.

Peer Landscape: Benchmarking Hexcel in the Specialized Materials Sector

Within its specialized materials segment, Hexcel's performance trajectory finds relevant comparison points against peers like Woodward Inc., which similarly experienced better-than-expected quarterly revenues recently amid growing end-market demand [N1][N5]. Such peers operate under comparable cyclical influences linked to aerospace aftermarket cycles and industrial capital goods trends. While broad sector momentum appears supportive currently, peer comparisons emphasize the challenge of differentiating through technology leadership versus scale efficiencies or diversified end-market exposures. This context situates Hexcel’s incremental gains within a contested arena where maintaining premium positioning requires continuing innovation paired with cost discipline.

Analyst Voices: Interpreting Recent Upgrades and Warnings

Analyst commentary adds nuance to market perspectives surrounding Hexcel. Morgan Stanley's recent upgrade signals confidence derived perhaps from Q4 beat momentum or valuation considerations even as other brokers caution about expected near-term earnings declines tied to anticipated softening demand or margin pressure dynamics [N6][N8]. This juxtaposition suggests divergent interpretations of how well Hexcel can manage cyclical headwinds or leverage its strategic initiatives going forward. It also underlines an underwriting tension between fundamental optimism steered by quantitative beats versus qualitative skepticism rooted in recurring uncertainties.

Dividend Signals and Capital Allocation

Recent ex-dividend notifications signal continued management commitment toward shareholder returns despite earnings fluctuations [N7]. Such dividend actions may be viewed as efforts to maintain investor confidence by demonstrating financial discipline and cash flow adequacy. However, they also suggest a balancing act wherein capital allocation decisions reflect cautious optimism tempered by need for prudent liquidity preservation amid less predictable earnings pathways.

Outlook Variables: Navigating Growth Amid Uncertainty

Looking ahead, Hexcel faces a landscape marked by both opportunity and challenge. Its structural advantages in indispensable composite technologies offer avenues for organic growth alongside potential expansion into emerging markets such as renewable energy composites or next-generation aerospace platforms. Meanwhile, persistent macroeconomic uncertainties—geopolitical shifts impacting defense budgets, inflationary pressures on input costs, supply chain normalization trajectories—will test operational agility. Maintaining strong liquidity provides strategic optionality but does not immunize the company from fundamental demand volatility highlighted repeatedly in SEC disclosures [ valye_report_excerpt][S1][N6]. How well Hexcel calibrates investment pace with evolving market realities will be crucial for sustaining growth momentum beyond episodic earnings beats.

This analysis is based exclusively on publicly available information including SEC filings and recent news reports; it does not constitute investment advice or recommendations.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments