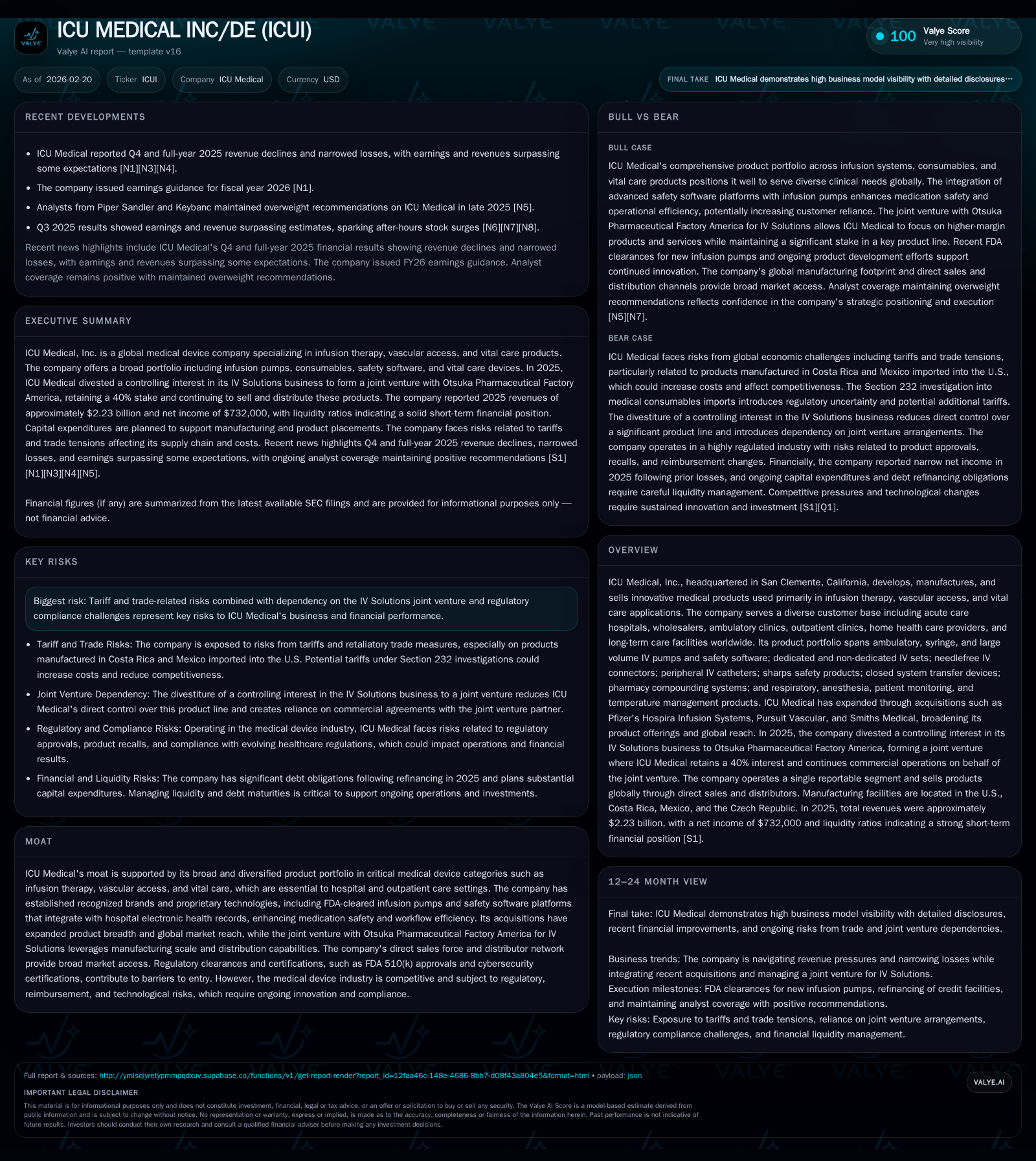

ICU Medical’s Tariff Impact and JV Transition Amid Modest Revenue Contraction in 2025

The company's revenue dipped in 2025 amid tariff headwinds and a strategic divestiture, while ongoing regulatory and capital dynamics shape near-term outlook.

ICU Medical experienced a 6.3% revenue decline in fiscal 2025, driven notably by increased tariffs on critical medical device imports and the transition of its IV Solutions business into a joint venture with Otsuka. Although operating income remained stable year-over-year, net income swung from loss to near-breakeven reflecting cost controls and prepayments on debt funded by divestiture proceeds. The company’s extensive product portfolio and recent acquisitions underpin its moat, but tariff uncertainty and FDA regulatory scrutiny pose ongoing operational risks. Capital expenditures are set to increase moderately in 2026, focusing on manufacturing facilities and product placement, while debt refinancing reduces near-term principal repayments.

Company Overview

ICU Medical Inc., based in San Clemente, California, designs and manufactures a broad portfolio of critical care medical devices spanning infusion therapy pumps (ambulatory, syringe, large volume), safety software integrations for hospital IT ecosystems, vascular access products including needlefree connectors and catheters, sharps safety items, closed system transfer devices for oncology compounding, and a variety of respiratory and anesthesia-related monitoring equipment. The company sells primarily into acute care hospitals but also serves ambulatory clinics, home health providers, wholesalers, and long-term care facilities worldwide. ICU Medical has bolstered its offerings through acquisitions such as Pfizer’s Hospira Infusion Systems (2017), Pursuit Vascular (2019), and Smiths Medical (2022), expanding technology breadth and geographic reach.

In late 2024 through early 2025, ICU Medical strategically divested a controlling interest in its IV Solutions business via the formation of a joint venture with Otsuka Pharmaceutical Factory America (Otsuka). This transaction transferred related assets into Otsuka ICU Medical LLC with ICU holding a remaining 40% equity stake alongside contractual agreements for continued supply and distribution services over up to five years [S1][S20].

Historical Financial Performance

ICU's revenues peaked recently at approximately $2.38 billion in FY24 but contracted to about $2.23 billion in FY25 representing a -6.3% year-over-year decline primarily from tariff-driven cost pressures impacting sales volumes and pricing dynamics as well as the partial divestiture of IV Solutions revenue streams [F1]. Operating income held almost flat year-over-year at ~$42.8 million but net profitability improved drastically from an over $117 million loss in FY24 to near breakeven at around $0.7 million net income in FY25 due to operational efficiencies alongside significant debt prepayments funded by the divestiture proceeds reducing interest burden [F1].

Financial Summary Table

Historical performance (annual)

| FY | Rev ($bn) | Net ($mm) | CFO ($mm) | OpInc ($mm) | Rev YoY | Net YoY |

|---|---|---|---|---|---|---|

| 2025 | 2.2 | 1 | 180 | 43 | -6.3% | +100.6% |

| 2024 | 2.4 | -118 | 204 | 43 | +5.4% | -296.9% |

| 2023 | 2.3 | -30 | 166 | 23 | -0.9% | +60.1% |

| 2022 | 2.3 | -74 | -62 | -43 |

Note: Omitted columns lack sufficient annual XBRL coverage in the provided tags (need ≥2 annual points): Capex, Div. Source: SEC companyfacts cache [F1].

Capital returns and efficiency (annual)

| FY | Buybacks ($mm) | FCF ($mm) | ROE% |

|---|---|---|---|

| 2025 | 9 | 92 | 0.0 |

| 2024 | 12 | 125 | -6.0 |

| 2023 | 9 | 82 | -1.4 |

| 2022 | 11 | -152 | -3.6 |

Source: SEC companyfacts cache [F1].

Note: Dividends paid not available from tags.

Revenue Drivers & Challenges

The dip in FY25 revenue correlates strongly with increased U.S.-imposed reciprocal tariffs amounting to about $33.6 million expense, hitting products manufactured chiefly in Costa Rica where a tariff hike from 10% to 15% was applied mid-2025; products made in Mexico largely remain tariff-exempt under USMCA—a significant relief given the company’s manufacturing concentration across these two countries [S1][S2]. These tariffs have amplified cost of goods sold directly or indirectly pressuring prices or margins.

Additionally, the U.S Commerce Department's investigation under Section 232 examining whether imports of medical consumables pose national security risks threatens further tariff escalation or revised exemptions with uncertain potential impacts on supply chain economics [S1][S2]. Delays linked to such trade investigations could disrupt order fulfillment timelines.

On the operational side, the closure in February 2026 of an FDA Warning Letter issued initially in 2021 concerning quality system regulations at Smiths Medical's Minnesota facility provides some regulatory clarity after years of remediation efforts; however, an April 2025 Warning Letter citing modifications to MedFusion™ Model 4000 Syringe Infusion Pump and CADD™ Solis VIP Ambulatory Infusion Pump requiring new FDA clearances adds near-term uncertainty especially as new-generation device submissions await FDA review [S8][S21]. These regulatory actions necessitate ongoing investment in compliance vigilance.

The April-May 2025 establishment of the Otsuka joint venture divesting majority ownership of IV Solutions materially reshaped ICU’s reported revenues—IV Solutions had been historically significant but now contributes only via equity losses recorded from the JV stake plus service fees under continuing commercial agreements [S1][S20]. This pivot aims to leverage scale advantages through partnership but results in reduced standalone top-line figures.

Growth Prospects & Constraints

Looking ahead, growth levers include expansion of the safer infusion pump systems footprint supported by integration of proprietary safety software interfacing with hospital EHRs; enhanced vascular access solutions promoted through acquisitions like Pursuit Vascular’s ClearGuard® technologies targeting infection reduction; and broader international penetration enabled by Smiths Medical’s global reach post-acquisition [N3][S14]. Respiratory and vital care product lines also provide diversification beyond core infusion systems.

However, key constraints remain:

- The evolving tariff landscape creates cost unpredictability that may constrain pricing flexibility or dampen demand especially if USMCA benefits erode.

- Regulatory clearances for next-gen infusion pumps are pending, posing timing risk for launches impacting future sales momentum.

- The IV Solutions joint venture limits direct revenue recognition although operational synergies may offset through service contracts.

- Supply chain inflationary pressures along with freight cost volatility persist amid geopolitical tensions affecting raw materials sourcing [S1].

Monitoring how Section 232 investigations resolve will be essential for assessing trade risk exposure going forward.

Guidance & Milestones

Explicit formal guidance documents for FY26 earnings were not provided within available filings or news releases ([N1]), but capital expenditure estimates for manufacturing growth range from $85 million to $100 million reflecting investments principally aimed at equipment enhancements across Costa Rica, Mexico, Europe, and U.S coastal plants designed both to support existing product lines and place larger numbers of infusion pumps outside the U.S.[S4]. Watching FDA clearance status for updated MedFusion and CADD platforms remains critical milestones influencing product pipeline health.

Returns & Capital Allocation

Though ICU Medical’s net margin remains razor-thin yielding an approximate zero percent ROE (based on near break-even net income versus roughly $2.12 billion equity end-2025), positive operating cash flow stands out at nearly $180 million enabling free cash flow generation roughly estimated at $92 million after subtracting capex spend [F1].

Investment spending has ticked up modestly alongside consistent share repurchases totaling about $8.8 million executed during FY25 suggesting measured stock buyback activity remains part of capital return strategy albeit on a small scale relative to market capitalization [F1]. No dividend payments were disclosed indicating capital retained predominantly for reinvestment or debt servicing purposes.

Substantial debt prepayment activity during FY25 totaling $290 million was funded largely through IV Solutions JV sale proceeds; this has deferred principal amortizations primarily beyond FY29 on Term Loan B which matures January 2029 while Term Loan A refinanced with a $750 million facility maturing October 2030 reduces near-term leverage pressure [S4][S5][S6]. Interest rates under new credit facilities have adjusted modestly based on leverage ratios featuring margin tiers tied to covenant compliance metrics.

The company maintains compliance with all financial covenants presently despite these significant credit arrangements ensuring liquidity buffers remain intact.

Industry Context Analysis

In the medical device segment focused on infusion therapies and vascular access products—critical tools used daily across hospital workflows—customers prioritize reliability coupled with enhanced safety features that reduce medication errors or catheter-related infections which can drive multi-million dollar risk reductions per hospital stay cycle (analysis). The integration of software platforms providing real-time alerts around infusion dosing aligns with broader digital health trends embracing interoperability mandated increasingly under regulatory oversight (analysis).

Manufacturing span over multiple Latin American sites leverages trade agreements like USMCA which helps offset global inflationary pressures but conversely exposes companies like ICU Medical vulnerable where diplomatic shifts backtrack exemptions or impose retaliatory tariffs on key components imported or assembled abroad (analysis).

Overall competitive moats stem from entrenched hospital relationships built on entrenched installed bases for pumps coupled with high switching costs due to regulatory clearances necessary for alternative competitors limiting commoditization risks common elsewhere in healthcare consumables categories (analysis).

Conclusion & Watch Areas

ICU Medical enters FY26 balancing progress on legacy regulatory issues against tangible external pressures stemming mainly from trade tariffs that carved meaningful revenue headwinds last year compounded by strategic portfolio reshaping through its large IV Solutions joint venture transaction that altered growth visibility metrics superficially downward.

Key watch factors include:

- Outcomes from national security tariff probe under Section 232 affecting import duties beyond current levies;

- FDA clearances for newer infusion pump models critical for replenishing growth trajectories;

- Execution effectiveness integrating Smiths Medical’s products globally;

- Capital expenditures utilization efficiency supporting market expansion versus compression due to cost inflation;

- Debt covenant compliance monitoring especially given amortization timing exposures.

The company’s expansive addressable market coupled with an entrenched product ecosystem supports stable operating margins presently but tightening external macro factors merit attention when evaluating future operational resilience.

This analysis summarizes publicly available information as of early 2026 without offering investment advice or price targets.

Disclaimer: This is research-only, informational analysis and not investment advice. It may include AI-generated interpretation and general industry context. Always verify important details using primary sources.

Comments